(P&I) The Process – Entropy Risk

Compound Interest

Essay. Entropy risk affects all assets – if an asset can be “capitalized”, then it has a modality and, therefore, an entropy, and its “development” by capitalization has, necessarily, the same structure as, for example, the development of the firm, which is a much richer structure than mere “compounding”, or even “continuous compounding”, that is fundamental to all of finance and most of economics.

In the context of the theory of the firm, the modality, α = R/P, is defined by the ratio of “what is owed to the firm” (R) and “what it owes” (P), and we know that if there is a “conservation law”, which is the balance sheet in this case, then the “payables” and “receivables” that are created and negotiated between the “parties”, who are the firm, the “producer”, and the “customer”, the trading connections, will develop into the 1st and 2nd E-conditions, a×log(a) = α×log(b) and b×log(b) = α×log(a), respectively, where a=p((a)) and b=p((b)) are the measures, or probabilities, of sets (a), of “payables”, and (b), of “receivables, that are in-process, and “the process” is accumulating (P) to (R).

In specie, R = P×exp(log(R/P)) = P×exp(r), where r=log(R/P)=log(α) and, hence, the continuous rate of compounding, r, is negative if 0<α<1, and positive if α>1, and Risk(α) = 1 + log(α) has the property that Risk(α)<0 if α<1/e =0.368… , and Risk(α)>0 if α>1/e.

The modality is a “state measurement” and we have shown that its value is the “entropy” of the process as Ω(b) = -∫ b(a)×log(b(a))da = -∫α×log(a)da = -α×[a×log(a) – a] = α on [0,1]; please see our Post “(P&I) The Process – System Dynamics” for more information and the two Posts “(P&I) The Process – The WalMart Company B Story” and “(P&I) The Process – Debt & The Company We Keep” for additional examples.

An asset – and we consider “liabilities” to be assets in the context of company or process development, rather than the object of mere debt service, which is just the “price of money” and is just a number that we know – that has negative risk is an “opportunity” because its current price is discounted to what we can reasonably expect that it will become, should we work at it, if such work is required.

In contrast, an asset with positive risk is an “investment” because we can only be hopeful that it will develop its “full value” and, in practice, some work is required of the asset rather than of us, as “investors” who are not the “producers”.

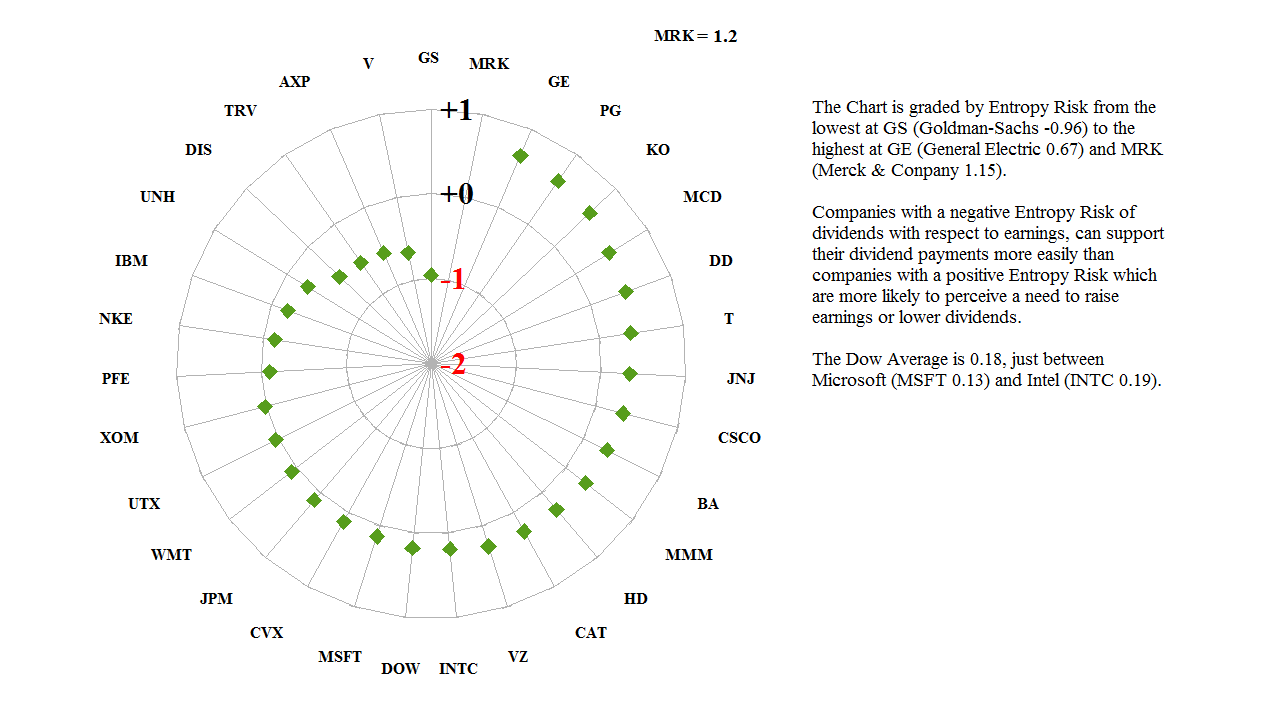

Figure 1: Dividend Risk in the Dow Industrials

This has some interesting consequences; for example, dividend payments that are in excess of 36.8% of the earnings are “at risk” whereas dividend payments that are less than 36.8% of the earnings have “negative risk”, and the point of view is that of the company rather than the investor, who might take the opposite point of view with no foundation because it is earnings that “create” dividends and not dividends that create earnings (for the company rather than the investor, who does no “work”); please see Figure 1 on the right.

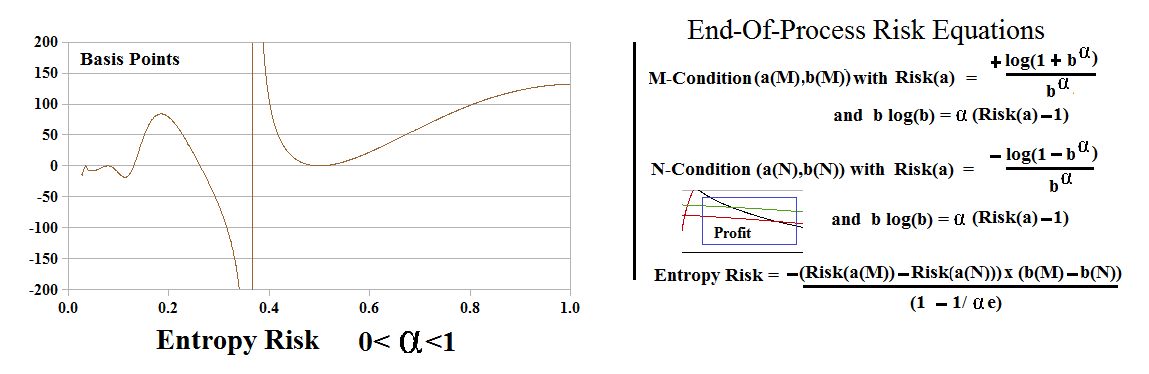

Entropy Risk in Basis Points

Figure 2: End-Of-Process Company A Risk Co-ordinates

We can also “monetize” entropy risk by converting its value into “basis points”.

In the case of the firm, the ability to negotiate an outcome at the end-of-process is determined by the “size” of the “blue box” which has the co-ordinates (Risk(a(M)), b(M)) and (Risk(a(N)), b(N)), in our usual notation; please see the “blue box” in Figure 2 on the left, and for more examples, the aforementioned Posts.

The area of this box is -(Risk(a(M)) – Risk(a(N)))×(b(M)-b(N))/(1-1/eα) where we have “oriented” the box to the “producer preference” of “less a(M) is preferred to more a(M)” and “more b(M) is preferred to less b(M)” meaning that in the absence of negotiation, the default solution favours the producer.

Figure 3: Producer Risk

We have also “normalized” the box by the relevant area which is between Risk(a) = 1-1/eα, on the left, and Risk(a)=1 on the right; please see Figure 3 (on the left).

The “risk” is formally infinite (“indeterminate”) at α=1/e=0.368… because that’s Company D, and we can’t leave Company D without some help, which is available but we need to ask for it; please see our Post “(P&I) The Process – Debt & The Company We Keep” for more details.

For more details, please see our Posts “(P&I) The Process – The 1st Real Dollar” which shows how a “currency” gets its value from the “subsistence economy” at the Company D modality, and “(P&I) The Process – The Guns of August” which explains how that modality actually “works”.

For more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice. And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

And for more information on real “risk management” and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary; we’ve also profiled hundreds of companies in these Posts and the Search Box (upper right) might help you to find what you’re looking for.

And for more on what risk averse investing has done for us this year, please see our recent Posts on The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.