(B)(N) The King Has Left The Building

The King has left the building.

Drama. In times of uncertainty, we’re minded of Shakespeare’s famous opprobrium “Cowards die many times before their deaths/The valiant never taste of death but once.” (Julius Caesar, Act 2, Scene 2) and Mr. Shakespeare was himself a very successful investor in ventures of all sorts, in risky times, and only fifty years before Charles I of England lost his head in 1649 with no resting place that he didn’t already “own”.

And our problem today is that many investors don’t know what to do when the free lunch in government bonds is over and they are now heaped with all kinds of anxieties for matters in which the outcome is quite clear, and that’s also a problem.

For example, what should we expect from trade sanctions affecting the Soviet World and their trading partners, from the Swiss Franc “ratio”, from the Greeks, and the Ukrainians, and the price of oil, and the price of the Euro (Reuters, January 26, 2015, How Draghi got divided ECB to say ‘yes’ to money-printing)?

Exactly – we all know the answer – we’re seeing a massive transfer of “paper wealth” in stocks, bonds, and currencies because governments can’t, or won’t, pay for it anymore.

But our defense is still the same and it’s the only one that we have – an “investment” requires 100% capital safety and a hopeful but not necessarily guaranteed return above the rate of inflation – anything else is just a gamble and that’s what worries them because nothing is known about the prices of stocks, bonds, and currencies except what they are every minute of every day.

And the bondholders have no defense at all.

Wealth Transfer in the Deflationary Economy

Figure 1: The End of Risk

But not to worry – if we know what an investment really is, as above, and apply it, then we can walk to the very edge of the Alpine slopes with the sure-footedness of a mountain goat with wings in the event of an avalanche and an earthquake in the foothills.

The illustration on the right, Figure 1, is the good news for bondholders, and Exhibit 1 and 2 below have many examples drawn comprehensively from the amazing companies of the Dow Transports and Utilities, both of which are much better than bonds in all weathers, but they carry only $1.2 trillion in market value and provide a meager income of only $38 billion, some of which which they’ll need themselves, and they’re going fast – like hot dogs – in the burgeoning economy of the Republic.

A “deflationary economy” – and most of the world is deflationary at the present time – provides a huge opportunity to acquire real wealth in investments and businesses in countries with an inflationary economy relative to our own and it is for exactly that reason that stock market prices tend to become very high in a deflationary economy – it is due to the high cost of acquiring an income in a deflationary economy – for which the cure is itself “inflationary” with respect to the money that we once held in government bonds for which the governments are now paying next to nothing and “printing money” as they see fit (The Guardian, January 27, 2015, Davos is starting to get it – inequality is the root cause of stagnation).

The ground has shifted (ibid, The Guardian) and the idle money of the wealthy in government bonds and cash or commodities is not “safe” anywhere because “the King has left the building” and the “smart” money that bet on him and thought nothing has changed got crushed on Thursday last in Switzerland and the “dumb” money that prays for his return is now to follow.

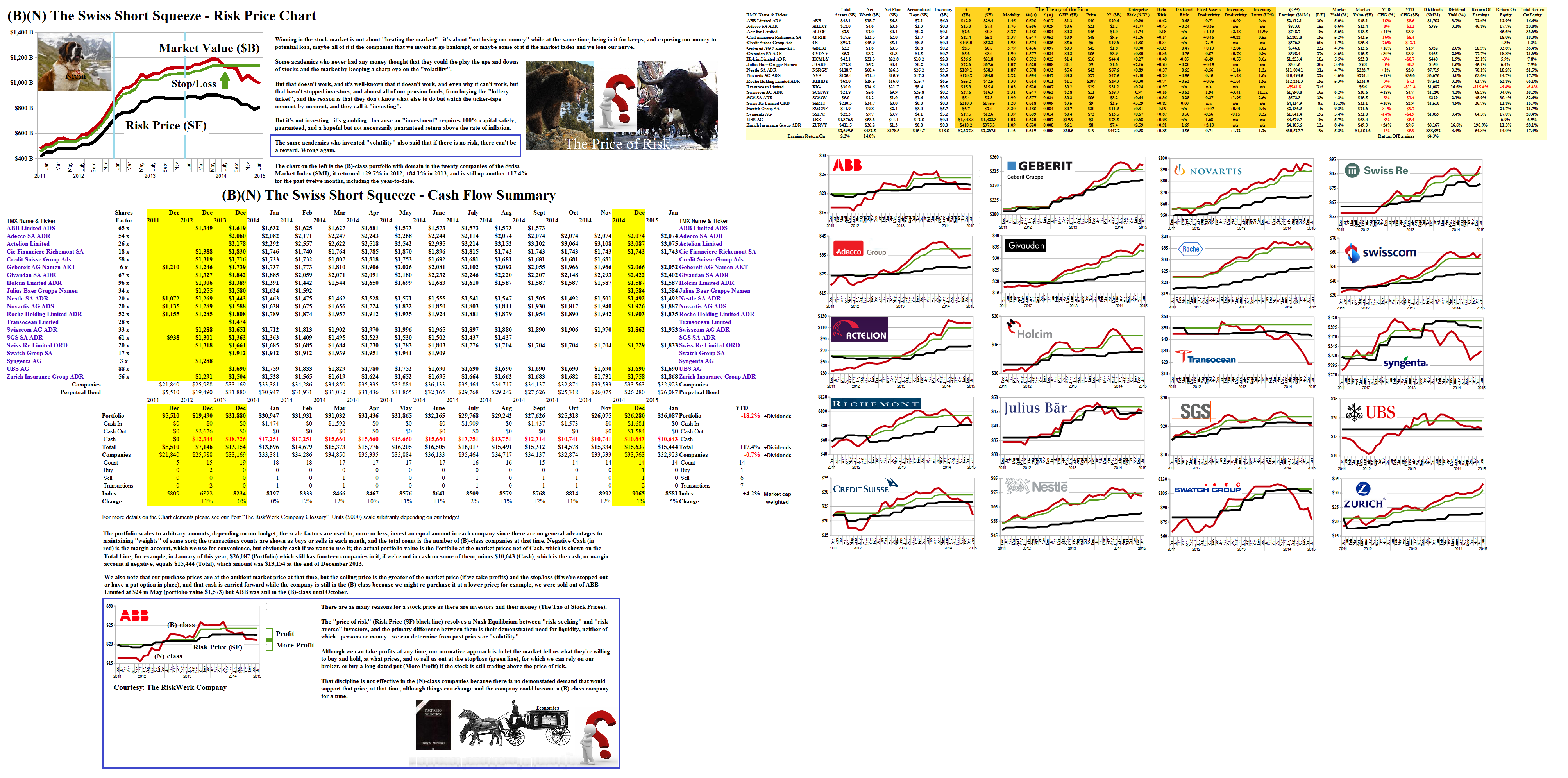

Figure 2: (B)(N) The Swiss Short Squeeze

Nor are we surprised; for example, the Swiss market lost about 14% (SMI 9108 to 7800) in one day, January 15, but has already recovered nearly half of that loss to close at 8400 today and a Swiss Franc is still a Swiss Franc but worth 20% more in Euros than a week ago and the Euro Area economies are also deflationary and the price of equities will rise as the well-heeled investors who are rich in cash, bonds, and derivatives look for a real income to pay their bills in the absence of the divine right.

The End of Risk

In all of that chaos and the uncertainty of the last year, the (B)-class companies in the twenty companies of the Swiss Market Index (SMI) gained +82% in 2013, +19% last year and are up another +6.5% post-tsunami (a ratio) and we’re still holding thirteen of the twenty companies in our portfolio, and the companies know what to do (Bloomberg, January 23, 2015, Nestlé Spent $100 Million on Buyback as SNB Ended Cap); please see Figure 2 above for a re-cap from “(B)(N) The Swiss Short Squeeze“.

And how about the US Market (Bloomberg, January 27, 2015, U.S. Stocks Plunge Nearly Three Hundred Points) on the same news; we can’t help them but the (B)-class portfolio in the Dow Transports was up +59% in 2013, +64% in 2014, and another +6.4% so far this year, and we’re holding twenty of the twenty-two companies that are in it.

“Practical men, who believe themselves to be quite exempt from any intellectual influences, are usually the slaves of some defunct economist.” — John Maynard Keynes 1936

Our subtitle “The End of Risk” is disturbing to many investors who believe that if there is no “risk”, particularly as “volatility”, then there can’t be a reward either.

But that’s simply not true – and it won’t be the first time that falsehoods have become widely accepted and acted upon – and volatility is easily defeated by using the common, public, and cheap facilities of an equities market.

“Investing” is not about “taking risks”, least of all “volatility risks” which are not risks at all; it is about knowing that there are risks, and what they are, and avoiding them, but investing anyway.

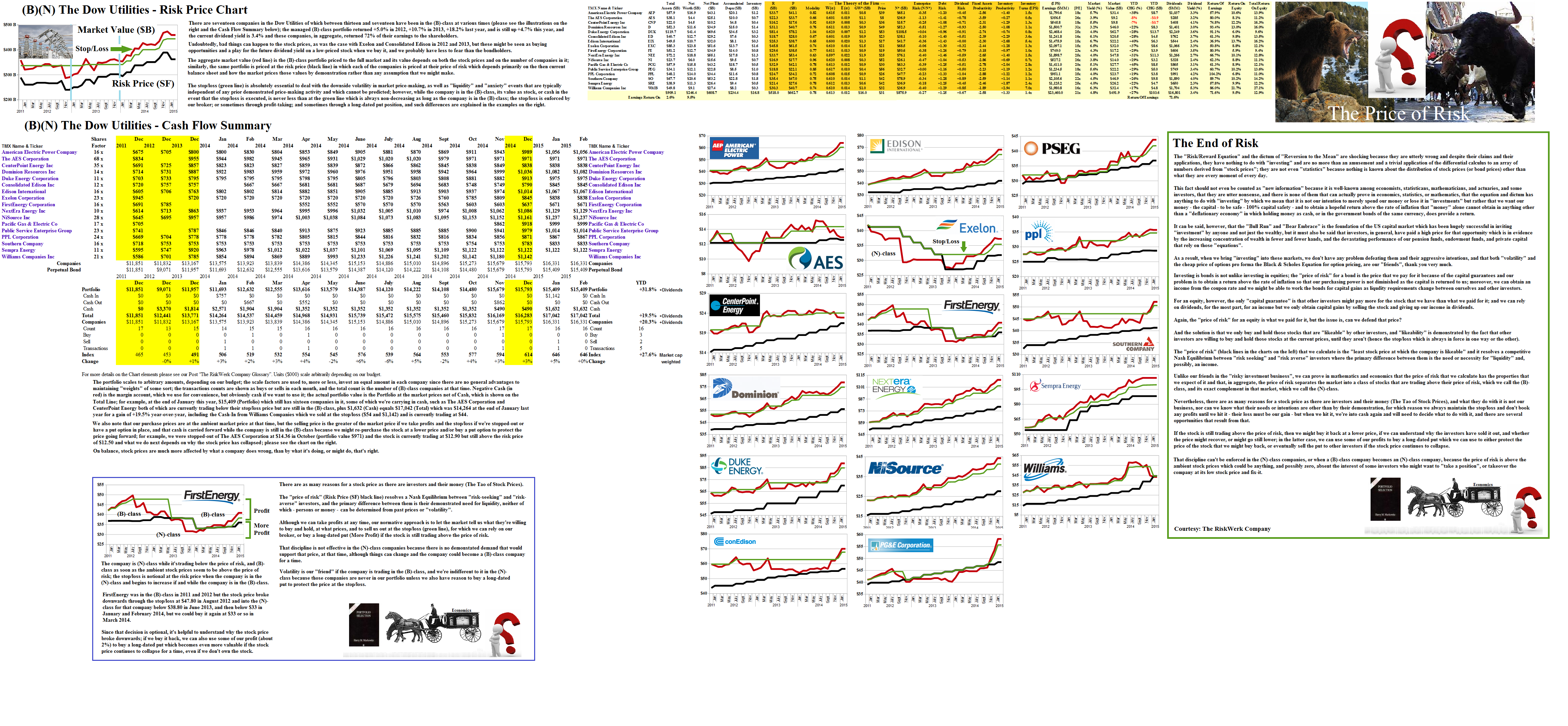

An “investment risk” is that we might not get our money back – we want 100% capital safety – or that we might not obtain a return above the rate of inflation, which is just another way of losing our money – so we want a hopeful but not necessarily guaranteed return above the rate of inflation – and with that in mind, and with due attention to the craft, that’s exactly what we get with no risk; please see Exhibit 1 and 2 below for more details on how that is done and copius examples from the current Dow Transports and Utilities that are in the game.

And we also note that avoiding risk has nothing to do with dumping our money into an index fund or giving our money to a mutual fund or portfolio manager who refuses to guarantee the capital and might also not hold out a plausible hope for a return above the rate of inflation both of which we can get for nothing by buying the government’s Real Return Bonds (RRBs or TIPS) which are illiquid but “cheap” right now and a hedge against rising prices for consumer goods and services that is soon to follow in the otherwise deflationary economy (The Globe and Mail, January 29, 2015, Canadian dollar sinks ever deeper: ‘There will be consequences’).

Exhibit 1: 100% Capital Safety in the Dow Transports

Figure 1.1: (B)(N) The Dow Transports – Risk Price Chart

Exhibit 2: 100% Capital Safety in the Dow Utilities

Figure 2.1: (B)(N) The Dow Utilities – Risk Price Chart

For more information on “the end of risk”, please see our Posts and use the Search Box in the upper right-hand corner for any topic of interest.

And for more information on real “risk management” in modern times and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary and “(P&I) Dividend Risk and Dividend Yield“, and our recent Posts “(P&I) The Profit Box” and “(P&I) The Process – In The Beginning“; and we’ve also profiled hundreds of companies in these Posts and the Search Box (upper right) might help you to find what you’re looking for, such as “(B)(N) TLM Talisman Energy Incorporated” or “(B)(N) ATHN AthenaHealth Incorporated” or “(B)(N) PETM PetSmart Incorporated“, to name just a few.

And for more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice. And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

And for more on what risk averse investing has done for us this year, please see our recent Posts on “(P&I) The Easy (EC) Theory of the Capital Markets” or “(B)(N) The Easy (EC) Theory of the S&P 500“, and the past, The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.