(P&I) The End Of Fixed Income

Liquidity Preference As Behavior Towards Risk – Tobin 1958

Drama. No doubt our thoughts are premature and the “bond play” has some time to run, but where will it run to? And what hope is there for higher interest rates and excessive inflation in the developed economies (Reuters, January 24, 2014, Pimco’s Gross problem: who can succeed the ‘Bond King’)?

However – not to worry – an “investment”, whether it be in bonds, equities or other properties, is just and only the “purchase of risk” and the risk is that we might not get our money back when we need it or that we might not get a rate of return that exceeds the rate of inflation which is just another way of losing our money.

And although “volatility” has nothing to do with that – with capital safety, liquidity and the necessity or hopefulness of a non-negative real return – the most common and prevailing investment strategies, dispersing trillions of dollars in pension plans, endowment and trust funds, are dominated by the heartless, dispirited, mechanics of volatility, co-volatility and diversification with nary a person in it and the sublimely informed bets on credit and interest rates, all of which enrich the investment industry but don’t serve the needs of investors for capital safety, liquidity and a hopeful but not necessarily guaranteed return above the rate of inflation.

James Tobin, the economist, defined the issue quite clearly in a seminal article of 1958, at about the same time that economics came to be dominated by “new tools” in the differential calculus that have only one outcome – optimisation – and its progeny, the “efficient frontier” which doesn’t exist in the normal and real world discourse of commerce and our senses and that make sense to everyone but the economists and their legions of provably naive calculating acolytes – who aren’t investors.

Manhattan Purchase 1626 – 60 guilders in beads, trinkets, knives, blankets and mirror glass – OK

As investors in The RiskWerk Company, we don’t hope to change that – after all, it would be disingenuous not to exploit the natives while we can.

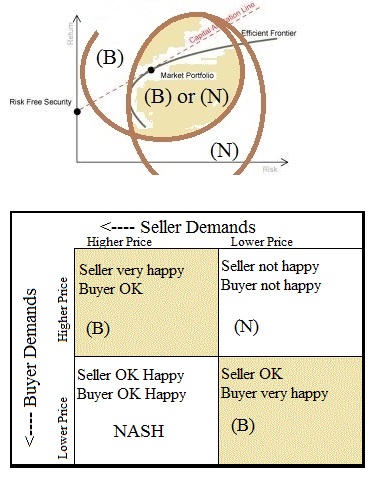

(B)(N) Buyer Happy Seller Happy – OK

But our pictures are quite different.

Instead of a “line in the sand”, we have the open-ended (B)(N)-diagram that defines the mechanics of “risk aversion” and the really efficient frontier.

And instead of volatility, co-volatility and diversification for the sake of “diversification” by the numbers, we calculate the deal at the “price of risk” which is the best deal for buyer and seller alike.

And instead of pinning our hopes on earnings expectation, credit ratings and the seizure of assets that we don’t know how to run, we pin our hopes on the companies that produce the money that we hope to earn.

And we make discoveries such as substitutes for currency and currency itself.

For more information and additional references to the theory, please see our Post, The RiskWerk Company Glossary.

And for more on what risk averse investing has done for us this year, please see our recent Posts on The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.