(B)(N) There’s Always A Bull Market Somewhere

Already? Are we covered for this?

Drama. The drums are rolling and the “market” is getting ready to signal its next “ritual suicide” with the same flare and “purpose” (please see below) as the ancient Phoenix. They say that it’s time for “renewal” and “fasting” and the “bears” are loose and growling or frowning or worried about high valuations and the impossibility of the companies living up to the high expectations that investors have set for them (Morningstar, November 25, 2013, Prudent Strategies for a High-Flying Market).

Undoubtedly, there are some very hot spots in the market and they make a lot of news – and noise – because they are astounding and off the charts but that’s not what the market is about any more than a few dozen noisy football fans will decide the outcome of the game.

In counterpoint to the noise, the thirty companies of the Dow Jones Industrials are up +21% this year and added $816 billion to their market value. They also paid $127 billion in dividends for a yield of 3.3% to the stalwart shareholders who have owned the Dow all year without much change. Please see Exhibit 1 below.

Exhibit 1: Aggregate Market Returns – December 12, 2013

Aggregate Market Returns – December 12 2013

Good, Serviceable

Maybe we should have it too?

Most of us would say that a good, serviceable, product (for which there are substitutes) that is not free but possibly scarce or difficult to make but everyone wants to buy it because it is “serviceable” and it can be bought, is “undervalued” because the demand for it at that price exceeds the supply of it.

The evidence of “good” and “serviceable” would be that if the supply diminishes, then the price might tend to rise as owners bargain with buyers.

On the other hand, if no one wants to buy it at that price then possibly it is “overvalued” but the demand for it might pick up at a lower price if it can be bought at a lower price; for example, it might not be produced or available if the price is too low or those who have it might not want to sell it at that price because they attach a higher value to it (at least, for themselves).

The Value of $1 Since 1776

Cash Is Not An Option Unless We Have A Lot Of It And Don’t Mind If Somebody Else Is Spending It.

So, that’s where we are in the “market” for stocks. Our choice is between “money” as cash or “money” in bonds or “money” in stocks and each such choice is the purchase of risk.

There are lots of people who don’t agree with this analysis.

Judgemental Are We?

But It’s Not In The Contract. (Sir.)

The “bears” are attacking the product on the basis of price and “serviceability”; they say that [P/E] multiples are too high and that there is no way that these companies can deliver on those expectations.

But the companies have never said that they could or would nor do they have to meet our “stock price” expectations – it’s not in the contract.

The business of the companies is their business and we rely on them to take care of business so that investing our money in them is an opportunity that is denied to many in the world, not a burden or an unwelcome journey into the darkness.

For that, we have travel insurance and it’s quite cheap when options are priced only on the demonstrated “volatility” and we’re checking our stop/losses for effectiveness and buying puts in some situations for the next lifetime. And no matter what the “market” does, we’re keeping a full house and looking for new opportunities to buy “good” stocks at “low” prices – those that are trading at or above the “price of risk” and no others.

Moreover, the “bears” could have said that the market is “overvalued” at the beginning of the year when prices were much lower but the market gains were still in excess of +30% or so since early 2009. And they did say it.

The Markets Are Efficient, You Say?

Where? How?

But “Thank You” For Keeping The Price Of Options So Artificially Low.

And “economics” doesn’t help either because there is nothing in economics that can be used to decide if a stock is “fairly valued” and a good use for our money – we want our money to be safe and to hopefully provide a return above the rate of inflation – and its celebrity counsel is noisily stuck in the “fire storms” of 1914 without the benefit of Alfred Marshall to temper their dismay (Reuters, December 7, 2013, Fama: The World Is At Risk Of Recession In 2014 and The Wall Street Journal, December 2, 2013, Robert Shiller ‘most worried’ about ‘boom’ in U.S. stock market).

But neither the money nor the companies are destructed by a stock market swoon, crash or boom. Both the money and companies just have new “owners” who are a lot like the previous owners and if stock prices are low after high, there will be even more “money” for the previous owners to invest, pay debts or spend.

What “renewal” means is that investors who have made bad calls this year, and perhaps longer, are going to lose their money because they’re late or ineffectual and they will give it to investors who have made good calls and better “choices” (so to speak) although simply buying into “momentum” seems to be what keeps a lot of the “market regulars” up at night and busy all day calculating [P/E] multiples and moving averages trying to determine “fair value”.

But we can reasonably expect that the “momentum stocks” with sky-high [P/E] multiples or no earnings or dividends at all will be among the first to fall in the flight to virtue – if there is one. But what are they going to do with their “money” if bond rates are low and “money” does not command a return above the rate of inflation (Reuters, December 3, 2013, Salmon:The $5 trillion dilemma facing banking regulators)?

Constructive Illiquidity

It’s In The Contract.

And when the market rolls (if it rolls), so will many ETFs and portfolios tied to the self-consuming “index” – that’s in the contract – and for those investors the market will always be “expensive” even if they managed to buy and hold at the market lows because it takes a long time to obtain new highs and gains that might not occur before they need their money or their creditors (who are efficient) want theirs.

On the other hand, the drums have been rolling since March and with some foresight, investors can turn every possible cliff and jump-off point into a “short hop” and run with the well-heeled “vicious bears” and “rampaging bulls” who have diverse agendas that are never transparent – it’s their money, isn’t it – but ritual suicide is not one of them (The Street, December 5, 2013, Cramer: There’s Always a Bull Market Somewhere).

100% Capital Safety

Guarantee It Or It’s Gone

For us, a stock is “undervalued” if it’s trading at or above the “price of risk” because at that price it demonstrates an excess of demand over supply. There is a metric but unlike [P/E]s or “technicals”, it is a “preference relationship” that is defined by the “demonstrated societal standards of risk aversion and bargaining practice” and turns on the observation that investors do not invest their money in order to have a better chance of losing it.

And the prognosis is not different for professional managers of institutional funds who will not guarantee capital safety whatever method they use. If they can’t or won’t guarantee capital safety, it’s the wrong method.

We can look at this more objectively without any “axe to grind”. The “meaning” of “undervalued” and “overvalued” can be understood from the three charts below.

A “market” in aggregate is “fairly valued” at the stock prices that are trading at the price of risk; “undervalued” if above the price of risk and “overvalued” below the price of risk.

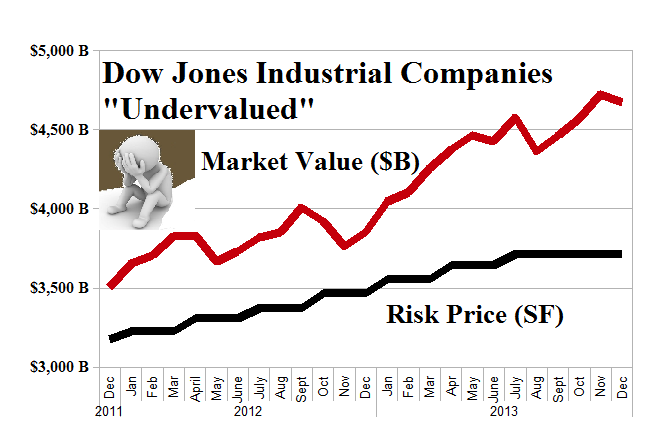

Dow Jones Industrial Companies – Undervalued

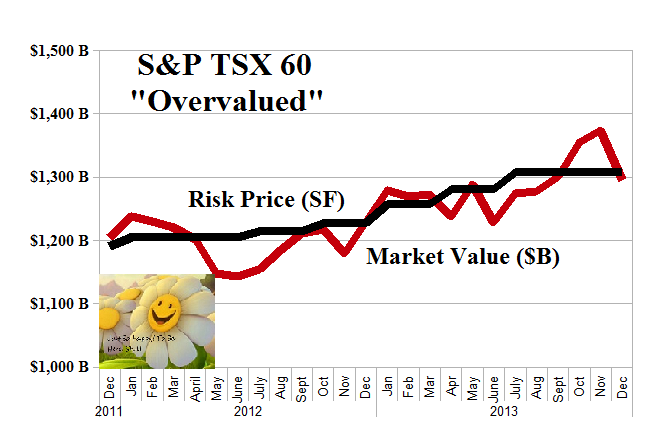

Investors have a choice. The “bulls” can continue to suffer (please see the chart on the left) in the “undervalued” Dow Jones Industrial Companies and the “bears” can take their money off the table and give it to the “overvalued” S&P TSX 60.

S&P TSX 60 Overvalued

It’s a pity, after all, that the Dow has paid so much in dividends ($127 billion) this year and might not be able to pay so much next year or if we’re just buying in now, the yield won’t be a spectacular 3.3% unless these companies can continue to produce what people need or want.

Certainly, it’s a long throw.

In contrast, the “overvalued” S&P TSX 60 really needs our money – the “bears” should give it to them – and there are lots of bargains in commodities, resources stocks, banks, rail roads, grocery stores and retail, and the market is “cheap” at less than $1.3 trillion and only up an uncertain +5% since last year.

S&P 500 Overvalued Undervalued

In fact, the S&P 500 was also “overvalued” at low prices just two years ago and look what happened.

These companies gained $2.2 trillion in market value this year and paid their shareholders $340 billion in dividends for an aggregate yield of 2.7% (please refer to Exhibit 1 above) so, clearly, there was a lot of undiscovered value there, one would think.

But maybe the “bears” are right and they’re all tapped out too and can’t do it again.

In any case, these markets gave us +40% in the cash only Perpetual Bond™ this year and even our stop/losses will check us out with less than 10% in price declines should the market decide to bail.

We’re not so worried and will just keep a full house and celebrate our good fortune. “Luck” and “uncertainty” has nothing to do with it. There’s always a bull market somewhere and it will find us because we really are undervalued.

For more information and additional references to the theory, please see our recent Post, The RiskWerk Company Glossary.

And for more on what risk averse investing has done for us this year, please see our recent Posts on The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100.

And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.

text