(P&I) Dividend Risk & Dividend Yield

Oklahoma Land Rush 1889 But it’s free!

Essay. Investors want more – better prices for the stocks that they own, and better dividends for the stocks that pay them – and so, on balance, they routinely beat each other up in the stock market, trying to get more from other investors who don’t really have that much more.

As a consequence, in the absence of logic, the “market” is a noisy place and most investors, by number if not by money or capital, are going to get beaten.

But that’s the deal, and investors can (and do) use whatever tool (or club) they like in order to “beat” other investors. If it can be helped, then such help might be to remember that an investment is just and only the purchase of “risk” and it requires only three things to be a “good purchase” – 100% capital safety, 100% liquidity, and a hopeful but not necessarily guaranteed return above the rate of inflation – and if it doesn’t have those three things, it’s just a gamble.

And those three things – safe, liquid, and hopeful – are not hard to verify, no matter what the tool (or “club”), but failing that, we can still choose to believe that Zeus is the source of all thunder, lightning, and magic.

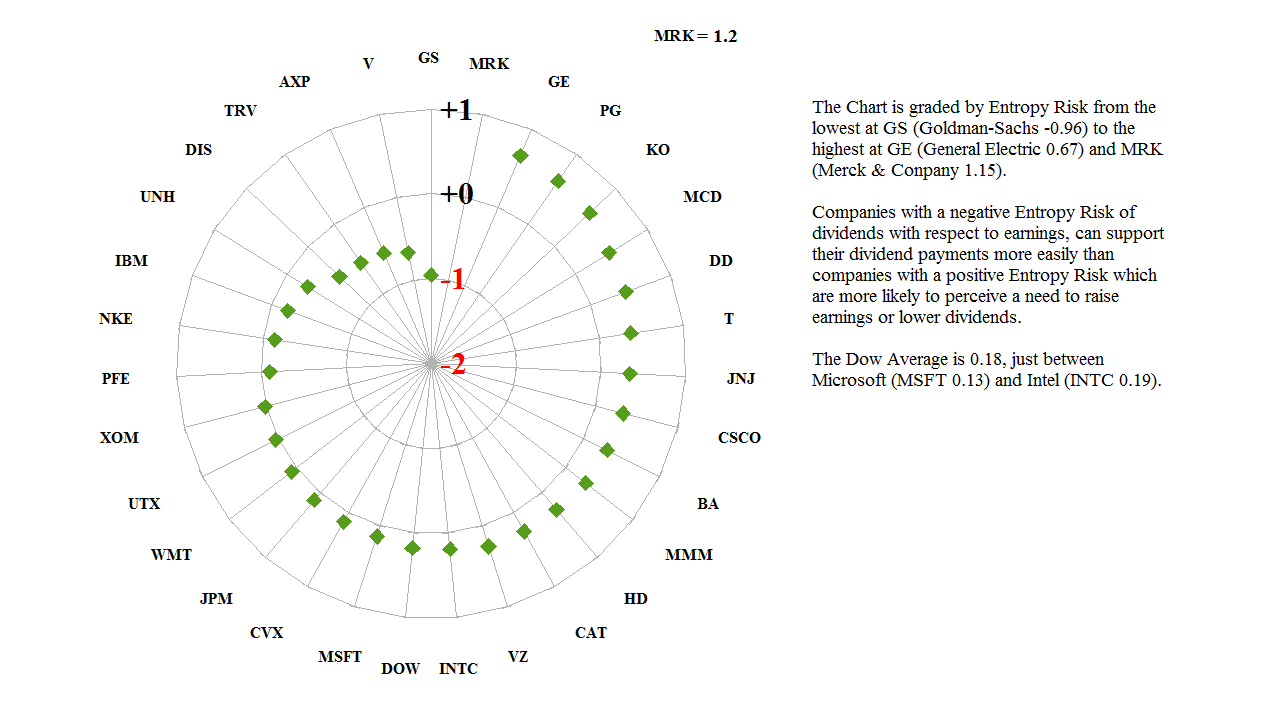

Figure 1: Dow Industrials Entropy & Dividend Risk

We define “risk” not as “volatility”, but as the demonstrated and verifiable ability to accumulate whatever we have, towards our goal, which is “more” of what we have.

For example, more dividends linked to more earnings; please see Figure 1 on the right, and for more information, please see our recent Post, “(P&I) The Process – Entropy Risk“.

From the chart, we can see that some companies have no problem supporting their dividends from earnings, and for those, the “risk” is negative, but other companies need to work for it, and for them, the “risk” is positive and a challenge that might cause them to work harder and smarter for higher earnings, or implement a lower dividend rate as a “return of earnings”.

In the latter case, they might be considered a “growth company” because they keep more of what they earn, but they will still have positive risk if they return more than 36.8% of their earnings.

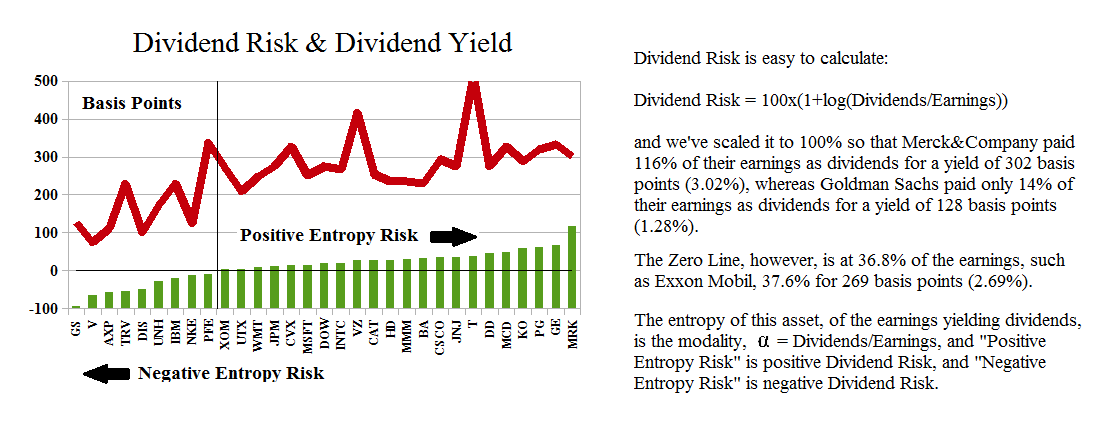

Figure 2: Dow Industrials Dividend Risk & Dividend Yield

But how is such “risk” priced in the market?

That is, are investors willing to bid-up the stock prices of companies which need to work harder to make their earnings and pay their dividends?

And the (surprising) answer is – No – on balance, virtue is not rewarded with a higher stock price; please see Figure 2 on the right.

The companies on the left of the chart have the least Dividend Risk; and lower (and the lowest) payout rates less than 36.8% of their earnings; and the lowest Dividend Yields, but the “highest” stock prices, and we would say that they were “overvalued” with respect to the companies on the right.

The companies on the right all have positive Dividend Risk; and higher (and the highest) payout rates in excess of 36.8% of their earnings; and the highest Dividend Yields, but “lower” stock prices, and we would say that they were “undervalued” relative to the companies on the left.

The Dividend Yields are, of course, directly and inversely related to the stock prices, and the terms “overvalued” and “undervalued” don’t mean anything unless investors are willing to sell the former and buy the latter.

But that’s an actionable “investment strategy” – sell on the left and buy on the right – and that will tend to level-out the dividend yields to between 200 and 400 basis points, for which the “bond players” will “kill” each other, and even for less than 50 basis points in the frenzy for yield; to put it another way, sell the high-priced and low-yielding stocks, and buy the low-priced and high-yielding stocks, and we say that a stock is “high-priced” if it returns less than 36.8% of its earnings, and “low-priced” if it returns more than 36.8% of its earnings (sic).

Moreover, there is lots of opportunity, limited only by our budget, and not by what the market is doing today; please see Exhibit 1 below for an all-market summary of the big-caps.

Exhibit 1: Major Market Dividend Risk & Dividend Yields

Figure 1.1: Dow Industrials Dividend Risk and Dividend Yield |

Figure 1.2: Dow Transports Dividend Risk and Dividend Yield |

Figure 1.3: Dow Utilities Dividend Risk and Dividend Yield |

|

Figure 1.4: S&P 100 Dividend Risk and Dividend Yield |

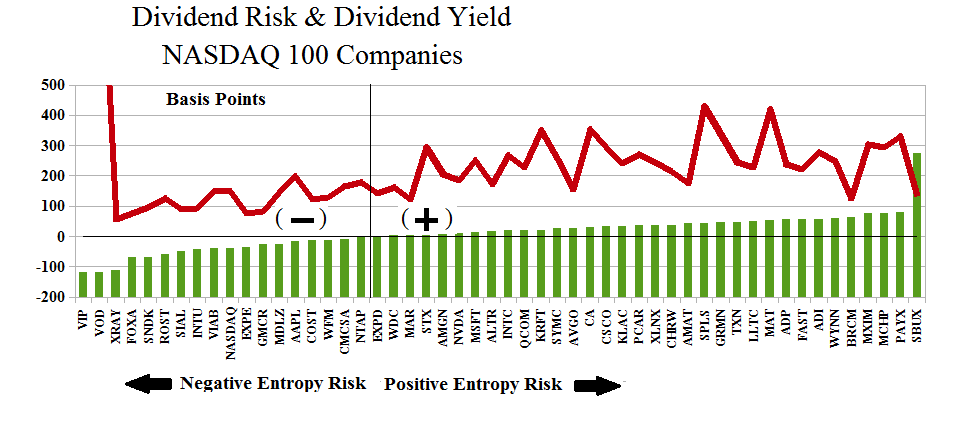

Figure 1.5: NASDAQ 100 Dividend Risk and Dividend Yield |

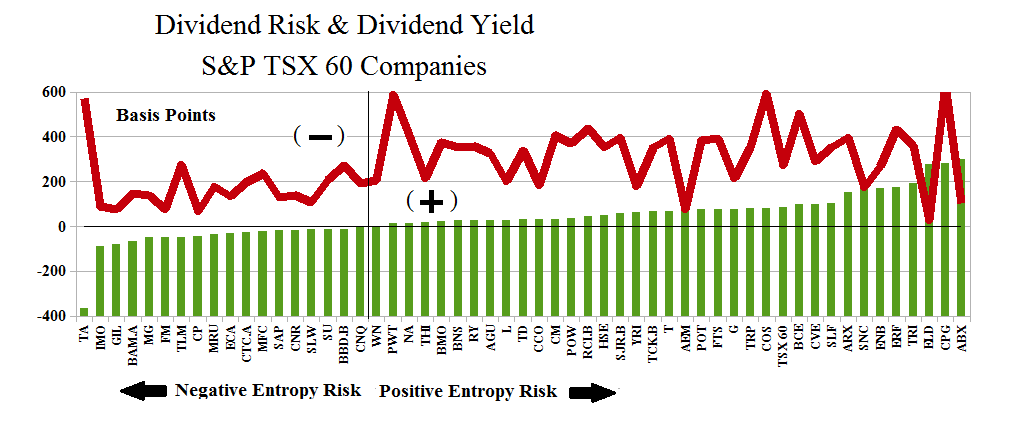

Figure 1.6: S&P TSX 60 Dividend Risk and Dividend Yield |

In Figure 1.4 for the S&P 100 companies, Citigroup is on the extreme left-hand side with a miserly return of earnings of 1.3% and a dividend yield of 8 basis points (0.08%); the stock price is off minus (-4%) for the year, but the [P/E]-multiple is just 16× which might explain why many investors think that it is “undervalued”; we think otherwise, and we think zero rather than the current $50 per share and a market value of $150 billion.

Indeed!

Starbucks is on the extreme right-hand side with a return of earnings of 578% (yes) and a dividend yield of 1.3%; the stock is trading with a [P/E]-multiple of 400× and the market value has hardly moved all year off its current $58 billion; we would think it rational for the stock price to decline, but we don’t make the prices and, obviously, the investors believe that good coffee makes a good stock.

In Figure 1.5 for the NASDAQ 100 companies, only fifty-two of them pay dividends as a matter of policy; the NASDAQ is thought of as “growth stocks” and there might be something to that because the return on the shareholders equity is 25% which exceeds that of other markets such as the Dow Industrials (18%) or the Dow Utilities (8%) and is similar to the Dow Transports (28%) which are also light on dividends.with an aggregate return of earnings of only 23%.

Courtesy: VimpelCom Limited

VimpelCom, Vodafone, Dentsply, and Twenty-First Century Fox are on the extreme left, and Starbucks is (again) on the extreme right; VimpleCom lost ($3 billion) last year but paid dividends of $3.8 billion (anyway) for a dividend yield of 25%, but that hasn’t done much for the stock price which is off (-30%) at $8.50 for the year so far.

The S&P TSX 60 (Figure 1.6) is a little bit more challenging to our theory (or principle), but still manages to pull-off yields of 200 to 400 basis points on the right, but less than 200 basis points on the left; the bottom-feeders on the right are Agnico-Eagle Mines (0.77% or 77 basis points), SNC-Lavalin Group (1.72%), Eldorado Gold Corporation (0.25%), and Barrick Gold Corporation (1.04%) with a dividend payment of $233 million despite losses of $12.7 billion last year.

Zeus? Is that you?

Some companies accept debt covenants that are tied to the stock price, or the payment of dividends, which might explain “investor-like” behaviour in corporate managements with a different reality.

Moreover, when we look at the entire universe of S&P NYSE big-cap companies (about 800 of them), we can see how really conflicted investors are about what they want and how they might get it – the words “random” and “noise” and “thunder” come to mind; please see Exhibit 2 below.

Exhibit 2: S&P NYSE Dividend Risk & Dividend Yields

S&P NYSE Dividend Risk and Dividend Yields

For more details, please see our Posts “(P&I) The Process – The 1st Real Dollar” which shows how a “currency” gets its value from the “subsistence economy” at the Company D modality, and “(P&I) The Process – The Guns of August” which explains how that modality actually “works”.

For more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice. And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

And for more information on real “risk management” and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary; we’ve also profiled hundreds of companies in these Posts and the Search Box (upper right) might help you to find what you’re looking for.

And for more on what risk averse investing has done for us this year, please see our recent Posts on The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.

Ι think the admin of this site is truly working hard in favor of his

web site, for the reason that here every material iѕ quality based information.

LikeLike

Thanks for sharing your thoughts about situs bola.

Regards

http://qq188cc.co/

http://qq188cc.co/en.php

http;//qq188cc.co/ch.php

LikeLike