(B)(N) The Swiss Short Squeeze

It was a Ratio.

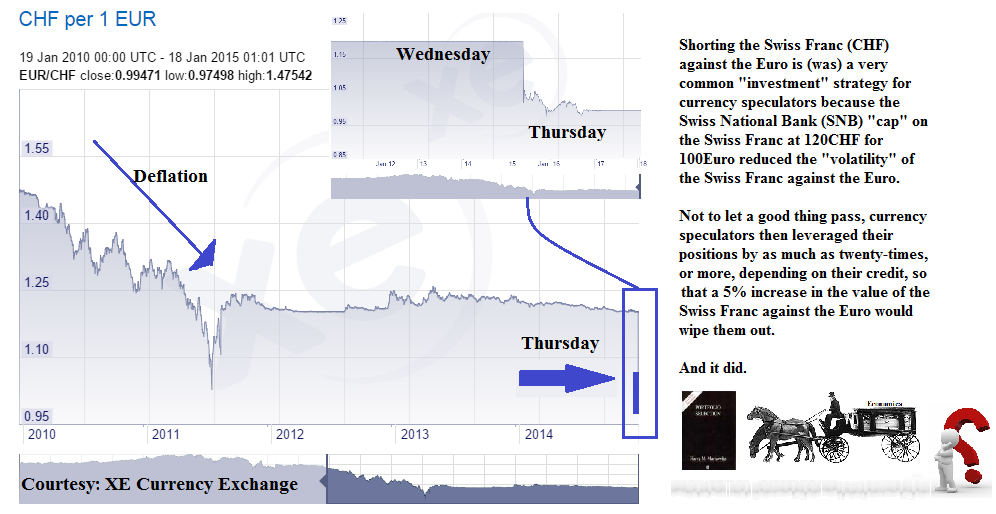

Drama. They say that it was a “tsunami” that swept through the World financial markets last Thursday and caused the equivalent of about US$800 billion to be “vaporized” between bankruptcies in the foreign exchange trade and an intra-day loss of about $100 billion Swiss Francs (CHF) in the Swiss Market Index (SMI) (Reuters, January 15, 2015, Swiss central bank shocks markets with currency “tsunami”).

But it wasn’t a tsunami – it was a “ratio” – the ratio CHF/Euro=120 that guaranteed that 100 Euros could buy no less than 120 CHF guaranteed by the Swiss National Bank (SNB), the central bank, that instantly fell to CHF/Euro=100 or less when the SNB dropped the “cap” and allowed the Swiss Franc to lift and rise up against the Euro and, therefore, against any other currency.

The Swiss Short Squeeze

Figure 1: CHF per 1 Euro Courtesy: XE Currency Exchange

The demand for the Swiss Franc has always been strong, but it became much stronger since 2009 (please see the chart on the right) and became a landslide in December with a huge influx of lazy money in rubles, yuan, and dinari, for example, looking for a safe harbor in Switzerland which they couldn’t find at home.

And Switzerland is a distinguished exporting nation in high-value goods and services, and in its currency, and the natural response to a persistent and increasing demand is to raise the supply, and the price, and the Swiss central bank did both with respect to its currency by printing more money, as it saw fit, and, secondly, by raising the discount, or interest rate on deposits, from a small positive return to a negative return and, most recently, minus 0.75% (-0.75%) on central bank deposits.

Figure 2: It was a Ratio that did it.

Both moves help its industry by helping to keep the price of the Swiss Franc low, or predictable, against the other currencies that buy its products; but the downside is that the interest rate earnings on bank deposits and government bonds are low, which means that its wealthy citizens who don’t have to work, but can live on the interest, will have a declining income against the Euros that they need to buy things with, and they will need to look elsewhere for it – which they did, in the stock market; please see Figure 2 on the right.

Figure 3: The Barometer – Switzerland, The Euro Area, and The World

The central bank move is certainly a gift to Swiss consumers – their Swiss Francs can buy more today than yesterday – but it’s a one-time gift and it will cast a shadow on its companies which will have to deal with higher prices for their exported goods and services, possibly offset by lower prices for their inputs and materials.

But the knee-jerk and mechanical reaction of the stock market investors is good for us because we have reason to think that the long-term deflationary pattern of the Swiss economy will not be so easily reversed by playing with their “money”; please see Figure 3 on the right which explains how the Swiss Franc figures in World and Euro Area trade.

What are they going to do for an income?

And, so, what are they going to do for an income?

To get an income, they need to invest, and that means that they want 100% capital safety and a hopeful return above the rate of inflation; anything else is just a gamble and that’s everything else (The Economist Buttonwood, January 19, 2015, Swiss miss).

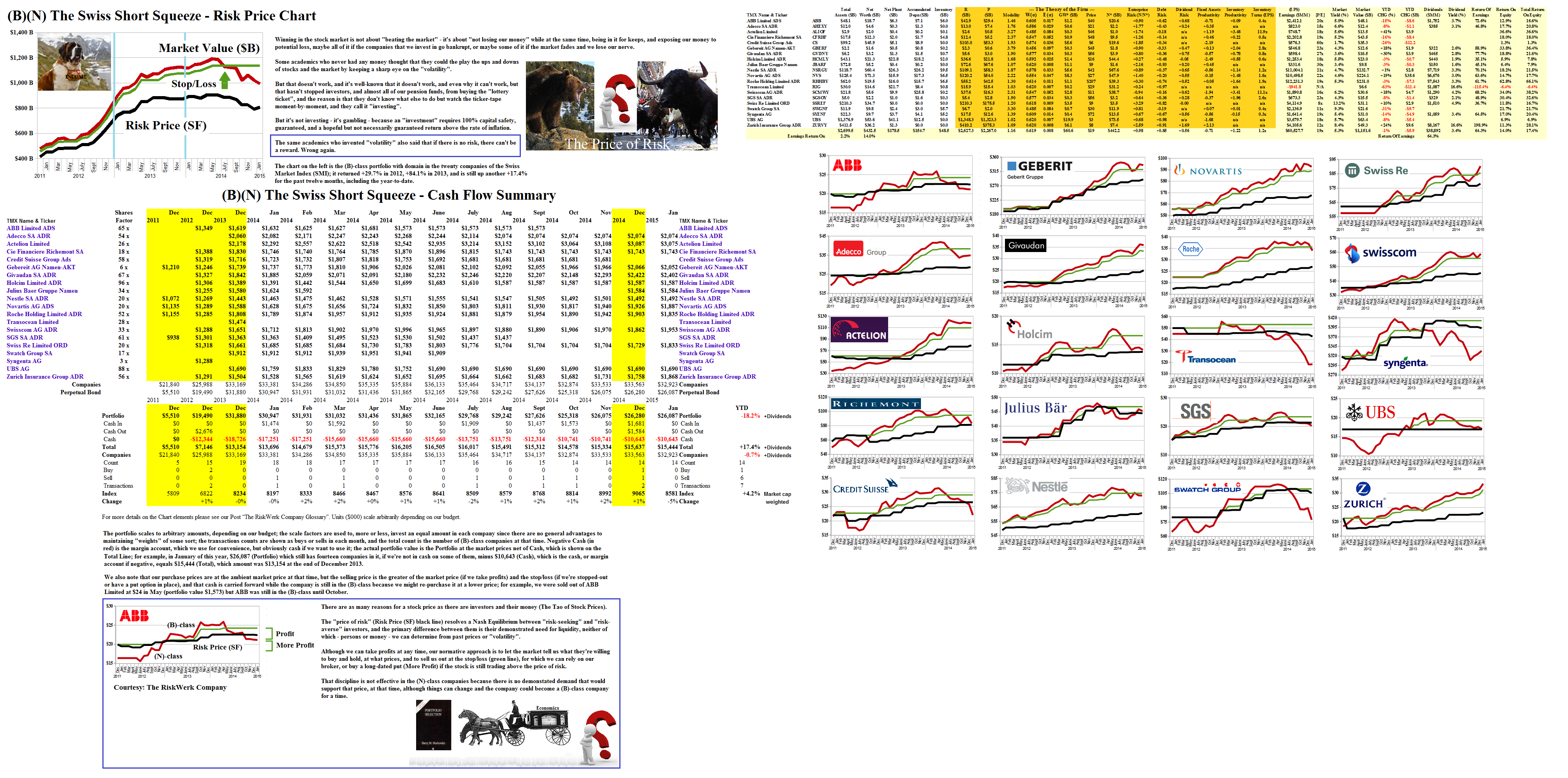

Exhibit 1: (B)(N) The Swiss Short Squeeze – Risk Price Chart

Figure 1.1: (B)(N) The Swiss Short Squeeze – Risk Price Chart

For more examples from the Euro Area, please see our Posts “(P&I) The One World Food Bank” and “(P&I) The World Trader’s Almanac“, and for the Country Risk, “(P&I) The NYSE Mittelstand“.

And for more information on real “risk management” in modern times and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary and “(P&I) Dividend Risk and Dividend Yield“, and our recent Posts “(P&I) The Profit Box” and “(P&I) The Process – In The Beginning“; and we’ve also profiled hundreds of companies in these Posts and the Search Box (upper right) might help you to find what you’re looking for, such as “(B)(N) TLM Talisman Energy Incorporated” or “(B)(N) ATHN AthenaHealth Incorporated” or “(B)(N) PETM PetSmart Incorporated“, to name just a few.

And for more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice. And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

And for more on what risk averse investing has done for us this year, please see our recent Posts on “(P&I) The Easy (EC) Theory of the Capital Markets” or “(B)(N) The Easy (EC) Theory of the S&P 500“, and the past, The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.