(P&I) The NYSE Mittelstand

Figure 1: World Consumption

Drama. The American “Mittelstand” of mid-sized companies of all sorts is the world’s fifth-largest economy, and we can imagine it as chugging-away every day in the USA producing products for consumption at home and abroad, profits for its owners, and jobs – which is what it’s all about.

And while America chugs, Wall Street “pumps” (please see our recent Post “(B)(N) What’s A Girl To Do?“) and it’s been pretty good at creating under 30’s billionaires in the last fifteen years or so, and a side-benefit is increased investor liquidity – in and out fast – to launch new ventures in a way that is similar to “banking”, but with bigger “chips” and a different skill-set (Bloomberg, October 29, 2014, Why the US can take on Germany at its own game).

But that’s happening in other countries too; the United States and China account for $30 trillion of the World’s Gross Domestic Product (GDP) of $93.5 trillion, and there are eighteen countries with a GDP in excess of $1 trillion per year, but the “savings rate” – which is the money available for investment – in the United States is only 16% of the GDP, and less than every other country in the world but for the United Kingdom and Turkey; please see Figure 1 above on the right, for a survey of how the world looks today, and Exhibit 1 below for the connection between the “factors of production”, consumption, and the GDP per capita, and how it might look tomorrow.

Exhibit 1: Der Mittelstand – Enterprise Risk & World Consumption

Figure 1.1: Enterprise Risk & World Consumption

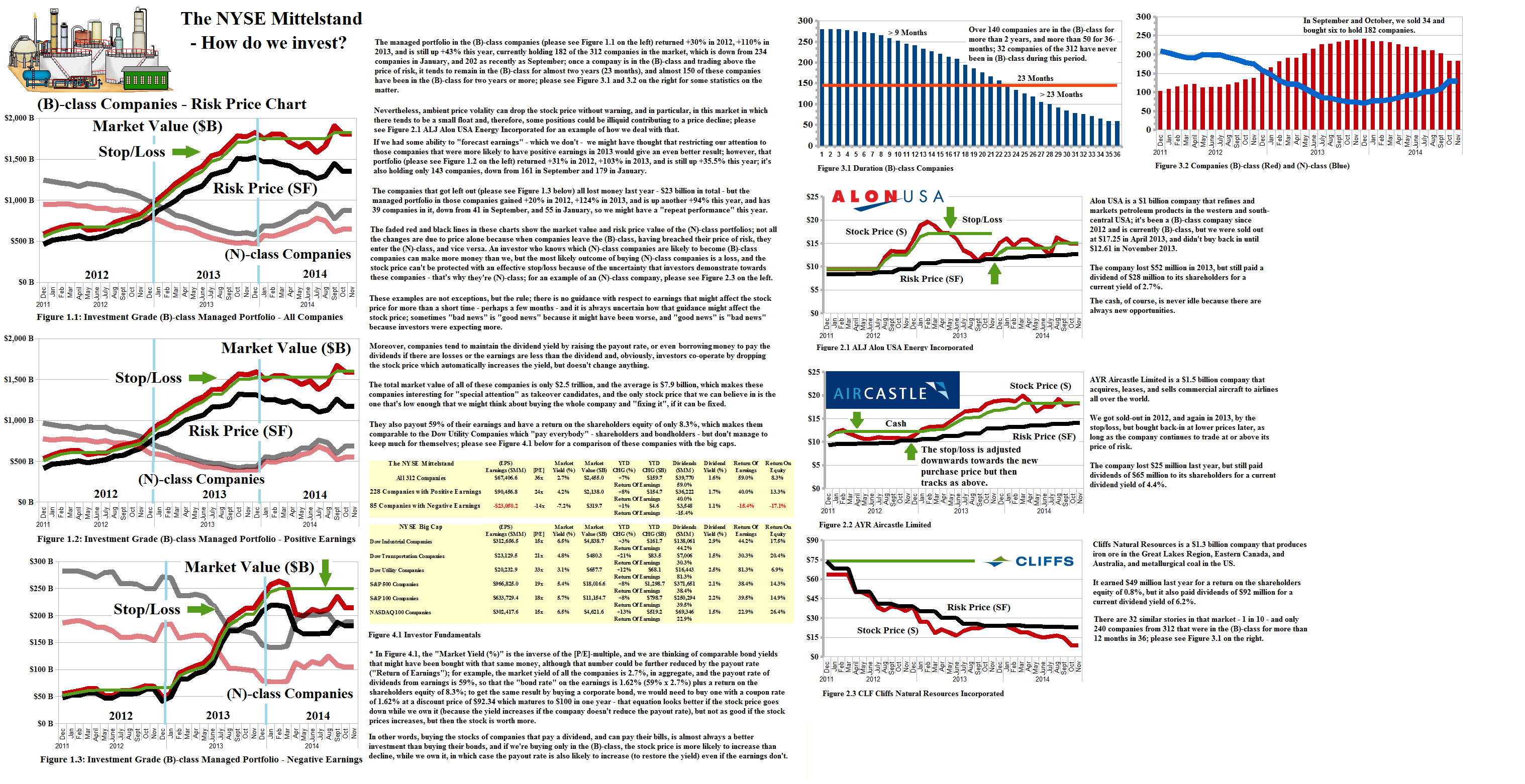

The NYSE Mittelstand

There are, of course, thousands of private and public enterprises in the US, but if we look at the NYSE companies that are outside of the Dows, and the S&P 500 and the NASDAQ 100, we have a domain of about 300 landed-companies that can be bought and sold on the public exchange, and these are the survivors of the aforementioned Wall Street “pump” after the down stroke and Wall Street has cashed-out.

But which of them should we buy and sell, and when, and is there any advantage to owning shares in these companies that is different from the big-caps?

We looked at that question in our Post “(B)(N) American Small Caps” and we found that there is indeed opportunity in that class of companies, but if it’s “better” for investors than owning a portfolio of the big-caps, it comes from the renewed activity of the investment bankers and changes of ownership in a faltering business, or an acquisition, that might drive their stock prices one way or the other.

But it doesn’t come from the return on the shareholders equity, or the dividend yield, or the return on the assets, or any other accounting or “value” prescription that we might have, short of owning it, and “fixing it” if it can be fixed; please see Exhibit 2 and 3 below for examples taken almost at random, because it doesn’t seem to matter which box we open.

Nevertheless, the opportunities for investors in the Mittelstand in America are very compelling on a portfolio basis, but we need to consider how it’s working post-IPO, and post-frenzy, and how we might invest in it for the long-term, because the big-cap companies in America are yesterday’s news – they’re getting old, and producing +30% or so returns when managed as a (B)-class portfolio, but only the market returns of +8% or so in the long-term (20 or 30 years if we can stick it out) and ±20% in the short-term (twice in the last fifteen years and maybe again in the next) if managed only for volatility, which is what the Capital Assets Pricing Model (CAPM) and Modern Portfolio Theory (MPT) do, thereby distorting and re-shaping the market according to some “pipe-dreams” of “mean reversion” – which doesn’t exist in our World and, hopefully, not in the rest of it either.

The summary in Exhibit 2 below shows how we manage earnings in the Mittelstand on a portfolio basis in the (B)- and (N)-class companies, for routine double- and triple-digit returns with no risk to the capital, but it also shows how readily “good” can become “bad”, and vice versa, if all we know is an earnings report.

Exhibit 2: (B)(N) The NYSE Mittelstand – Fundamentals

Figure 2.1: (B)(N) The NYSE Mittelstand

Most investors “know” that buying and selling stocks on the basis of “good” or “bad” earnings reports is a loser’s game, but that’s still what’s happening in the broad market dominated by “volatility”-based investment “thinking” and programmed-trades.

We’ve had to use quotes on all of these terms, including “thinking”, because none of them is forward-thinking, and all of them are backwards-looking, either before the purchase, or sale, or after it.

Do you think now?

A better measure than “earnings”, and volatility-defense, but is related to the earnings, is the “Total Return on the Shareholders Equity” (please see the description in Figure 2.1 above) which aims to “shoot it while it’s standing still” rather than while it’s moving, so to speak, but these investments need to be run on a portfolio-basis in the (B)-class, rather than to rely on the “one-off” screaming success, or failure, that we read about in the news every day.

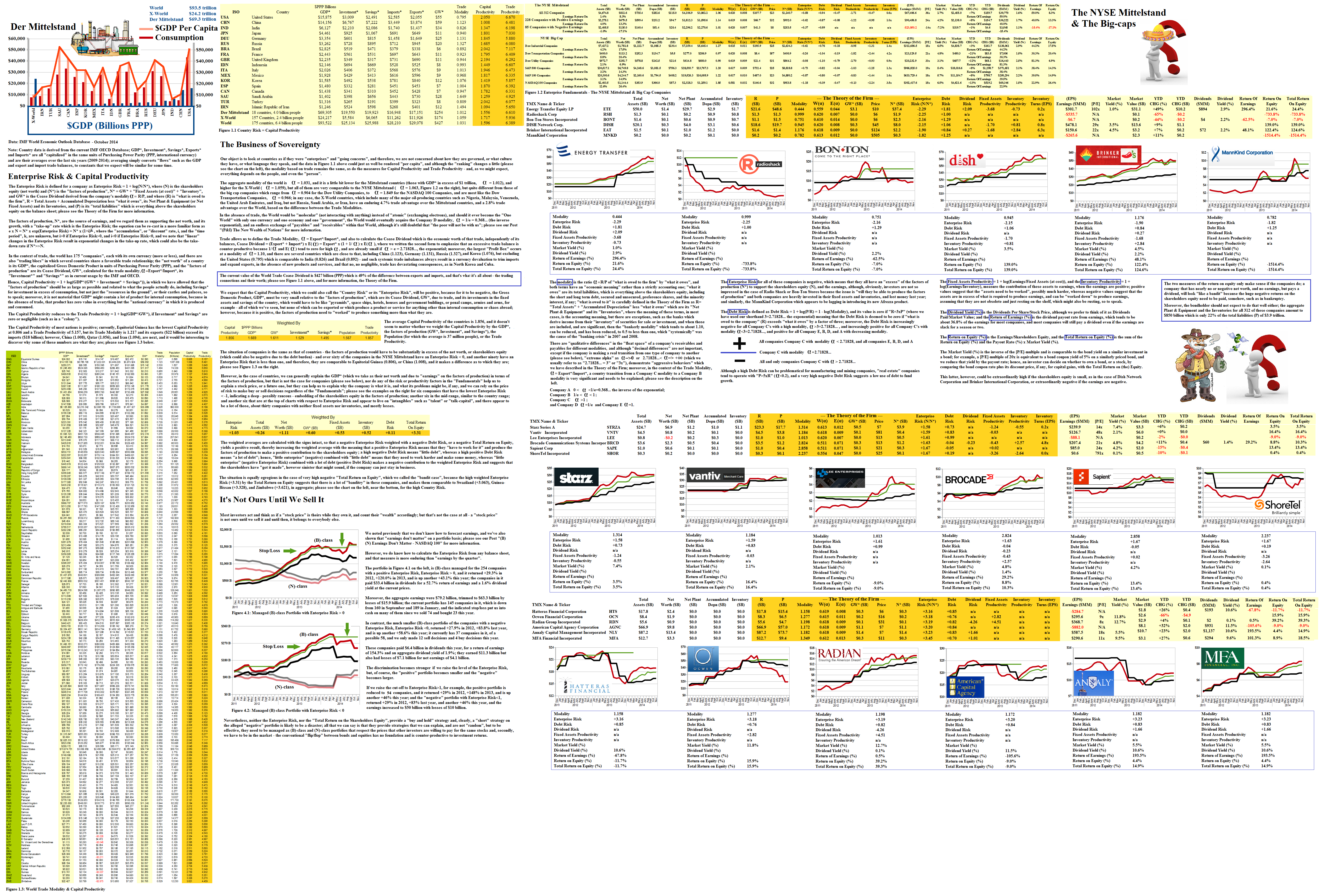

Enterprise Risk & Country Risk

Focusing of “earnings” in the NYSE Mittelstand doesn’t help us to understand how competitive the NYSE Mittelstand (which is the World’s fifth-largest economy) is in the World of up-and-coming economies that are likely to displace it if we don’t pay some attention to the matter.

The measures that they have in common are the Enterprise Risk, which we can also use in evaluating a portfolio of them (please see Exhibit 3 below), and the “Country Risk” which is the same as the “Capital Productivity” of a country, and relies on its Trade Modality, and its investments in the fixed assets and savings of the country for investment, and when the capital is badly deployed, and the trade relationships are weak, we can expect loan defaults, a hungry people, and a change of government akin to a new management; please see Exhibit 3 below which is a “story board” on everything that we need to know.

Exhibit 3: Enterprise Risk & Country Risk

Figure 3.1: The NYSE Mittelstand – Enterprise Risk & World Capital Productivity

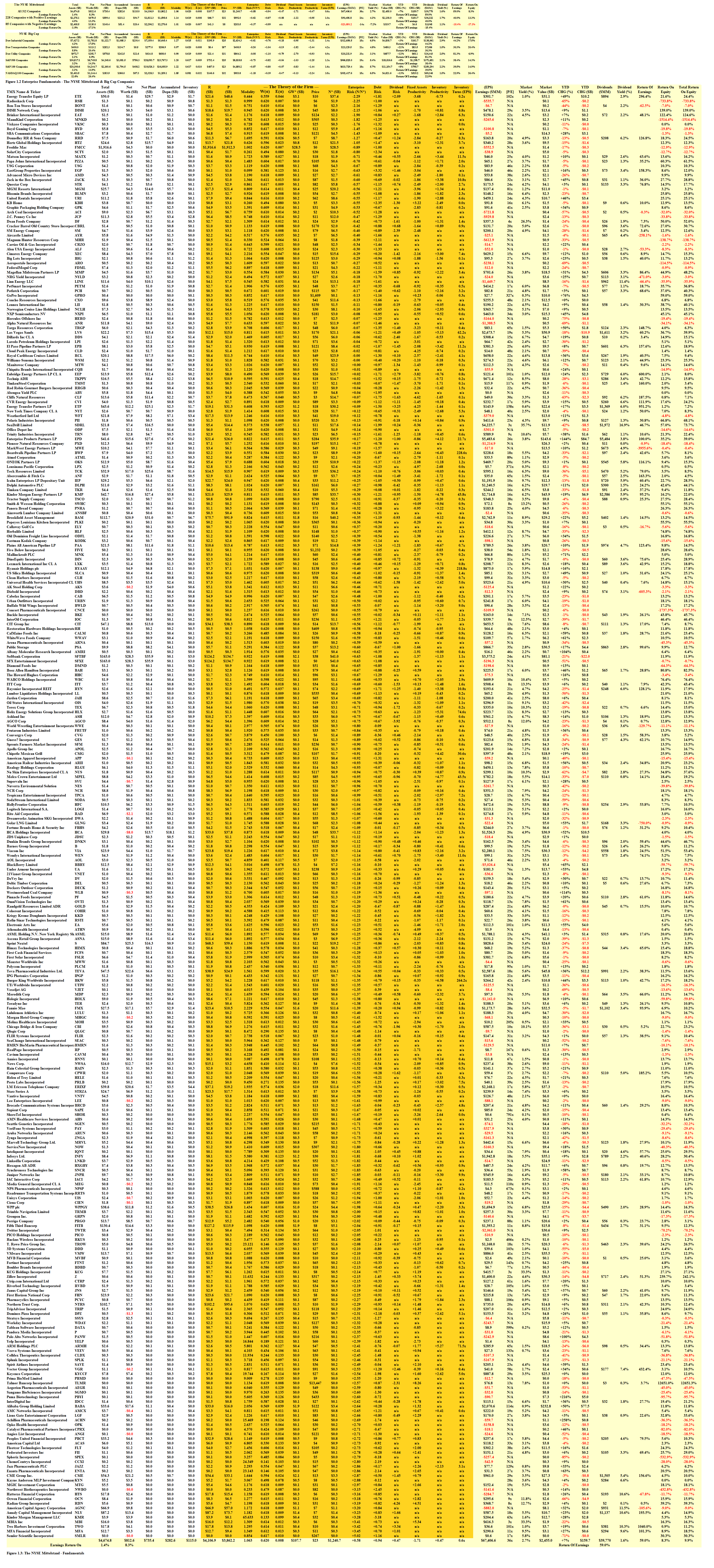

Please click on the link (and again to make it larger if required) “The NYSE Mittelstand Fundamentals” for more details on the companies.

And for more information on real “risk management” in modern times and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary and “(P&I) Dividend Risk and Dividend Yield“, and our recent Posts “(P&I) The Profit Box” and “(P&I) The Process – In The Beginning“; and we’ve also profiled hundreds of companies in these Posts and the Search Box (upper right) might help you to find what you’re looking for, such as “(B)(N) TLM Talisman Energy Incorporated” or “(B)(N) ATHN AthenaHealth Incorporated” or “(B)(N) PETM PetSmart Incorporated“, to name just a few.

And for more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice. And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

And for more on what risk averse investing has done for us this year, please see our recent Posts on “(P&I) The Easy (EC) Theory of the Capital Markets” or “(B)(N) The Easy (EC) Theory of the S&P 500“, and the past, The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.

{kind=link}