(B)(N) ABL African Bank Investments Limited

So, you say you’re a bank?

Drama. In its short life, African Bank Investments Limited, has never been a “bank”, although it seems to have been heading in that direction; please see Exhibit 1 below (Bloomberg, August 10, 2014, African Bank Splits to Isolate Loans During Rescue).

Most of its funding is a long-term bond, but to be a bank, it needs customer deposits and, for those, it needs “deposit insurance” and, in this case, might consider offering their customers a higher rate of interest, something that they can’t get through their own endeavors; and it also needs to make profitable loans to customers and small businesses, and not tie-up its capital in “long term investments” – a furniture company? And unsecured and non-performing personal loans and credit cards.

Where are the regulators when you need them, before the collapse?

Exhibit 1: The Bank’s Non-bank Modality

Figure 1.1: ABL African Bank Investments Limited – Modality

We don’t really need to bring out the “big guns” for this (please see our recent Posts, “(B)(N) The Canadian Bank Act” and “(P&I) The Banker’s Modality“) because the “Profit Box” increases only linearly if the modality is α>1.1, and that’s typical of “investment companies”.

In this case, the modality was about α=1.5 in 2010, and has been worked down to the current α=1.17; please see Figure 1.1 on the left.

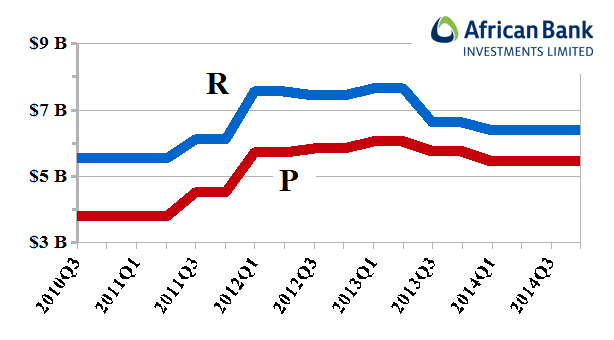

Figure 1.2: ABL African Bank Investments Limited – R P

However, it’s because (R) “what is owed to the company” is converging towards (P) “what the company owes”, and that’s not because it’s becoming “more selective” about depositor accounts; please see Figure 1.2 on the left.

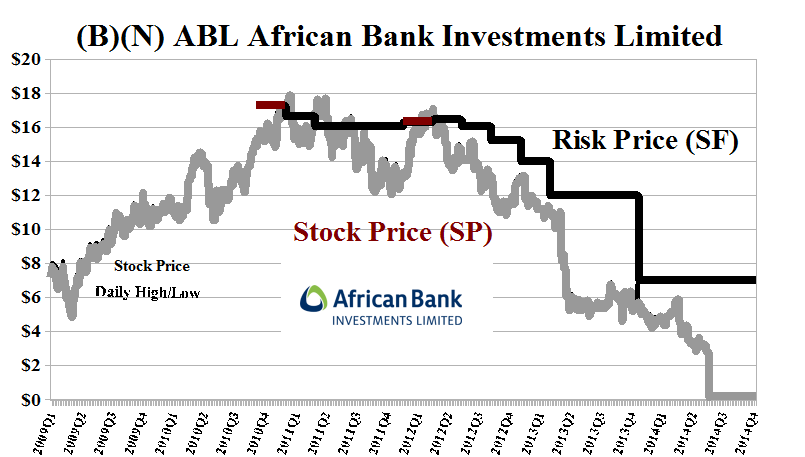

Pity that investors who paid $14 for the stock just two years ago, and were maybe “harvesting” the dividend yield in excess of 5%, can only get $0.14 for it on Monday; please see Exhibit 2 below.

Exhibit 2: (B)(N) ABL African Bank Investments Limited – Risk Price Chart

ABL African Bank Investments Limited

African Bank Investments Limited is a bank. The two underlying operations of the company are unsecured credit and retail & furniture and appliances retailing environment. It operates through two primary businesses, African Bank and EHL.

From the Company: African Bank Investments Limited, through its subsidiaries, underwrites unsecured credit risk through the provision of personal loans to the formally and informally employed residents. The company offers personal loans, overdrafts, credit cards, and vehicle finance. It also provides credit life policies to customers who utilize the loan and credit card products offered by African Bank, as well as funeral insurance products. The company is also engaged in the retail of furniture and appliances, and provision of related services under the Ellerines, Beares, Furniture City, Dial-a-Bed, Geen & Richards, and Wetherlys brands. It has operations in the Republic of South Africa, Zambia, Botswana, Lesotho, Namibia, and Swaziland. The company was formerly known as Theta Group Limited and changed its name to African Bank Investments Limited in 1999. African Bank Investments Limited has 13,000 employees and is based in Midrand, South Africa.

Appendix: The Non-Performing Loan Portfolio

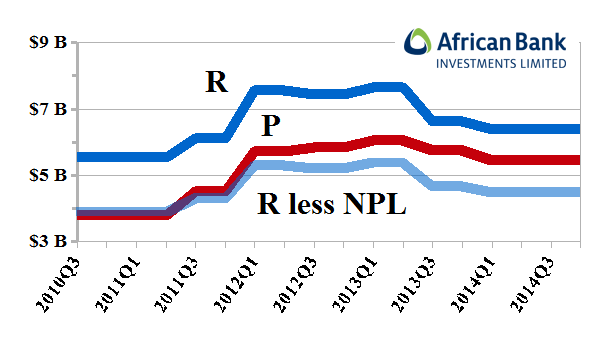

Figure 3.1: ABL African Bank Investments Limited – Modality with (R less NPL)/P

The bank has estimated that it’s non-performing loan portfolio (NPL) is 30% of its total assets.

That’s an astonishing number but the bank attributes previous loan practices and the South African economy as the cause of its problem; please see Figure 3.1 and 3.2 on the left.

Figure 3.2: ABL African Bank Investments Limited – with (R less NPL)

It also creates a liquidity problem (payables) because the bank isn’t making any money on these loans, and a credit problem (receivables) because the money might not come back, and it has the same effect as “inventory on the shelf” which drives the “private modality” from α=1.17 (by the book) to α=0.8; please see our Post, “(P&I) The Banker’s Modality” for more information on what that does to profits.

And for more information and additional guides to the theory, please see our Posts “(P&I) The Process – The 1st Real Dollar” which shows how a “currency” gets its value from the “subsistence economy” at the Company D modality, and “(P&I) The Process – The Guns of August” which explains how that modality actually “works”.

For more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice. And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

And for more information on real “risk management” and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary; we’ve also profiled hundreds of companies in these Posts and the Search Box (upper right) might help you to find what you’re looking for.

And for more on what risk averse investing has done for us this year, please see our recent Posts on The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.