(P&I) The Profit Box

RiskWelt Courtesy: The RiskWerk Company

Essay. “The Profit Box” is a result of the Theory of the Firm, and it figures prominently in assessing bank liquidity and credit risk, and the ability of any company (or country, or economics, or person) to be, or remain, a “going concern” within its demonstrated process.

That sounds pretty basic – we all want to know that (please see the map) – but this is a serious business because the “tools” that are in common use for understanding business viability and risk management are, at best, a “circumlocution” for the Profit Box, and they are, generally, ineffective and indeterminate, with no provable foundation.

But they could be re-cast in those terms, the Profit Box, should someone want to do it – and stop “stuttering” and “mumbling”, so to speak, of which Basel III and “EuroPlan“, are not exceptions (Business Insider, August 10, 2014, Europe’s Huge Failure Is About To Be On Full Display).

We’re not going to do it, but we can explain the Profit Box in more detail, to help said “someone”, should they still want to do it.

The Process

The In Process Game

There is always a “process” if we can make a distinction by merely “counting”, and there is a “conservation law”, of which the balance sheet, energy, and entropy are examples; please see “The Process” for more details, and the proof.

That remains true even if the “conservation law” is a political one that proscribes the “demonstrated societal norms of risk aversion and bargaining practice” and, as such, it is a “higher law”, with consequences that we can measure, now, so that we don’t need to wait for the end of the five-year, or thirty-year, plan to discover the outcome.

Because there is a “distinction” and a “conservation law”, we can develop a σ-algebra, (N), from any examples of the “process elements” which, in this context, we usually call sets of “payables”, (a) or (P), and “receivables”, (b) or (R), with a probability measure in (N), a=p((a)) and b=p((b)), so that our “configuration space” of observables is mapped to the “process space”, 0≤a,b≤1, which is a “state space”.

The sets, (a) and (b), that are developed in the σ-algebra, (N), are always quite complicated, despite their humble beginnings as, for example, countable sets of observations of a company’s payables and receivables, and they will always have the power of the continuum if their measure (or probability) is greater than zero, and they are, in fact, “fractals” with a computable Hausdorff dimension that is proportional to their modality which, it turns out, is also the entropy of the process; please see our Post, “(P&I) The Process – Commensurability” for more information.

Management decisions can affect the outcome of the “Profit Box” (please see below), but these decisions are necessarily countable and, therefore, “random” and of measure zero, but they can also change the modality if the new sets of payables or receivables are systematically different from the old sets.

As a result of the σ-algebra, (N), there are four equations of state in the process space of the process and its “trading connections”.

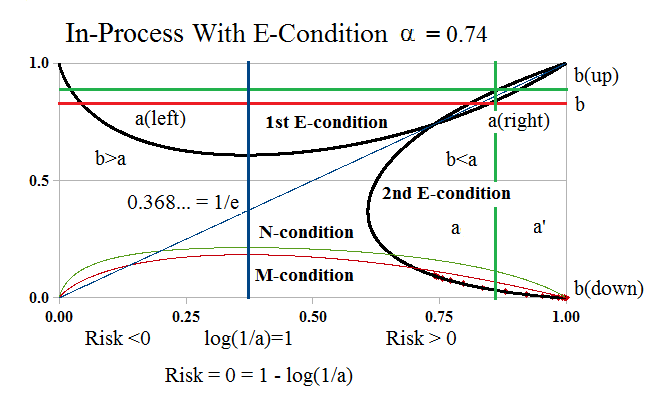

Figure 1: In-Process Company B with α=0.74

The first two are the 1st and 2nd E-conditions, a×log(a) = α×log(b) and b×log(b) = α×log(a), respectively, and they describe what it means to be “in-process” with modality (α), 0<α<+∞, and they are consequences (not assumptions or hypotheses) of our first two assumptions, that we can make a distinction by counting and that there is a conservation law; please see Figure 1 on the left for an example with α=0.74 (which is a Company B modality, 1/e<α<1).

Figure 2: In-Process Company B At End-Of-Process

The other two equations of state are the M-condition and the N-condition which are necessary and sufficient to describe the “end-of-process” and the delivery and receipt of “product” at the end-of-process, in such a way that the process doesn’t end with the delivery and receipt of product, in-process; these are “state equations” that are determined by the “entropy” which is the modality, α, and as such, defines the “arrow of time” as something more than just “tick-tock”.

Please see our Posts, “(P&I) The Process – Entropy Risk” and “(P&I) The Process – System Dynamics” for more information, and the Company A, B, C, D, and E end-of-process descriptions for how the end-of-process is decided.

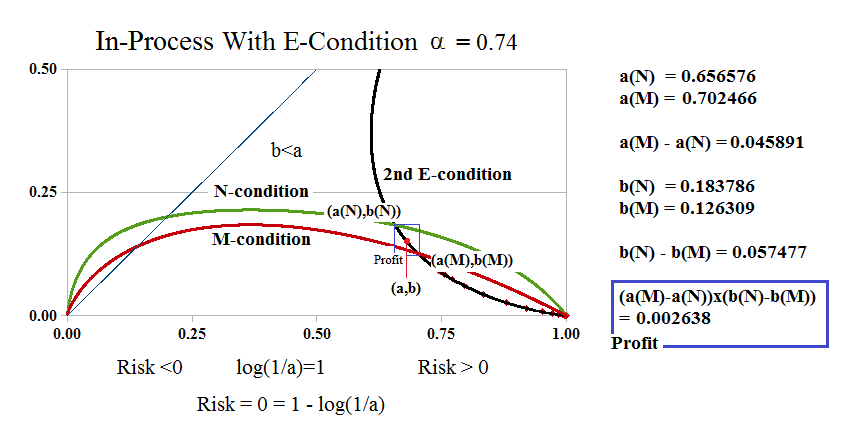

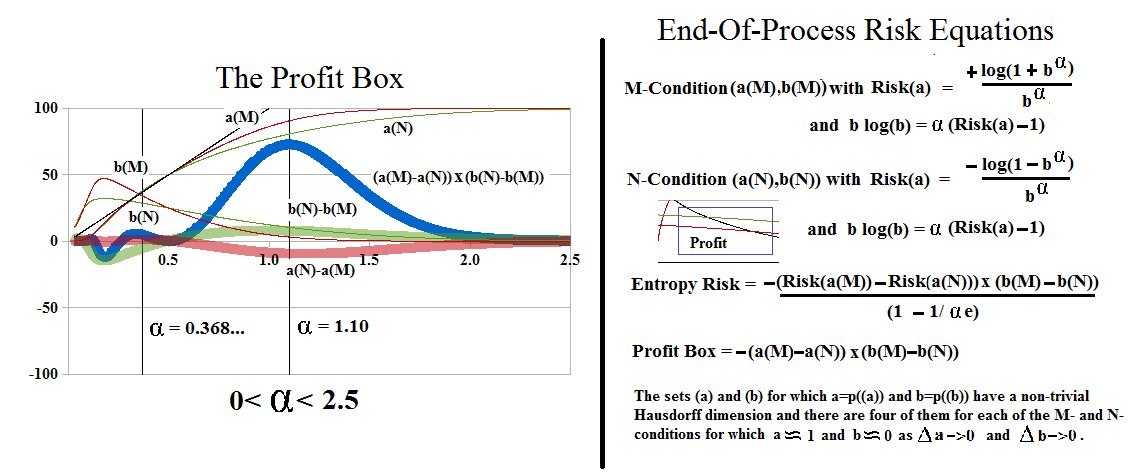

The Profit Box

The process “profit” is always decided by the M-condition at the end-of-process – that is the default – but the N-condition defines an in-process solution in which the producer payables, a(N), are less than the producer payables, a(M), and the producer receivables, b(N), are greater than the producer receivables, b(M), at the end-of-process.

Figure 3: In-Process Company B At End-Of-Process Profit Box

Hence, with a few exceptions which we’ll describe below, the producer and the customer (the trading connections) always have an opportunity to negotiate a “price” for his product, in-process, and that price is always defined as a set of payables, (a), with a=p((a)), for which a(N)≤a≤a(M), and a set of receivables, (b), with b=p((b)), for which b(N)≥b≥b(M), where, as usual, a(M)=p((a(M))), for example, refers to the measure, or probability, of a set of payables, (a(M)), and similarly, for the sets (a(N)), (b(N)), and (b(M)), in our usual notation; please see Figure 3 on the left.

Moreover, there may be an incentive to do so, depending on the liquidity and credit concerns of either, or both, the producer and the customer, in-process.

Of course, “random” profits can always be negotiated, but they are not necessarily in-process and would, therefore, solve only a “temporary” or “ambient” problem – such as “too big to fail” – or, possibly, change the modality – legislation and regulatory action – if the process is not working for them; it’s also noteworthy that any set of measure zero can be added or taken out of a set of payables or receivables without changing the modality, or the process.

Remove the bandage, please.

In other words, “band-aids” and “quick fixes” with no foundation, don’t help if surgery is required; please see, for example, our recent Post on “(P&I) The Banker’s Modality” or the demise of “(B)(N) ABL African Bank Investments Limited“.

The Profit Box is defined by the solution to the end-of-process “risk equations” which are “set equations”, that is, they are about sets of payables and receivables (not “points”) that must be formed in-process in the process space of the producer and the process space of the “customer” (their trading connections), subject to the 1st and 2nd E-conditions.

Figure 4: The Profit Box

The “process” spaces are also reflections of each other, but the “producer” space may be regarded as the “real object” that demonstrates control over the payables sets, (a), whereas the trading connections, (b), have deeper resources, but less control over them because the sources of their receivables are disparate and independent; please see Figure 4 on the left.

We’ve “oriented” the Profit Box to that of the producer which means that less payables, a(N) < a < a(M), and more receivables, b(N) > b > b(M), are preferred, in-process.

However, that preference is only available to the producer if his modality, α>0.5; at α=0.5, the Profit Box “shrinks” to zero, and there are no choices that can be made but to accept the outcome which is a(M)=a(N)=0.50 and b(M)=b(N)=0.25 in the process co-ordinates, which we have scaled as the “unit”, 1=100 “basis points” in Figure 4 above; in general, the “units” are arbitrary, but always relative, and the Profit Box is always in the same “scale” as the units (not “squared”) because there is only one degree of freedom, in-process.

For 0<α<0.5, it’s more interesting (and probably necessary) to think of the process and the modality as emerging from “nothing” at α=0 to some tenuous “life” at α>0, but we note here that the Profit Box increases slowly to 5.5291169 basis points at α=0.337, and then descends slowly to zero at α=0.262379…, and that the essential changes are due to disappearing “flexibility” with respect to the payables set, a(N)-a(M), which is always positive for these α, 0.262379<α<0.337<0.5, but vanishes at these two points, whereas the receivables set, b(N)-b(M), is always negative until α<0.079879, and these changes in “outlook” occur when the company owes (P) twice (α=0.5), three times (α=0.337), and four times (α=0.262379) what is owed to it (R).

J.S. Bell, Cambridge University Press, 1987.

What happens at α=0 and a=b=0, is “not knowable”, or as John Bell FRS, the physicist, would say, it’s “unspeakable”, but we should not assume that the sets, (a) and (b), of measure zero, have no content, because, after all, we started with a finite and countable set of events, which had a finite and non-zero measure summing to one, but have zero measure in the σ-algebra that they generate.

The Profit Box for modality, α, emerging from α=0, has “substance” which is like a “wave” that results from “braiding” in which the a(M) and a(N) solutions change their relative position, as well as the b(N) and b(M) solutions on a different track, so that the Profit Box “oscillates” between tiny positive and negative values, with huge relative values as more events are realized, until it obtains more “substance” at α>0.024879; for the details of the solution please click on the link “Solution of the Risk Equations“.

For more information and additional guides to the theory, please see our Posts “(P&I) The Process – The 1st Real Dollar” which shows how a “currency” gets its value from the “subsistence economy” at the Company D modality, and “(P&I) The Process – The Guns of August” which explains how that modality actually “works”.

For more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice. And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

And for more information on real “risk management” and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary; we’ve also profiled hundreds of companies in these Posts and the Search Box (upper right) might help you to find what you’re looking for.

And for more on what risk averse investing has done for us this year, please see our recent Posts on The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.