(P&I) One economist at a time

“Investments are dear when the money is cheap” – The RiskWerk Company

Essay. Why is the rate of inflation in the United States so low, at around 2% per year, and even that seems hard to maintain? And in China at 1.6%? And why is it even lower in the Euro-area economies, which seem to be flirting with deflation and rates of inflation approaching zero? And why is it so high in Brazil (6%), Argentina (10%), and Venezuela (60%)?

We’re not sure what the economists are saying about this issue, because we have only one hand, and not the other, so to speak (please see below), but the economists seem to have been predicting that the rate of inflation in the United States is destined to rise, although they’re not sure when, and that has created some off-and-on panic in the bond markets because if it does, when it does, then the prices of the current low-yielding bonds will need to decrease in order to keep pace with the new issues that are higher-yielding (Bloomberg, October 30, 2014, Economics Progresses One Funeral at a Time).

That seems like an obvious conclusion, but what they’re not saying is that the reason that inflation is so low, now, is that the “price” of an income in the United States, and even more so in the Euro-area countries, is so high, now, and the rate of inflation will not rise until investments are cheap and money is dear – which might never happen because we see no reason that the cost of an income (from investments) should decline while money is “cheap” – which is now.

Dear Money is not Cheap

Figure 1: S&P 500 and Inflation

The chart on the right shows that the stock market tends to lie fallow when inflation is high, for example, throughout most of the 80’s, and pick-up when inflation is low (or lower), but it also shows an extraordinary response to “cheap money”, that is, money as near-cash that can’t get a non-negative real return in government bonds.

Figure 2: S&P 500 What are they buying?

And we’ll also say that “money is dear” if it can, and one of the conclusions is that “the stock market is always cheap“; please see Figure 2 on the right.

That “logic” might seem a little bit “twisted” – and it is – because the “investments” that we’re talking about are twisted; Figure 2 on the right shows that investors are currently willing to pay a 50% premium over the same investments in 2012 to get a 16% return on their equity (which actually belongs to the company) and a 2.1% dividend yield at the current prices – in other words, their money is cheap, and they would rather have the investment in stocks than in bonds; for more information, please see our Post on “(P&I) The End Of Fixed Income“.

But does that mean that we should be taking our “cheap” Euros and US dollars and buying “investments” in Brazil, Argentina, and Venezuela, and wherever else the rate of inflation is higher than ours and, therefore, where our money is dear and their investments are cheap?

Yes it does – but there is an important caveat, namely that an “investment” might not be what you think it is; for example, buying the government bonds of these nations, or any other nation, is not an investment if there is no risk – a “government bond” is a source of guaranteed income, and guaranteed capital (for the most part) and the investor in that bond needs to be happy with that income – but it’s unlikely that they will be if the rate of inflation in that currency is increasing, and ours is decreasing, or not increasing as quickly.

In other words, it’s a “risky” purchase with a guaranteed coupon and guaranteed capital (in most cases), but not a guaranteed income in the real terms of our purchasing power, which is also true if the currency is our own.

It’s not hard to see that “money is “cheap” – that is, it does not earn a non-negative real return – if and only if investments are “expensive”; and money is “dear” – that is, it earns a non-negative real rate of return – if and only if investments are “not expensive”, and we can’t substitute the terms “cheap” and “dear” for “not expensive” and “expensive” investments, because the non-negative real return on an “investment” is hopeful, but not guaranteed, whereas “dear money” is a “gift”, however righteous are the “dear investors” who receive it.

As a consequence, the rate of inflation is low (or lower) because investments (and, therefore, an income) are expensive, and money is cheap; and the rate of inflation is high (or higher) because investments are not expensive, and money is dear.

That notion is troublesome to economists because it puts them out of business; they think that “inflation” has to do with the prices of goods and services because that’s how they define it; we, on the other hand, know that inflation is low if and only if the stock prices are high (and so money is cheap), and inflation is high if and only if the stock prices are low (and money is dear).

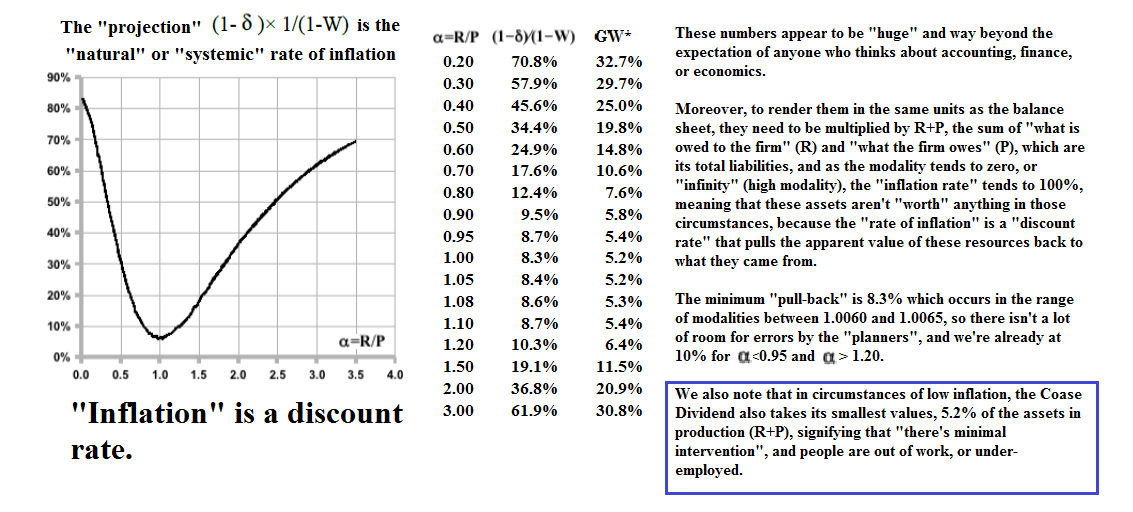

The Real Rate of Inflation (and Growth) is Always 8.3%

The headline says that “inflation” in the prices of goods and services is only a part of the story, and if that rate is 2%, for example, we need to wonder where the other 6% is. And if it’s 12%, then we know that there’s a 4% “hand-out” someplace else, most likely in government-secured assets that are paid for by the taxpayers; who are they and why are they getting it?

For example, in Venezuela which has an “inflation rate” in excess of 60%; who, or what, is consuming 60% of the wealth of this country? Or Brazil at 6% to 7% is almost right on the money; that looks like a place that we can invest in.

It’s taken us nearly one hundred years to establish that governments are “transfer machines” (like a “heat pump”) and what they do on a day-to-day basis – when not declaring war – is transfer wealth from some pockets to the others, and sometimes (if not oftentimes) from all the other pockets to “some” pockets, which is the “natural” tendency because there are no “benevolent” governments.

In order to understand that equation, we have to go to the Theory of the Firm in which “cash” has no importance – it is a zero and, therefore, very “cheap” – unless it can be deployed to produce “payables” and “receivables” which are “money in float”, between products and services (payables to produce them) and payments to receive them (receivables).

The modality of a “firm”, which is any enterprise, including governments and our lemonade-stand, is α=R/P, where (R) is what is owed to us, and (P) is what we owe, and that one number, the modality, α, guarantees that we know everything about those two accounts, (R) and (P), that we need to know from an economic point-of-view, that is, within “the demonstrated societal norms of risk aversion and bargaining practice”.

Figure 3: The Working Capital In-process

The Theory of the Firm develops the “working capital operator”, W(α) = CR(α) – DB(α), which creates payables and receivables, and mediates between them, and shows how the “factors of production” (N*) produce and, in particular, support the “shareholders equity” which we usually call (N) and is the subject of “ownership”; please see the illustration on the right.

Figure 4: Inflation is a discount rate

The “natural rate of inflation” is the “projection”, (1-δ)(1/(1-W)) = (1-δ)(1 + W+W²+W³+…), of the “operator”, 1/(1-W), where W=W(α) for the firm that demonstrates that modality, and the operator, W=W(α), “works” the “float space” of receivables and payables that is created between a firm and its trading connections; please see the illustration on the right.

Extraordinary!

The “numbers” appear to be “extraordinary”, but they’re not – what’s really extraordinary is the “parochialism” of the economists after years of study.

For more information on real “risk management” in modern times and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary and “(P&I) Dividend Risk and Dividend Yield“, and our recent Posts “(P&I) The Profit Box” and “(P&I) The Process – In The Beginning“; and we’ve also profiled hundreds of companies in these Posts and the Search Box (upper right) might help you to find what you’re looking for, such as “(B)(N) TLM Talisman Energy Incorporated” or “(B)(N) ATHN AthenaHealth Incorporated” or “(B)(N) PETM PetSmart Incorporated“, to name just a few.

And for more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice. And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

And for more on what risk averse investing has done for us this year, please see our recent Posts on “(P&I) The Easy (EC) Theory of the Capital Markets” or “(B)(N) The Easy (EC) Theory of the S&P 500“, and the past, The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.