(B)(N) Banking in America

Buccaneer Banking In America

Drama. The earnings season is upon us again – we just did this in October – and the big six New York banks are going to step up and be counted (CNN Money, January 12, 2014, Wolves of Wall Street to report earnings).

Hemmed in by two decades of scandal and abortive attempts at “buccaneer banking” that have cost them a lot of money and reputation, the banks appear to be returning to their roots as deposit-taking institutions that earn their money by service and not so much by speculation (The Globe and Mail, January 12, 2014, U.S. bank earnings likely to signal tough year ahead).

Nevertheless, investors have bid up the bank stocks by more than +40% since December 2012 and their earnings net of what they need to retain in order to re-build their capital are not available for distribution to the shareholders. The current dividend yield is only 1.5% but investors who bought the banks early last year did much better and are now holding stocks that have also appreciated in value by about 40%. Please see Exhibit 1 below.

Exhibit 1: Banking in America – Fundamentals

Banking in America – Fundamentals

We don’t know the future and the past is soon forgotten. But we do know now and for now, the investors have demonstrated a very positive outlook for the banks, even though “local volatility”, “rebalancing” and profit-taking might corrupt that view from time-to-time. Please see Exhibit 2 below.

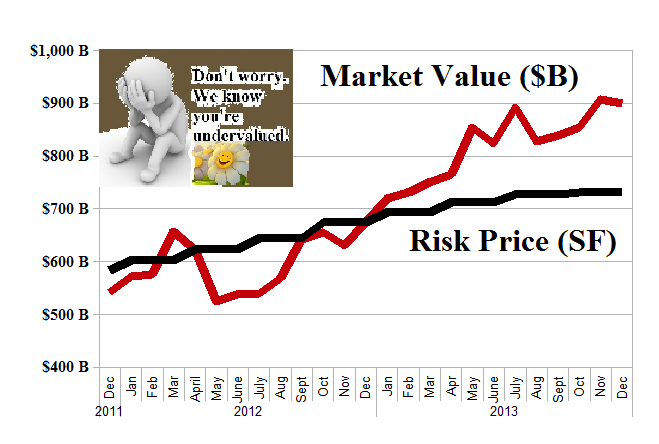

Exhibit 2: US Banks Still “Undervalued” – January 2014

US Banks Undervalued

The chart shows that the big six US banks have gained more than $400 billion in market value since 2011 (Red line) and that they have been trading above the “price of risk” since December 2012 and are trading substantially above the price of risk now (Risk Price (SF)).

What that means is that the “demand for the stocks exceeds the supply” and, therefore, the price of the stocks has been bid up substantially last year and that situation still obtains. If we were a bank, we’d think about retiring the cutlass and issuing some stock or convertible preferreds to ease the demand.

Our estimate of the downside in the stock price due to the demonstrated volatility is minus (7%) but as long as the banks are trading above the price of risk, we would see any price weakness as a buying opportunity. Please see Exhibit 3 below.

Exhibit 3: US Bank Stocks – Prices & Portfolio – January 2014

US Banks Perpetual Bond – Stock Prices & Portfolio – January 2014

For more information and additional references to the theory, please see our Post, The RiskWerk Company Glossary.

And for more on what risk averse investing has done for us this year, please see our recent Posts on The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.