(P&I) The Swiss Franc Debacle

Swiss Francs – only (-0.75%), you say?

Drama. If we are going to hold a currency pending further investments, it’s a good idea to hold a currency that belongs to a “deflationary” economy rather than an “inflationary” economy, and the terms are relative if we’re considering investments across currencies.

For example, we could hold Swiss Francs (CHF) in order to purchase investments in Euros that produce Euros, if we understand that the Euro is more subject to inflationary pressures than the Swiss Franc, and therefore, such investments will tend to be “cheaper” than their Swiss-domiciled cousins.

How much do you want?

But, if we have Swiss Francs, or Euros, we ought not to buy Argentine Pesos, although we might consider buying Argentine real properties and investments, if they have any that they’re willing to sell; or even Argentine government debt in, for example, US Dollars, if there was some hope that the Argentine government could pay it back and service the interest in US Dollars (Bloomberg, October 29, 2014, A New Twist in the Argentine Debt Saga).

Governments, of course, never have a problem servicing their debt in their own currency; their people and industries that don’t have access to a better currency will pay for it, won’t they?

Moreover, not every deflationary economy is going to be good for it either, and in that, Switzerland has some things in common with Greece, Cyprus, and the Ukraine, among others; please see below.

But What About The Income?

The problem with lingering in a foreign currency, especially a deflationary one, is, What are we going to do for an income? How are we going to pay the “rent” without spending our money?

For example, the Swiss National Bank (SNB) has kept interest rates low, and even negative, since 2011 in order to discourage a demand for the Swiss Franc (which is a government debt) as an “idle” investment currency; and to buy an income, we needed to invest in Swiss-domiciled companies and their stocks, which tended to boost the price of stocks and make an income more expensive to acquire.

But that policy can’t be maintained if the government itself needs to borrow money (absent “printing it”) or industry needs to increase its debt for growth and has to pay a higher rate of interest to get it.

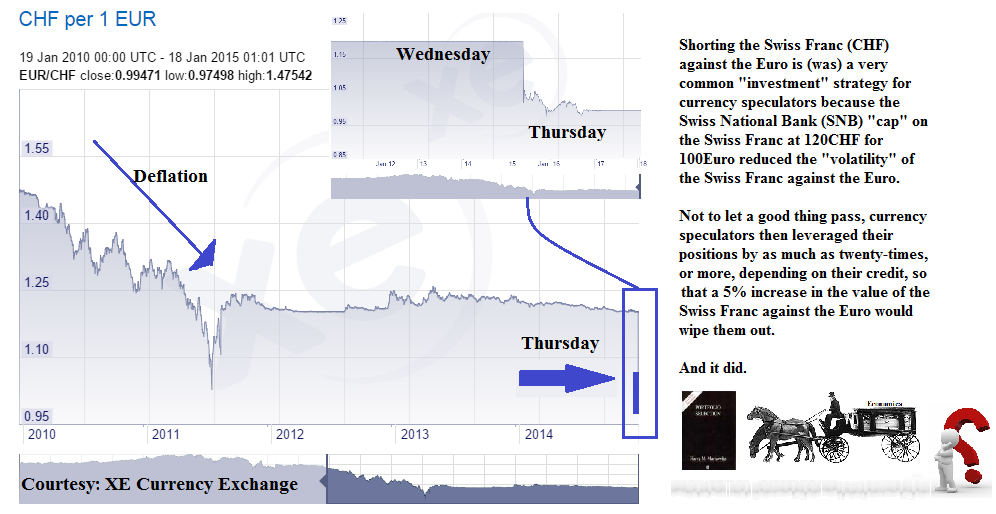

Figure 1: CHF per 1 Euro Courtesy: XE Currency Exchange

As a result, on Wednesday last week, we could buy 120CHF for 100€, but on Thursday, when the SNB lifted the “cap”, we could buy only 100CHF for the same 100€, and the stock market dropped by about 10% on the same day (Reuters, January 15, 2015, Swiss central bank shocks markets with currency ‘tsunami’) and investment firms and investors who were shorting (borrowing) the Swiss Franc last week, lost their shirts because they didn’t know what time it was (Bloomberg, January 17, 2015, Swiss Franc Trade Is Said to Wipe Out Everest’s Main Fund).

The Barometer and The “Hail Mary” Pass

The Swiss central bank has said that “”If you decide to exit such a policy, you have to take the markets by surprise” (ibid, Reuters). Indeed.

For example, it is a “gift” to well-heeled investors for governments which are “managing” a deflationary economy to pay a high rate interest for bonds issued in their own currency, and it is a gift that is paid-for by the taxpayers; similarly, corporations should acquire debt in an economy that is inflationary relative to their own, because the coupon and capital can be paid in “inflated dollars” in the future, relative to the “dollars” that they earn in their own currency.

However, the common measure of inflation is the Consumer Price Inflation (CPI), or possibly the Producer Price Inflation (PPI), both of which significantly lag the “inflation”, and neither of which might actually be present in an inflationary or deflationary economy; they are symptoms and not causes.

Figure 2: The Barometer

The signature and hallmark of a “deflationary economy” is that the price of an income is “high” (again, relative), and of an “inflationary economy” that the price of an income is “low”; for a brief explanation, please see Figure 2 on the right and our Post “(B)(N) What’s A Girl To Do?“.

For example, the policy of “Quantitative Easing” in the US has helped to drive-up the price of stocks and bonds, and, therefore, the price of an income in terms of dividends, in the past few years; moreover, if government bonds aren’t paying a high rate of interest, or corporations don’t need to borrow money, then the dividend payout rates can be reduced because the yields, despite the high price of stocks, don’t have to be that high if the earnings are strong.

However, investors don’t seem to show much respect for these facts; even though the Swiss Franc has been “inflated”, the Swiss economy is still deflationary and will wheeze itself flat.

As a result, investors have tended to not only want to feed at the trough, but to put their whole head in it in the pursuit of “capital gains” – their idea of an “income” – as has been demonstrated, again, by shorting the Swiss Franc against the Euro, which has put several of them into insolvency or bankruptcy this week, and by other investors who promptly dumped the stocks that they held in Swiss Francs, expecting an inflationary economy to emerge and, therefore, higher rates of interest for the Swiss Franc.

And they want the “Hail Mary” Pass too, by buying Euros as soon as possible, but it is already too late because the Swiss economy is deflationary, as are many other economies throughout the World, and the Swiss central bank has already said that they will “print money” – and they might have to if they can’t find investments for all the foreign currencies that they’re holding – rather than raise interest rates and compete with dividends in Swiss Francs; this latter problem plagued Japan for more than a decade, and it is still a problem now.

Switzerland, the Euro Area, and the World

The solution of the Swiss central bank problem is not to print more money, and keep “buying” foreign currencies, but to invest the foreign currencies that they hold in the foreign countries that will make it good; nor should that be foreign to them because Switzerland survives on exports, not imports.

According to the IMF and the World Bank, most of the World is inflationary, which they measure using the local Consumer Price Inflation (CPI) expressed in “international units” of Purchasing Power Parity (PPP) and that rate is 2.74%, and even higher (4.25%) when measured by the forward moving average – but it has been decreasing from much higher rates of 4.5% to 5.5% in the recent past; please see Figure 2 above.

Figure 3: The Barometer

The Barometer, however, is more sedate and optimistic; first of all, the World rate of inflation as measured by the Purchasing Power Parity (PPP) when weighted by the GDP* per capita, is 3.89% and a relatively steady 4.76% in the moving average, and neither of these rates has the same volatility and depressing declines as the CPI-based rates.

Moreover, the World is in need of investment because the GDP* uptake times are decreasing (currently 10.72 years) and the Trade* uptake times are increasing (currently 2.41 years), so that it is a (down)(up), or no worse than an (up)(up) situation pending a return to (down)(up) as the productivity of their investments is realized.

In contrast, the fourteen Euro Area countries are decidedly (up)(up), at 24.21 years and 3.42 years, respectively, and using the same measures as above (per capita income weighted), the rate of inflation is only 1.31% (2.12% in the forward moving average), and both rates have been declining.

Finally, the Swiss economy is the least-favored of these; the rates of inflation are (-0.24%) and 0.50% on the moving average basis, both of which have been declining, and they are decidedly (up)(up) at 30.18 years and 4.15 years, respectively; and they are in the good company of the Ukraine (-0.28%), Cyprus (-0.40%), Georgia (-0.51%), Mali (-0.60%), Palau (-0.76%), and Greece (-0.92%); please see Exhibit 1 and 2 below (and click on them, and again, to make them larger if required).

Exhibit 1: Switzerland, the Euro Area, and the World – The Barometer

Figure 1.1: The Barometer – Switzerland, The Euro Area, and The World

Exhibit 2: Winners in the Race to the Bottom

|

Figure 2.1: UKR Ukraine CYP Cyprus |

Figure 2.2: GEO Georgia MLI Mali |

Figure 2.3: PLW Palau GRC Greece |

For more examples from the Euro Area, please see our Posts “(P&I) The One World Food Bank” and “(P&I) The World Trader’s Almanac“, and for the Country Risk, “(P&I) The NYSE Mittelstand“.

And for more information on real “risk management” in modern times and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary and “(P&I) Dividend Risk and Dividend Yield“, and our recent Posts “(P&I) The Profit Box” and “(P&I) The Process – In The Beginning“; and we’ve also profiled hundreds of companies in these Posts and the Search Box (upper right) might help you to find what you’re looking for, such as “(B)(N) TLM Talisman Energy Incorporated” or “(B)(N) ATHN AthenaHealth Incorporated” or “(B)(N) PETM PetSmart Incorporated“, to name just a few.

And for more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice. And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

And for more on what risk averse investing has done for us this year, please see our recent Posts on “(P&I) The Easy (EC) Theory of the Capital Markets” or “(B)(N) The Easy (EC) Theory of the S&P 500“, and the past, The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.