(P&I) Stocks & Bonds For Actuaries

Man Creates Mutual Funds

“Here, Man, You Deal With It.”

$20 Trillion of Our Money.

Drama. Once upon time, not too long ago, we needed a broker to execute our orders for buying and selling stocks and bonds and the cost was not cheap but ran to 3% or 4% of the “order” whether buying or selling.

But times have changed, and between then and now, Man has developed “mutual funds” – tens of thousands of them since the 80’s – and then “hedge funds” in the 90’s and even more tens of thousands of those, none of which we can use because none of them can do anything for us that we need and can depend on.

And they don’t reliably do anything that the Perpetual Bond™ does for us:

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

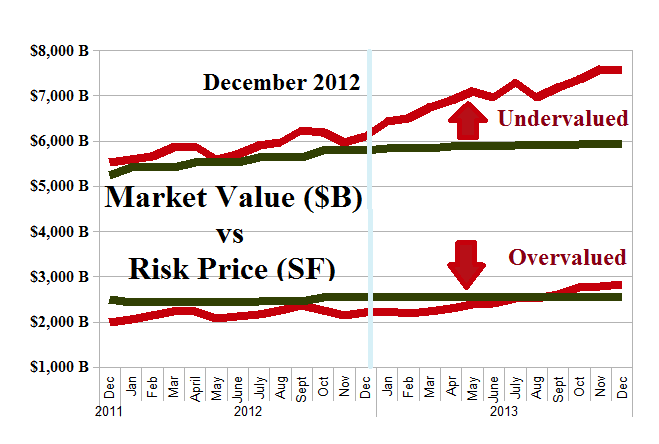

Nor is that too much to ask. For example, last year was spectacular for us because we were helped by a rising market for stocks meaning only that the demand for stocks exceeded the supply and, therefore, the prices of stocks tended to increase because the effective supply didn’t. Please see Exhibit 1 below.

Exhibit 1: The “Undervalued” Equity Markets in 2013 – Same Rule All Year

Aggregate Market Returns – December 12 2013

But this year it could be tough to make money in the stock market. Not because the companies are waning (as many suppose) or because the supply of stock is increasing at a faster rate but because of the destabilising influence of all those thousands of mutual funds and hedge funds that don’t know what they’re doing with multiple trillions of our dollars other than, they say, “investing” it by deployment – which we might call “dumping”.

Because they don’t know that an investment is just and only the “purchase of risk” and although they are manifestly familiar with the “cost of risk“, they have no idea of the “price of risk“.

Because they don’t know that an investment is just and only the “purchase of risk” and although they are manifestly familiar with the “cost of risk“, they have no idea of the “price of risk“.

And they don’t know that the “risk” is that we might not get our money back when we need it and that “risk” is the same as it was last year and every year before it.

Or that we might not get a hopeful return above the rate of inflation which, if we don’t get it, is just another way of losing our money.

And if they can’t or won’t guarantee the capital – 100% capital safety – they’re just gambling.

Efficient Frontier (B)(N) Boundary Open

“In Control And Not Just Gambling”

Guarantee It Or It’s Gone.

In order to show us that they’re not just gambling, they need to show us that whatever method they use separates the market into a portfolio of stocks, the (B)-portfolio, that tends not to lose in value and equally importantly, that the portfolio of stocks that does not use their method, the (N)-portfolio in the same market, tends not to gain in value.

If they can do that, then we’ll know that they’re in control and not just the subjects of random or specious factors and market “surprise”.

Friction

All that water but no liquidity. Blame it on the “sand” and high [P/E]’s.

But the action in both bonds and equities is a lot like waves in which the crest is blown by passing winds that “foresee the future” but the bottom of the wave which is the “fundamental” is moving much more slowly and has to do a lot of work and, of course, the demonstrated action of the “wave” is nothing like the peaceful up-and-down reversion to the mean that is implicit in Modern Portfolio Theory (MPT) and portfolio management by “volatility” and “co-volatility”.

And so we invest only in the “fundamental” that is defined by the “price of risk” and if the “winds” pick up, so much the better because we only ever have to deal with “surprise” both good or bad. And that’s easy.

Exhibit 2: (B)(N) How The Future Unfolds – The “Unmanaged” S&P 100 Since December 2012

S&P 100 (B) and (N) Portfolios – December 2012

For example, the (B)-portfolio in the S&P 100 companies held only 74 companies in December 2012 but has 90 now.

The managed cash only portfolio returned +44% last year and the current active portfolio with 90 companies in it (and only 10 not) and a moderate use of the margin account returned +82% plus dividends last year.

The chart on the left shows how the unmanaged portfolios evolved in the course of the year and how we were faced with the same apparent “dilemma” of the high-priced “undervalued” stocks in the (B)-portfolio and the low-priced “overvalued” stocks in the (N)-portfolio.

For more information and additional references to the theory, please see our Post, The RiskWerk Company Glossary.

And for more on what risk averse investing has done for us this year, please see our recent Posts on The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.