(B)(N) The Canadian “Hot” Money Stocks

The Weather Report

Drama. The S&P TSX Composite Index is up +16% so far this year. but there are over 120 stocks that have gained more than that – much more than that – and another 150 stocks that have gained (or lost) more than that – much more than that – for which “reasons” we don’t know, in either case, because there are as many “reasons” for a stock price as there are investors and their money, and it’s the money that counts.

The Index ETF or “balanced fund” buyer just got what the market gave them, and they had to stand in the sunshine and the rain without an umbrella – no cover – and talk about the “weather” (economics) with their “professional investment adviser” to whom they might pay 2% to 3% of their net worth, every year, for a “good weather” report.

But this is a desperate time (Fortune, January 9, 2014, Ray Dalio’s ‘All-Weather’ fund goes cold, or U.S.News & World Report LP, May 30, 2014, How to build an all-weather mutual fund portfolio).

And most “investment professionals” will tell us – fervently, they insist – that’s the best that we can expect to do, in the long term, but what they ought to say – and what they don’t say – is that “that” is the best that they can do for us, as they turn to another channel, or wait to tee-off.

But the fact is that if they cared, even a little bit, and for which we pay them, there is no excuse for heavy losses in a portfolio, even if the “market” is effectively “random” and can’t be predicted – which it is – and there is no excuse for losses to the capital no matter what the weather.

How much “risk” would you like?

To avoid “long term poverty” and “property damage” in all-weathers, all that we have to do is three things:

We need to buy and hold stocks, and we prefer those that pay dividends, to help with our need for cash; for “bonds”, please see below.

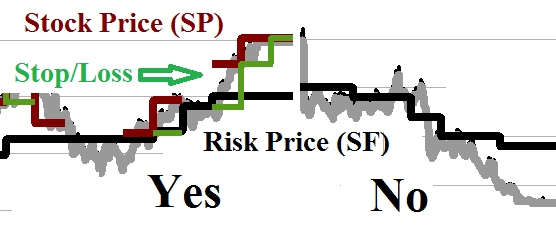

And we only buy and hold stocks at or above their “price of risk” – which we can estimate by looking at a stock chart and drawing a line (if we don’t have a better method) and just say that is what it is for this stock, and that stock, and so forth – but we need to be prepared to be wrong, which we can do (but for more on “drawing good lines”, please see our recent Post on “(P&I) Fannie Mae & Freddie Mac“).

Because, finally, we need to have an attentive stop/loss policy, or guaranteed sell-point, below the price that the stock is trading at, but no less than the “price of risk” which we have set to the best of our ability and common sense; for examples, please see almost any of our company Posts, of which “(B)(N) APPL Apple Incorporated” (yes) and “(B)(N) ARO Aeropostale Incorporated” (no) are two recent examples.

Just jack it up – the market will pay for it.

“Sell-points” or “target prices” above the current stock price are irrational – just jack-up the stop/loss, and see what else the market wants to do for us.

And we can ignore bonds because they don’t pay a rate that is much above the rate of inflation, and gains and losses are determined by “basis points” (100 basis points = 1%), which is only useful if we’re working a multi-billion dollar portfolio, and there aren’t enough equities to go around.

Moreover, the above method “simulates” bond-like properties – 100% capital safety, 100% liquidity, and a hopeful but not necessarily guaranteed return above the rate of inflation – which makes it better than a bond if we don’t have too much money. And nobody talks about “capital safety” with bonds, anymore. anyway.

So, if we can do this for ourselves, why can’t our investment advisers do as much – safe, liquid, and hopeful – those are the words that move us, and those are the words that we need to impress upon them. And if we don’t hear those words, in writing, then there is no point in giving them our money. Better to buy a TIPS or RRB if we don’t hear those words, and maybe those words – TIPS and RRBs = will impress them.

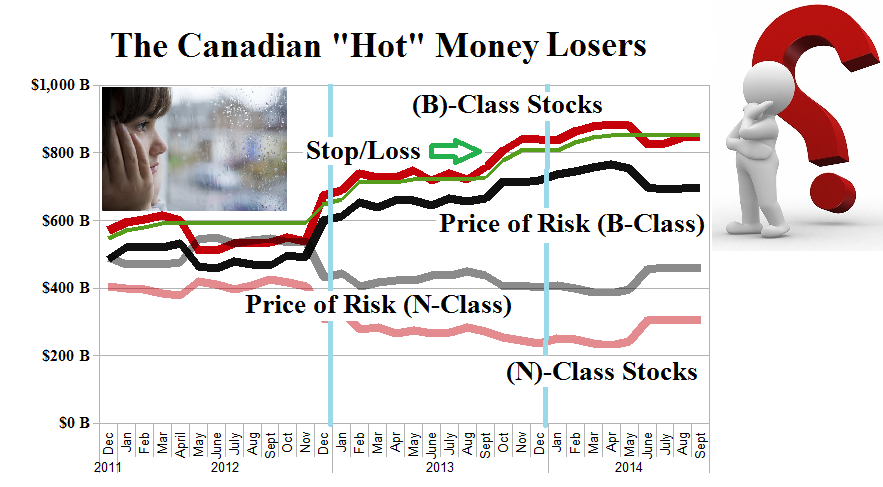

Normally, we look at the whole market, or possibly segments of it, such as the transports or the utilities or the banks, but today we’re going to look at the status of the “Winners Portfolio” – those stocks that have gained more than +16% so far this year, and the “Losers Portfolio” of those stocks that have gained less than +16% so far this year – and compare that with what we knew about them in December, last year, because December, this year, and a change in the weather, might soon be here.

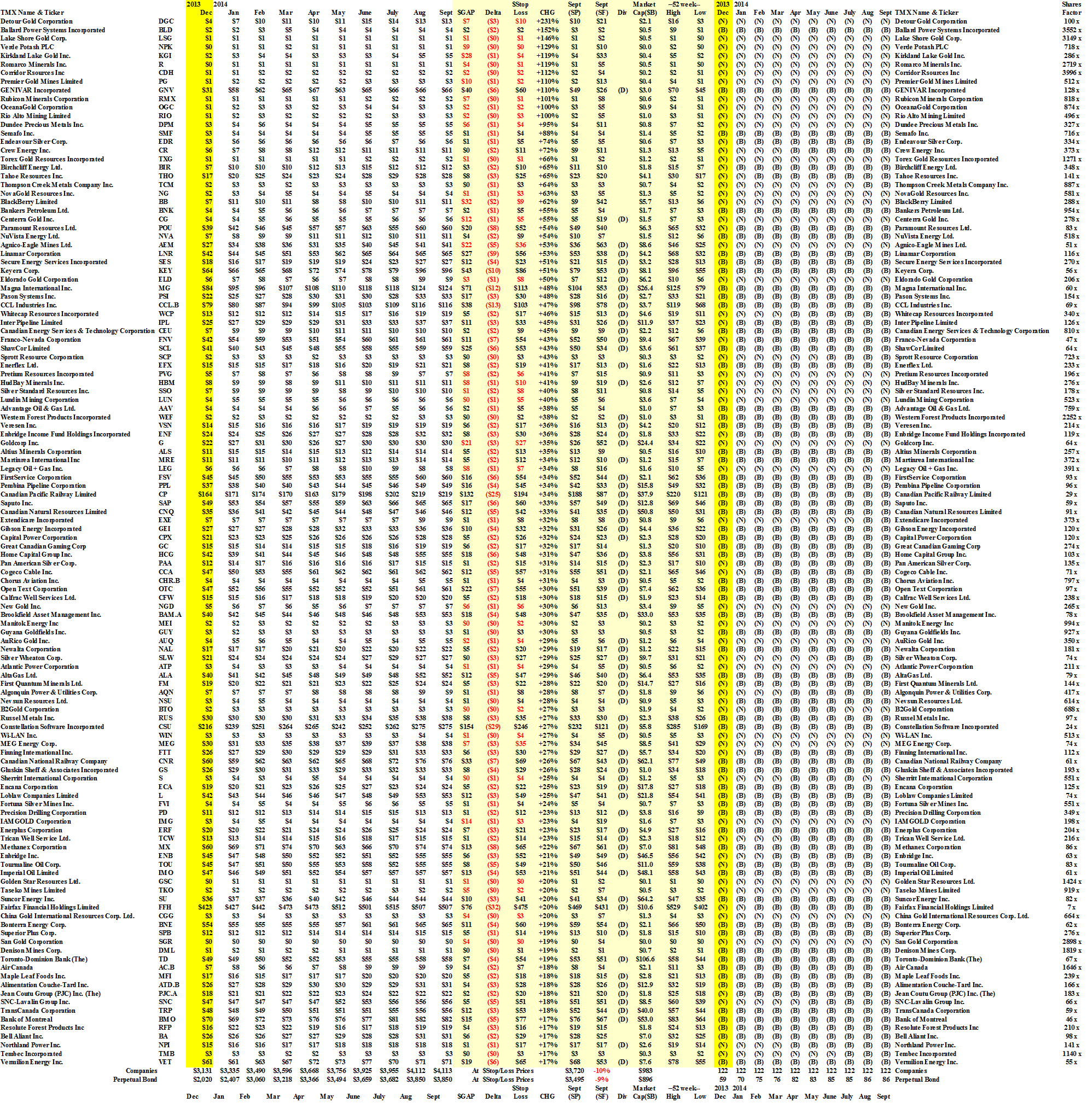

Exhibit 1: (B)(N) The Canadian “Hot” Money Stocks – Winners & Losers

Figure 1.1: Hot Money Winners

Figure 1.2: Hot Money Losers

The “Winners” are up +51% on a cash basis, and +80% on a moderately leveraged basis, using only the margin account, and “equal-weighting by market value” (and we note that weighting by the “capital assets model” (CAPM), or “modern portfolio theory” (MPT), is irrelevant, and gives and guarantees only “random” results).

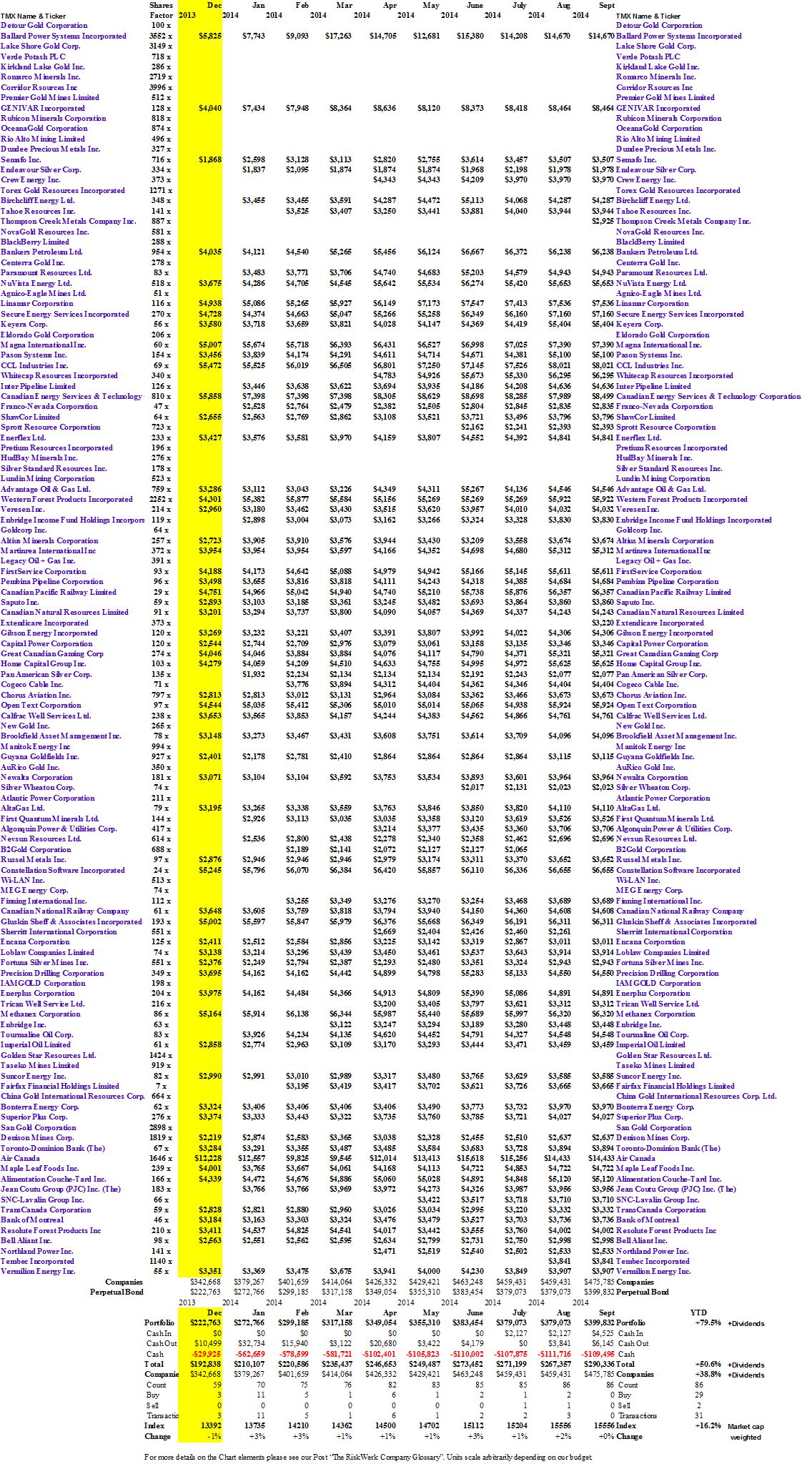

They also lost a lot of money last year ($13 billion) but they also made a lot of money ($46 billion) in aggregate, for a net gain of $33 billion, and they returned 60% of their earnings, and an aggregate dividend pay-out of $19.7 billion, which gave the investors an aggregate dividend yield of 2%; please click on the links (and again to make them larger if required) “(B)(N) The Canadian Hot Money Stocks Winners – Cash Flow, Portfolio, and Fundamentals” for the details.

Currently, 86 of the 124 companies in the Winners are (B)-class – that is, they’re trading above the price of risk – which is up from 59 in December, and we only made 29 buy decisions and 2 sell decisions in all of that time; moreover, the “guaranteed” portfolio return is at the stop/loss (green line in Figure 1.1) – so, go ahead, change the weather.

In contrast, the performance of the (N)-class companies – trading below the price of risk – in that same portfolio of companies with stock prices that have increased by more than 16% this year (Figure 1.1 above), were not in our portfolio all of the time, only some of it, and that portfolio is down minus (-54%), because some of those companies migrated into the (B)-class, and we knew enough to buy them when they did, but not enough to buy them in the (N)-class, for which the prices are lower, but indeterminate, volatile, and we don’t know the downside – hence, they are not qualified for safe, liquid, and hopeful; there are still 36 companies in that class (122 less 86).

The portfolio of stocks that have gained less than +16% this year (Figure 1.2), has a domain of 152 companies, and if we managed it in the same way as the other portfolio, it returned only +8%, and had a lot of idle cash. Those companies also lost $11 billion, but earned $61 billion, in aggregate, and returned 75% of their net earnings to the shareholders for an aggregate dividend yield of 3.3%.

We started with 91 of those companies, but are down to 84, and we made 10 buy decisions and 17 sell decisions since December; please click on the links “(B)(N) The Canadian Hot Money Stocks Losers – Cash Flow, Portfolio, and Fundamentals” for the details.

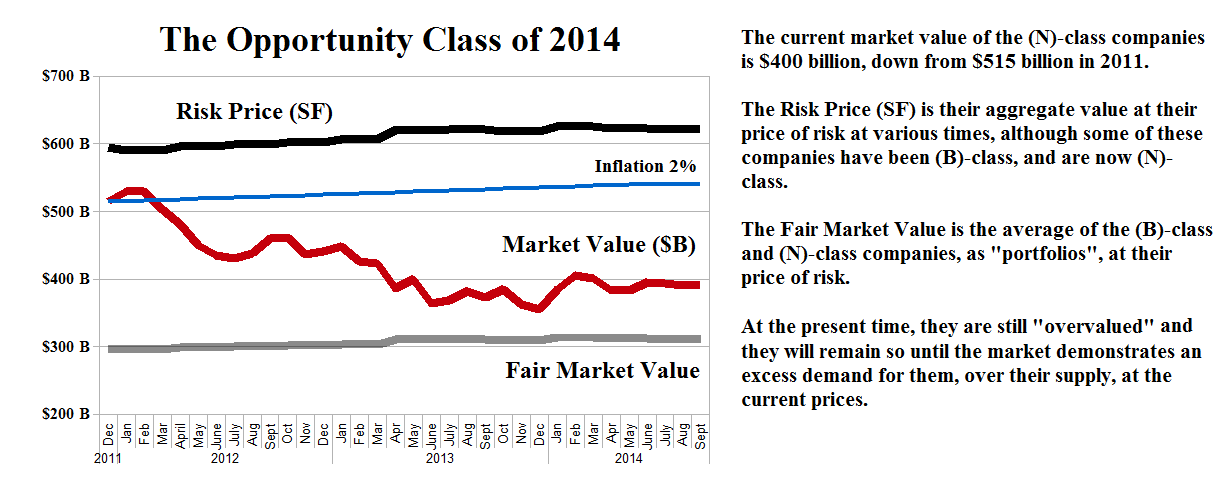

Figure 1.3: The New “Opportunity” Class of 2014 Not Safe, Not Liquid, Maybe Hopeful

The “opportunity class” of (N)-class companies is also much larger – 68 companies – so that there are currently 106 (N)-class companies in this market (38 plus 68).

That’s about 1/3rd of the market (106/276 companies) and these companies have no direction as far as their stock prices are concerned, neither up nor down, but, based on Figure 1.1 and 1.2, they have a lot less to lose, and they’re all trading below the price of risk – which might make them attractive to some folks – but not to us; please see Figure 1.3 on the right, and the aforementioned links for more details.

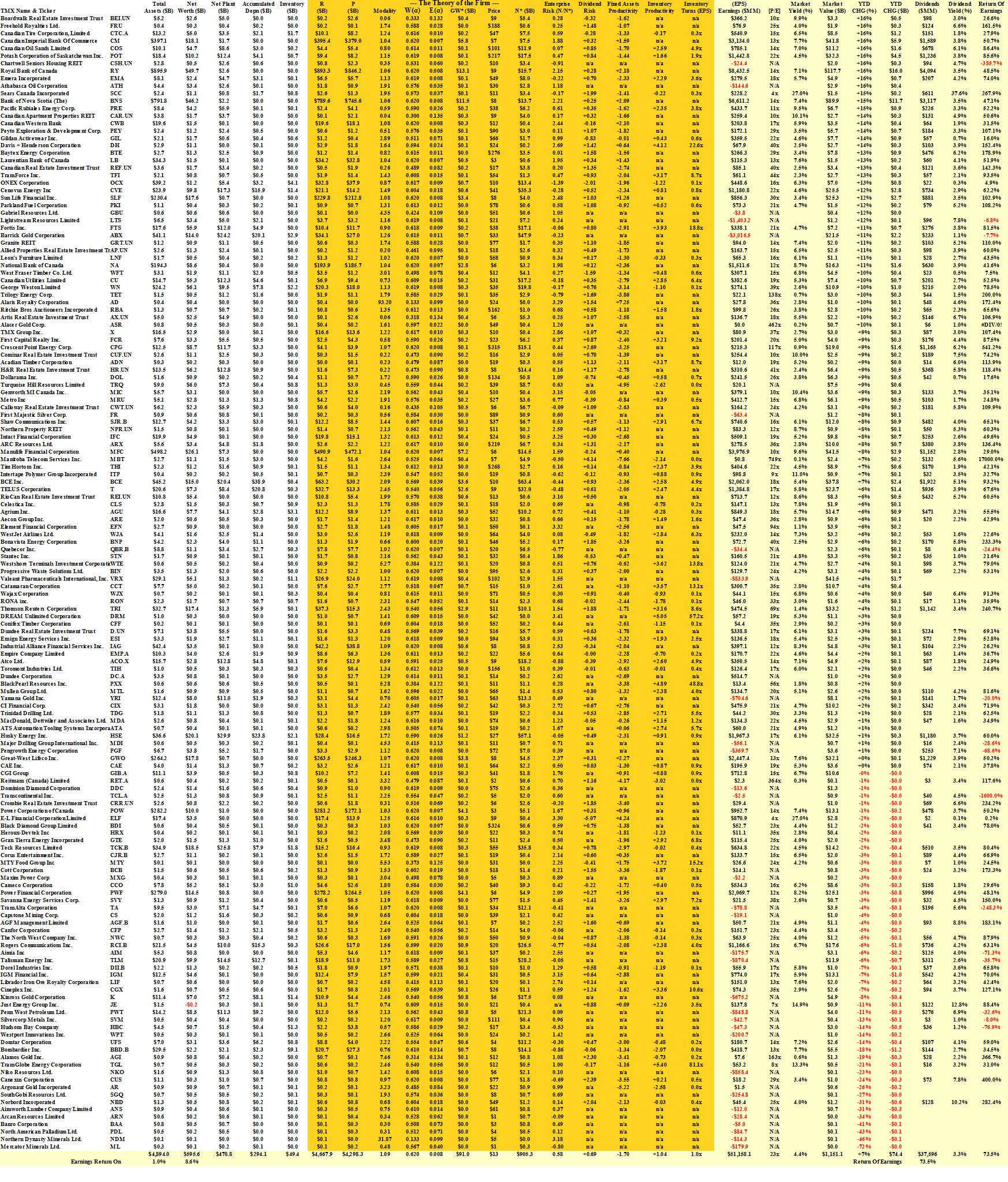

For more information on real “risk management” and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary and “(P&I) Dividend Risk and Dividend Yield“, and our recent Posts “(P&I) The Profit Box” and “(P&I) The Process – In The Beginning“; and we’ve also profiled hundreds of companies in these Posts and the Search Box (upper right) might help you to find what you’re looking for, such as “(B)(N) TLM Talisman Energy Incorporated” or “(B)(N) ATHN AthenaHealth Incorporated” or “(B)(N) PETM PetSmart Incorporated“, to name just a few.

And for more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice. And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

And for more on what risk averse investing has done for us this year, please see our recent Posts on “(P&I) The Easy (EC) Theory of the Capital Markets” or “(B)(N) The Easy (EC) Theory of the S&P 500“, and the past, The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}