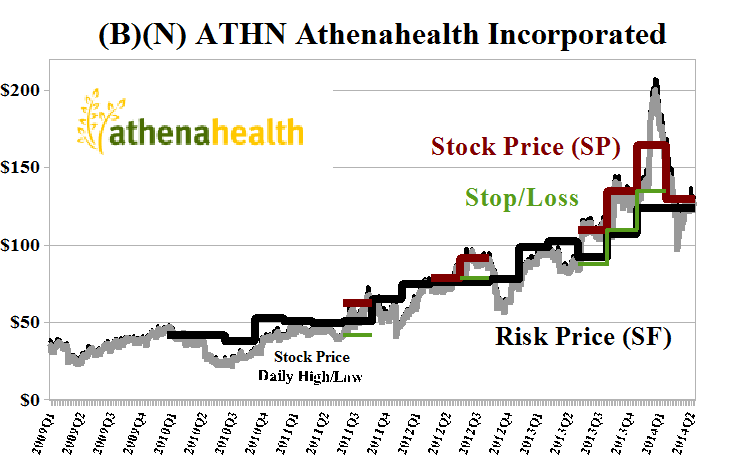

(B)(N) ATHN AthenaHealth Incorporated

Great Expectations by Charles Dickens 1861

Deal Book. It’s estimated that Americans will spend about 18% of every dollar that they earn on “healthcare”, if not in every year, then over time, and if we “ball park” the budget, it looks something like taxes (30%), home (20%), automobile (10%), healthcare (18%), and what’s left is 22% for everything else, including food, clothing, and savings (net of vacations, weddings, and divorces that might affect 50% of the families).

That’s “life” if the family income is less than $100,000 per year, with some adjustments to the priorities if the family income is a more typical $50,000 or less, and it’s clear that “life” is a lot of hard and steady work for most folks.

And it’s nothing like “Hollywood” or the family serials and soap operas that flood our televisions, and the best time of life for most people will be the “school years” between the ages of four and eighteen, with the hope that they graduate with a skill or the ability to obtain one.

Safe, Liquid, and Hopeful.

To which we must add the “punishment” of our savings by an investment industry that is not oriented towards capital safety, liquidity and a hopeful but not necessarily guaranteed return above the rate of inflation – the three words that move us – safe, liquid, and hopeful – but towards the “risk/reward equation” that is made in Hollywood and played-out on Wall Street (Business Insider, July 6, 2014, This Man’s ‘Healthcare Internet’ Has Ignited A Huge Controversy On Wall Street).

Wall Street funded Athenahealth in 2007 with a NASDAQ IPO of 6.3 million shares at $18 ($113 million), and the company has since floated an additional 32 million shares (currently 37.8 million shares outstanding) to fund its growth because the company makes an average of about $10 million a year, and last year it made only $2.6 million, or $0.07 per share, and the company is still 50% owned by just six institutions, and 90% by twenty.

The American Trilogy, John Dos Passos, 1936

Obviously, this is not a playground for “Main Street”, but we rely on the institutions to invest our money for a hopeful return that exceeds the rate of inflation, but some of them bought the company at $200 early this year, and it’s now trading at $130; on the other hand, some of them bought the company at $20-$30 in 2010, and might have remembered to sell some of it when their “good fortune” exceeded even their wildest dreams.

But we can’t be sure of that and, on balance, the travails and returns of mutual funds and hedge funds and pension plans suggest more of John Dos Passos than Charles Dickens.

Our best estimate of the price of risk at the current time is $124 with a downside due to the demonstrated ambient “volatility” – largely due to investor uncertainty and opportunism, in this case – of minus (-$30) in the next quarter; please see Exhibit 1 below, and note our attentive stop/loss behaviour. Skål!

Exhibit 1: (B)(N) ATHN Athenahealth Incorporated – Risk Price Chart

(B)(N) ATHN Athenahealth Incorporated

AthenaHealth Incorporated is a provider of Internet-based business services for physician practices. Its cloud-based services include four integrated offerings: athenaCollector, athenaClinicals, athenaCommunicator, and athenaCoordinator.

From the Company: AthenaHealth Incorporated, a business services company, provides ongoing billing, clinical-related, and other related services to medical group practices primarily in the United States. The company provides services through the athenaNet, a proprietary Internet-based practice management application. It offers athenaCollector, a revenue cycle management service that automates and manages billing-related functions for physician practices, and includes a practice management platform. The athenaCollector assists its physician clients with the handling of claims and billing processes to help manage reimbursement. The company also provides Anodyne Analytics, a business intelligence application, which offers physicians and practice managers with insight into practice performance; and Healthcare Data Services that offers practices an understanding of the cost and quality of the care to patients. In addition, it offers athenaClinicals, an electronic health record service that automates and manages medical-record-management-related functions for practices, as well as assists medical groups with the handling of physician documentation, orders, and related inbound and outbound communications. Further, the company provides athenaCommunicator that allows practices to manage patient communication tasks electronically; the creation of a self-service patient portal for registration, appointment requests, bill payments, and general communication; automatic generation of emails to patients; and patient education tools. Additionally, it offers athenaCoordinator, a referral cycle management tool that helps streamline the disorganized system of patient care coordination. athenahealth, Inc. sells its products through a direct sales force, as well as through channel partners. The company was formerly known as athenahealth.com, Inc. and changed its name to athenahealth, Inc. in November 2000. athenahealth, Inc. was incorporated in 1997, has 3,000 employees and is headquartered in Watertown, Massachusetts.

For more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice. And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

And for more information on real “risk management” and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary; we’ve also profiled hundreds of companies in these Posts and the Search Box (upper right) might help you to find what you’re looking for.

And for more on what risk averse investing has done for us this year, please see our recent Posts on The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.