(B)(N) PETM PetSmart Incorporated

Courtesy: PetSmart Incorporated

Deal Book. The hedge fund, Jana Partners, has taken a 9.9% interest (just short of 10%) in the lead-dog in the care, feeding, and lifetime needs of our pets, PetSmart Incorporated, and they pointed-out to us that the stock is “undervalued” and that they want to talk about “selling the company, improving the operating performance, and capital structure” (The Street, July 3, 2014, PetSmart Shares Surge on Jana Stake).

And, indeed, they’re right – people used to pay $70 for this stock as recently as in December, but today it’s just $60 were it not for the added-value ($67) from the Jana Partners, on Friday, already; please see Exhibit 2 below.

This market needs more leadership like that and, so, we found thirty-three other companies in the (smaller) NASDAQ that are similar to PetSmart as far as their financials and dividends are concerned.

They all have a market value between $1 billion and $20 billion, which makes them perfect for growth and budget-minded hedge funds; they all pay dividends; and they are all grandly Company C with modalities α>1.5, such as PetSmart itself, which has a modality of α=2.5 meaning that it is currently owed more than 2.5 times what it owes (please see The Theory of the Firm) and is, therefore, in a good position to do whatever it wants to do.

Modality, of course, does not drive the stock prices because “good companies” don’t necessarily get “good stock prices” (The Street, July 3, 2014, Cramer: Good Companies Are Horrible Shorts), and we’ll get lots of evidence of that below, and we will also need to confront the enigma of “stock prices” and “value”, and what we can do to defend ourselves and save our money from harm.

However, despite that, we can expect that these companies will still be there for the long-term, and can pay dividends (as they are wont to do) even if there is a slack earnings season or so; please see Exhibit 1 below, and for all the details of the fundamentals, please click on the link “NASDAQ Undervalued – Fundamentals“.

Exhibit 1: PetSmart and the NASDAQ Undervalued – Fundamentals – July 2014

PetSmart and The NASDAQ Undervalued – Fundamentals – July 2014

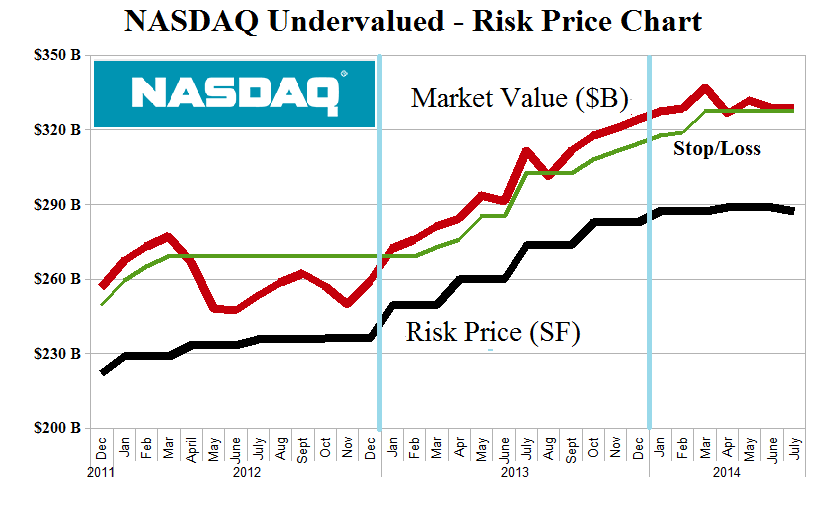

Figure 1.1: PetSmart and The NASDAQ Undervalued – Risk Price Chart – July 2014

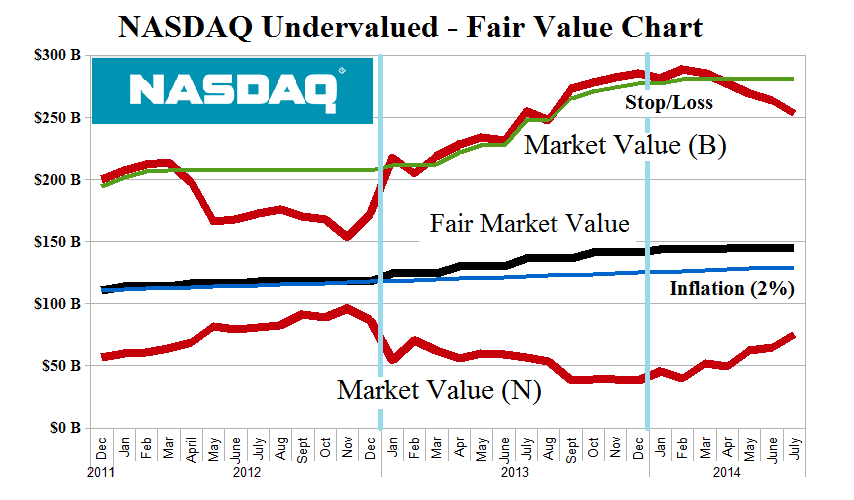

Figure 1.2: PetSmart and The NASDAQ Undervalued – Fair Value Chart – July 2014

These thirty-three companies gained a miserly +1% in 2012, but were up +25% last year, and now, are off by 3% from gains of +4% earlier this year; please see Figure 1.1 on the left.

They also paid dividends of $6.9 billion for a return of earnings of 46% and a dividend yield of 2.1% to the apparently less than grateful shareholders.

The (B)(N)-portfolio in Figure 1.2 was off minus (-14%) in 2011, but roared-back with +65% last year, and then wound-down a bit with minus (-11%) so far this year.

But, we don’t need to ride the roller-coaster of investor and market fancies if we maintain an attentive stop/loss policy, which we gear to the price of risk, but which could also be enforced in the (B)-class companies by setting a sell price below (not above) the current stock price.

However, that policy can’t be usefully enforced in the (N)-class companies which, as a portfolio, lost minus (-55%) last year, but then roared-back with +95% so far this year, not because of astounding stock price increases, but because the number of (N)-class companies increased from four to eight; please see Figure 1.2 above and click on the links below for more details.

We also note that the market value of the (B)- and (N)-class portfolios (Figure 1.2 above) depends on stock prices and the number of companies that are in the portfolio, because companies can drift in and out of these classes which are defined by the price of risk rather than the stock prices; the “Fair Market Value” is a better gauge of the enduring “worth” of these companies than the stock prices, because it is a measure of the demand for these stocks at whatever prices they’re showing.

In the midst of all this “activity”, the equal weighted by value Perpetual Bond™, in the same group of companies, returned +8% in 2012, +47% last year, and is still up +5% so far this year; for more details, please click on the links (and again to make them larger if required) “NASDAQ Undervalued – Prices & Portfolio” and “NASDAQ Undervalued – Portfolio & Cash Flow Summary“.

Safe, Liquid, and Hopeful.

What’s missing in the vocabulary of the hedge funds are the words – safe, liquid, and hopeful – for which they substitute the all too familiar “sale”, “operational efficiency” (headcount) and “capital structure” (more debt before the sale) because their bread is not buttered on the same side as ours.

But these companies, all thirty-three of them, are all the same in what matters – their payables and receivables – and they could take on more debt, indeed, $70 billion of new debt, doubling their current debt (please see the link “NASDAQ Undervalued – Fundamentals“), and they could become leaner and meaner machines, but why, when their return on earnings is 46% and their return on equity is a respectable 15% , which outstrips the hedge funds who are coming to “fix” them with votes, proxies, and a power-point. Woof!

Exhibit 2: (B)(N) PETM PetSmart Incorporated – Risk Price Chart

(B)(N) PETM PetSmart Incorporated – July 2014

PetSmart Incorporated provides specialty products, services and solutions for the lifetime needs of pets in North America. It offers products for all the life stages of pets, professional grooming, training, day camp for dogs and boarding.

From the Company: PetSmart Incorporated, together with its subsidiaries, operates as a specialty retailer of products, services, and solutions for pets in the United States, Puerto Rico, and Canada. The company offers consumables, such as pet food, treats, and litter; and hardgoods, which include pet supplies and other goods comprising collars, leashes, health care supplies, grooming and beauty aids, toys, apparel, and pet beds and carriers, as well as aquariums and habitats, accessories, décor, and filters for fish, birds, reptiles, and other small pets. It also provides fresh-water fish, small birds, reptiles, and small pets; and pet services, such as dog training, pet grooming, and pet adoption services. In addition, the company operates PetSmart PetsHotels that offer boarding for dogs and cats; provides personalized pet care, temperature controlled rooms and suites, daily specialty treats and play time, and day camp services for dogs; and operates veterinary hospitals, which offer services comprising routine examinations and vaccinations, dental care, a pharmacy, and surgical procedures. As of March 05, 2014, it operated approximately 1,333 pet stores; and 199 in-store PetSmart PetsHotel dog and cat boarding facilities. The company also offers pet food and pet products through an e-commerce site, PetSmart.com. PetSmart, Inc. was founded in 1986, has 26,000 employees, and is based in Phoenix, Arizona.

For more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice. And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

And for more information on real “risk management” and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary; we’ve also profiled hundreds of companies in these Posts and the Search Box (upper right) might help you to find what you’re looking for.

And for more on what risk averse investing has done for us this year, please see our recent Posts on The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.

{kind=link}

{kind=link}

{kind=link}