(B)(N) American Small Caps

American Small Caps

Drama. There are more than 10,000 public companies listed on the US stock exchanges, but many of them trade over-the-counter (OTC) and have a small float and volume, and they trade like an ADR (American Depository Receipt for foreign-domiciled companies) in terms of the cost of trading them and the information that we can get about them.

Of these, we follow about a thousand American “Small Caps” which are listed on the big boards and have a market value of less than $10 billion, which is an amount that could fit into a lot of budgets that might want to own them.

Folklore has it that these companies are the engines of growth and enterprise, and we don’t expect them to pay a dividend because their money is better than ours.

But the folklore is not quite right because their aggregate return on equity (ROE) is less than 7% in the NYSE, and less than zero (-1.4%) in the NASDAQ, and there are many ways for an investor to get those returns without slogging through a production line or counting the inventory, and we would expect that at least some of these companies are pledging more hope than results.

La Passarola, A Dream by Padre Dr. Bartolomeu Lourenco de Gusmao 1709, Overruled by the Inquisition of the Dominicans.

So we trimmed them down to just those with an ROE between 15% and 30%, which – if it’s attainable now – should be attainable in the future, year-after-year, almost every year, and should not shadow “growth” or “enterprise” that can also be well-funded by debt, and those companies number less than a hundred (91) and have a current market value of only $490 billion, which is less than 2% of the aggregate big board companies; please see Exhibit 1 below, and click on the link for the Fundamemtals.

Positive Bliss

These criteria (it turns out) did create a positive bias to the upside and 2/3rds of the companies have increased in price this year, with more than 1/3rd showing double-digit increases in excess of +12%; selling also seems to be more motivated by liquidity concerns than by market anxiety or aggression, but ten of them have had double-digit price declines, including, for example, Tractor Supply Company (TSCO -17%), Chicago Bridge & Iron Company (CBI -22%), Lululemon Athletica (LULU -25%). and Lumber Liquidators (LL -38%); please click on the links (and again to make them larger if required) “(B)(N) American Small Caps – Prices & Portfolio and Cash Flow Summary” for further details.

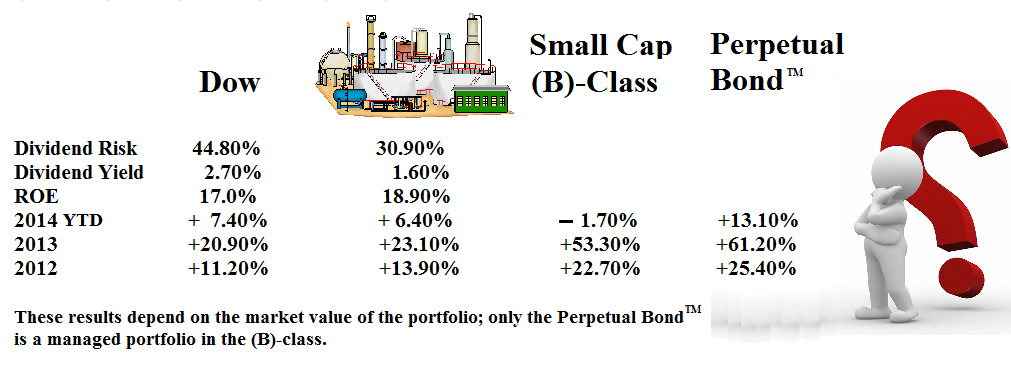

Figure 1: The Benchmark

Despite all of that – which we regard as merely anecdotal evidence – this portfolio, in aggregate, performed similarly to the Dow Industrials last year and this year (please see Figure 1 on the right, and our Post “(B)(N) Through The Looking-Glass” for more information on the benchmark) but, when we managed it as a Perpetual Bond™, we obtained +25% in 2012, +61% last year, and are up +13% so far this year, merely by buying and selling appropriately in the (B)-class companies for which we have more flexibility than in the Dow at the present time, because they’re almost all (B)-class companies in the Dow and have been for most of the last two years; please see the aforementioned links for more details, and Figure 1.1 below.

Exhibit 1: (B)(N) American Small Caps – Fundamentals

Summary American Small Caps – Fundamentals

Figure 1.1: (B)(N) American Small Caps – Risk Price Chart

There are some systemic differences in the small cap stocks for the different markets (NASDAQ, NYSE and Dow Transports); for example, in the modality and the Enterprise Risk, and the price of the Coase Dividend, but none of them, individually or severally, can be said to “drive” stock prices, and we’ll examine the Dividend Risk and Dividend Yield, below, for possible arbitrage opportunities; please see Exhibit 1 for further details.

Our conclusion, of course, is the one that we always have – there is no information in a stock price, or even in thousands of stock prices, nor does any merit in any company suggest one (although a failure might suggest zero), but should we see one for a company that we own, we can defend it, and that’s all that we have to do, and all that we can do; please see below for more on the concept of defense and how it applies to the Risk/Reward Equation.

Figure 1.1, above, shows the portfolio performance for the last several years, and the faded lines show the portfolio performance of the (B)-class companies within that same group of companies; an attentive stop/loss policy (the green lines) is also required in order to protect (defend) our prices, but we will also buy those companies back at lower prices if they’re still trading above the price of risk – which is a “phantom” stock price, and the only one that matters; please click on the links “(B)(N) American Small Caps – Prices & Portfolio and Cash Flow Summary” for further details.

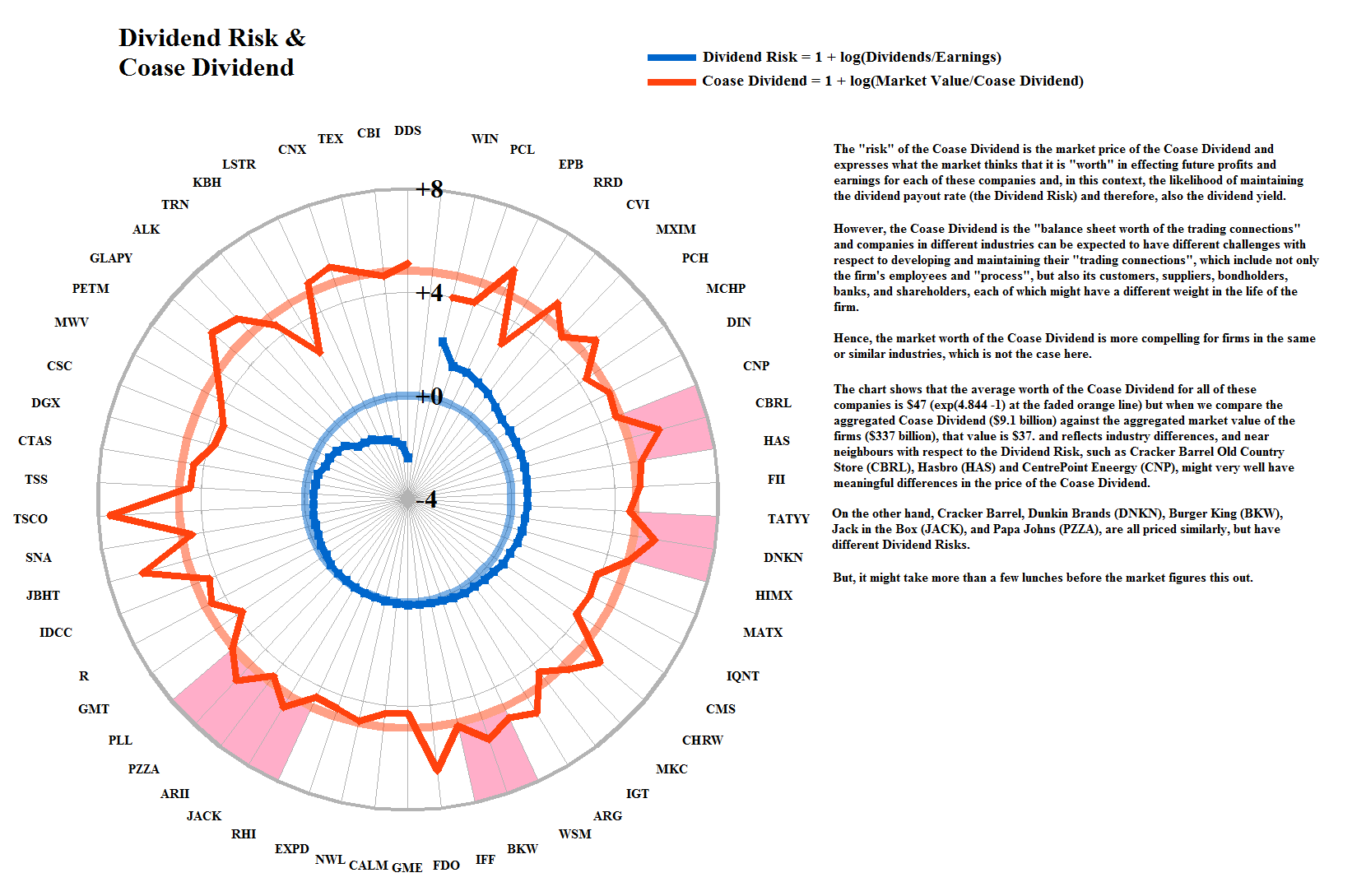

Dividend Risk and Dividend Yield

Exhibit 2: American Small Caps – Dividend and Non-dividend Paying Companies – Fundamentals

American Small Caps – Dividend Paying Companies

Fifty-seven of these companies pay dividends, but the return on equity for the dividend and non-dividend paying companies is nearly the same at 19.3% and 18%, respectively, and again casts some doubt on the notion of “growth” companies making better use of our money than we; the payout rate for the dividend-paying companies is 44% and the aggregate dividend yield is a respectable 2.3% and $7.8 billion last year; please see Exhibit 2 above for further details.

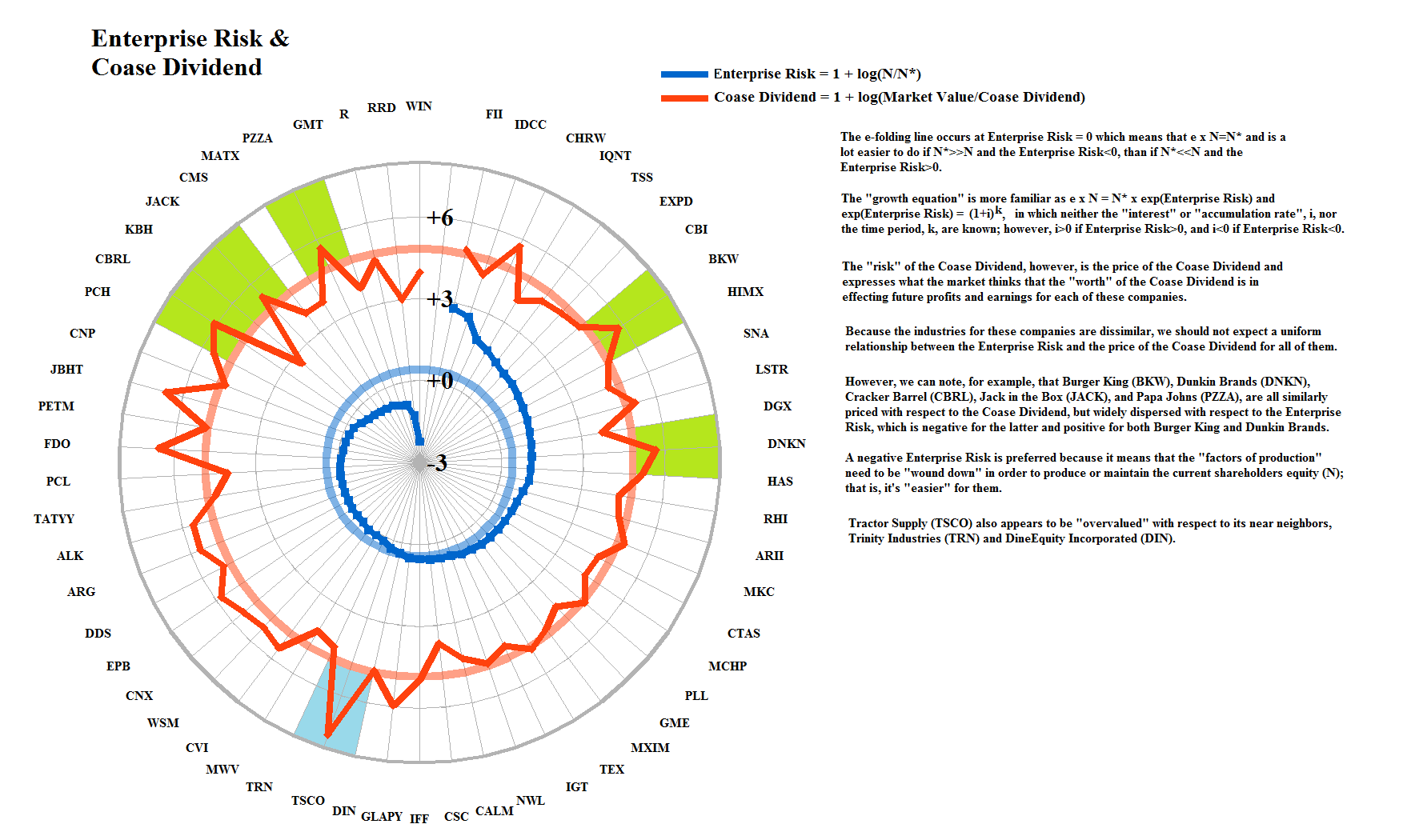

In general, we will buy and hold only those companies that are trading in the (B)-class, and there is seldom sufficient reason to rationally “promote” an (N)-class company into the (B)-class merely on its merits; that’s an all or nothing proposition, but within that class, we can also check the Dividend Yield and the market price of the Coase Dividend against the Dividend Risk for possible arbitrage opportunities that could affect our weights; please see Exhibit 2.1 and 2,2 below; and similarly, the market price of the Coase Dividend against the Enterprise Risk, whether the company pays dividends or not; please see Exhibit 2.3 and 2.4 below.

Figure 2.1: American Small Caps – Dividend Risk & Dividend Yield |

Figure 2.2: American Small Caps – Dividend Risk & Coase Dividend |

Figure 2.3: American Small Caps – Enterprise Risk & Coase Dividend – Dividend Stocks |

Figure 2.4: American Small Caps – Enterprise Risk & Coase Dividend – No Dividend Stocks |

For more information on the chart elements and the “Five Equations of State”, please see our recent Post, “(B)(N) Through The Looking-Glass“ and for the Canadian Small Caps “(B)(N) The Canadian “Hot” Money Stocks“.

The Risk/Reward Equation

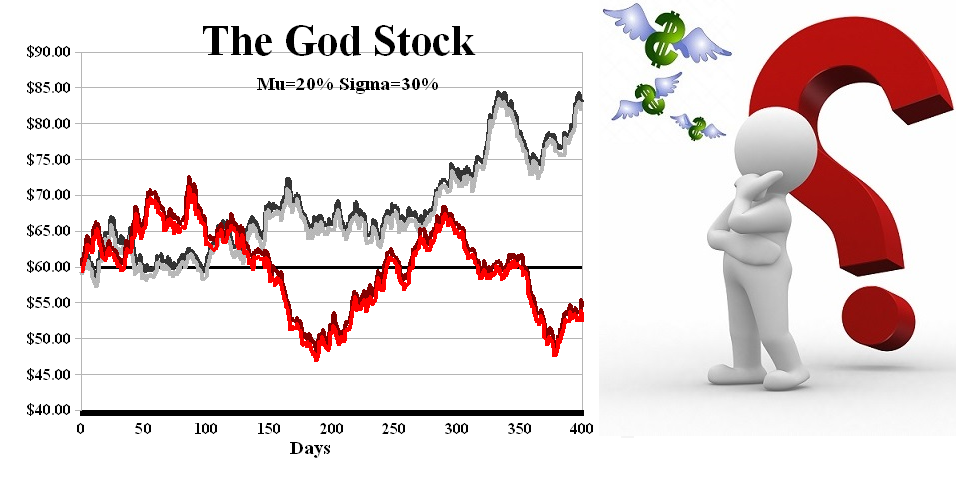

Figure 2: The God Stock Does Not Reward Risk and Investing Is Not A Trial.

It has to be said by nearly everyone in the investment industry that “past performance is not a guarantee of future performance” and the reason that “it has to be said” is that it’s true – very true – and the reason that it’s very true is that these folks who are “selling investments” don’t know anything about the past, except what it was – that is, they know what it was in awesome detail, but they don’t know why it was, and the particular nexus of events that made that past, will never happen again, in just that way – which is a fair statement, even though it doesn’t say anything other than “we don’t know what we’re selling, or what the outcome will be, but this is the deal and it’s all here – in the prospectus“.

As a result, the entire retail investment industry (which customers also include pension plans and endowment funds) has a long-standing dilemma – they need to tell us that we shouldn’t expect to make any money if we buy their “investment” – and it’s more likely that we’re going to lose it, net of their fees and loads – but that’s not a strong sales pitch, and it’s the only pitch that they have as long as they believe in the “risk/reward equation” and its 60/40 or 40/60-defense, with other “weights” as assigned.

Do we need a pilot?

In fact, the same equations that are used to allegedly “manage” billions of dollars in “investments” are also used to computer-manage a sailboat in uncertain winds (60/40) and choppy water (weights and correlations) but, absent a compass – safe, liquid, and hopeful – where is it going?

And if the weather is bad, does it become a submarine and dive, so to speak. And the answer is yes, it does, although it is well-known that the liquidity concerns of a submarine (or a jet, on autopilot) and a pension plan might not be the same, at the same time.

Contract – Safe, Liquid, and Hopeful

We, of course, don’t know anything about their investments either – past, present or future – because we never buy investments; we only buy “risk” and for us, an “investment” is just and only the “purchase of risk”, and that it is something that we’re buying, not selling as does the rest of the industry.

And we know a lot about that – safe, liquid, and hopeful – and that’s always true, and we know how to guarantee that result. But they don’t, or won’t, and unlike the past, that isn’t good enough for this generation of investors.

And for more information on real “risk management” in modern times and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary and “(P&I) Dividend Risk and Dividend Yield“, and our recent Posts “(P&I) The Profit Box” and “(P&I) The Process – In The Beginning“; and we’ve also profiled hundreds of companies in these Posts and the Search Box (upper right) might help you to find what you’re looking for, such as “(B)(N) TLM Talisman Energy Incorporated” or “(B)(N) ATHN AthenaHealth Incorporated” or “(B)(N) PETM PetSmart Incorporated“, to name just a few.

And for more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice. And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

And for more on what risk averse investing has done for us this year, please see our recent Posts on “(P&I) The Easy (EC) Theory of the Capital Markets” or “(B)(N) The Easy (EC) Theory of the S&P 500“, and the past, The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.

{kind=link}

{kind=link}

{kind=link}