A New Key In Economics

Essay. Most economists readily agree that “equilibrium” is not something that we should expect to see in our markets or economies. But despite that, the economic method almost always starts with some assumptions about markets clearing, prices forming, supply and demand in balance, or that markets are efficient and transaction costs can be ignored, and the economists will self-justify or expertly affirm themselves by saying to politicians and leaders, or their colleagues, that what they’re doing is a reasonable approximation to the “real thing”.

Jump?

The problem is that’s never true, and one should not expect that what they’re doing has any bearing on what they’ve been asked to do if “smoothness” or “nearness” or “insignificant” are the rationalisations. Secondly, the “real thing” might be the fiscal budget, monetary and mercantile policy, inflation, deflation, employment, social welfare, and so forth, virtually everything and anything that might affect the life and death of people and nations.

As we shall show, we have not overstated the case – economics has no predictive value but is a vast data gathering system that gathers any kind of data in every person and department of every company of every nation on earth, and can make interesting observations on aggregates of those data, but cannot make any prediction of anything except the “extraordinary”, that is, the “far from equilibrium” situations that we would describe as “catastrophes” such as an ever deepening depression or uncontrolled expansion, inflation and growth (like a “cancer”). To change that situation, we need to find a “key”, a new key¹, which we will describe below:

Liabilities & Assets

A “key”, a new “key” in economics?

Let Ε = {P, {T}, Z={A,B,C,…,{L},{M},N,…}} be an “economy” with some “production function” (P) that maps allocations of “tokens”, {T}, such as “money” or money-substitutes or both, to any number of “agents” or “actors” Z={A,B,C,…,{L},{M},N,…} which we may describe as people, companies, goods or services, or activities, or things that have nothing to do with P. We don’t need to know anything about the production function (P) and it is entirely arbitrary, but when it acts, or as it acts, tokens get moved around (or not) among the agents and that’s the “economy” that we observe (and tabulate) and informs (P). We can then say the following:

(1) If there are two classes of agents, {L} and {M}, that cannot be changed by the production function, P, unless they are both changed, then this economy will never obtain an equilibrium; that is, there is always an opportunity for something else, or for change, hopefully, for the better; and

(2) If there is no such pair, {L} and {M}, then this economy is a catastrophe.

We will call such a pair, {L} and {M} (and they could be “singletons” rather than sets), a “key”, and there may be many such keys with different consequences, but one should not assume that a key will exist or be easy to find because the requirement is that always, as a result of the action of P, which distributes “tokens”, either both {L} and {M} change or neither does, or, in other words, the economy shall either include them both with every action or shun them both with every action, but the economy cannot choose between one policy or the other in any instant; the choice is built in by the distinction that we make in {L} and {M} from the other actors in the economy. An example might be L=Labour and M=Money (or, following Adam Smith, “wheat”) and we require (for example) that labour cannot increase or decrease without also a change in money, and vice versa, so that neither changes or they both change, but we don’t require any direction, with, obviously, different consequences. We note also that, for example, L={L}, could be an abstraction such as “labour” or it could be actual labourers who are also “actors” in the economy.

Fermat’s Last Theorem

17th Century

The proof is immediate (after due discovery) but requires a theorem of Ormand Van Quine, the philosopher and logician ( “Fermat’s Last Theorem in Combinatorial Form”, American Mathematical Monthly, 1988) and Fermat’s Last Theorem (17th century) which was finally resolved in the affirmative by Andrew Wiles in 1995 ( ”Modular elliptic curves and Fermat’s Last Theorem”, Annals of Mathematics 141 (3): 443–551 (1995)) and not for want of trying for three hundred and fifty years.

Van Quine shows (and the proof is ingenuous but not difficult; please see below) that “the number of ways of distributing tokens {T} that shuns any two “buckets” {L},{M} is never the same as the number of ways that includes them both” and that result is equivalent to Fermat’s Last Theorem (with power, n, equal to the number of tokens in {T} and any number of buckets, three or more).

For example, if there are only two tokens (n=2) and three buckets, {L, M, N}, then there is only one way to distribute the tokens so as to shun two of the buckets, {L, M}, and only one way to distribute the tokens to include them both. If there are three tokens (n=3), however, then there is still only one way in the former (all the tokens are in N and none are in L or M) but already three in the latter (two in L and one in M, two in M and one in L, and one in each of L, M, and N).

Jump Anyway?

As a result, any economy in which we can find a key, k = k(L, M), splits into two completely different economies that involve the same agents but which have different outcomes because the possible distributions or opportunities of “tokens” must be different in number and, therefore, there is no isomorphism possible that does not involve some destruction or creation of actors and tokens, and which cannot be done “smoothly” – we must expect to lurch and not necessarily to transition by substitution or “smooth” and rational reallocations of resources from one to the other.

Recent examples of “lurching” abound such as the demise of the leader of Libya, or the firm, Lehman Brothers, or the success or failure of some new technology or process, none of which can be explained by a general equilibrium model of the economy to have such dramatic effects, nor can said lurching be deemed to be insignificant in the long run (consider Cuba). It happens all the time.

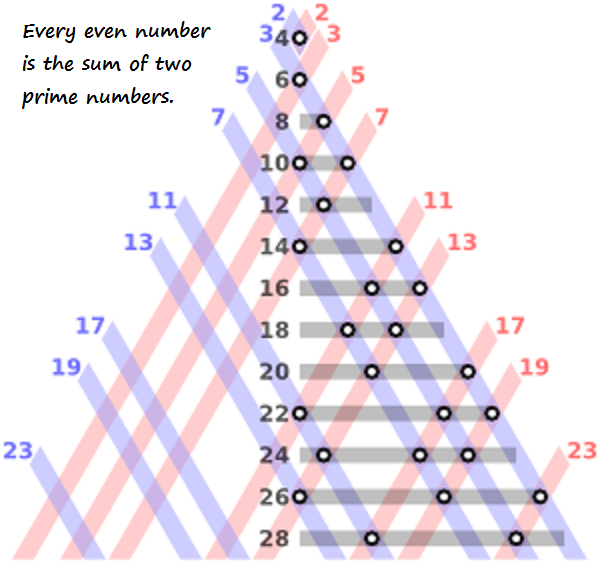

Goldbach Conjecture

(1690-1764)

Seems easy …

Moreover, every key defines two new economies involving the same agents, tokens and production process so that causality can be observed in increments and the “economy” separated (or “orthogonalized”) by a number of “keys”.

¹ This Post is inspired by my granddaughter, Elizabeth, who told me to “find a key, a new key, Opa.”

A Short Proof of Van Quine’s Theorem

Suppose that we have n beads (or investors) and z bins (or companies as above) so that there are in total z^n different ways of depositing (investing) the n beads into the z bins (companies). If x is the number of bins that are not {L} and y is the number of bins that are not {M} then there are x^n distributions of beads that shun {L} and y^n distributions that shun {M}. So let A be the number of ways that shun both {L} and {M}, let B be the number that shun {L} but not {M}, C be the number that shun {M} but not {L}, and D be the number that shun neither and, therefore, includes them both. Then,

x^n = A+B, y^n = A+C and z^n = A+B+C+D

so that x^n + y^n = z^n (Fermat) if and only if A=D. Since there are no integral solutions to Fermat’s Equation for n>2 we must also have that D is never A if n>2. QED.

We also note that Fermat’s Equation has infinitely many integer solutions of the form {x^p, y^p, z^p} for n=2/p, p=1, 2, 3, 4, … and so forth, but none of that form for n=3/p. That means that we can find arbitrarily long sequences {2/p1, 2/p2, 2/p3, …} for which there are infinitely many solutions in every case and some n=3/q as close as we like to some n=2/pκ for which the solution fails, which is something to think about when the economist argues for “continuity”. In fact, said n=3/q can be “surrounded” by millions of “solutions” but not one of them applies to n=3/q.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.