(P&I) Return Of Earnings

How much would you like today?

Drama. How much of a company’s earnings should be returned to the shareholders? There is no standard for the number and it varies in the S&P 100 companies, for example, between 3× (300%) of the actual earnings to zero to multiples of as much as 100× (10000%) for earnings that don’t even exist, that is, the earnings are negative but the company pays out a dividend anyway.

The question is not an idle one because some investors think that they’re entitled to more (Reuters, January 22, 2014, Icahn blasts Apple again, says bought $3 billion in shares) but the fact is that the companies don’t have to pay out anything to their shareholders.

They don’t have to pay dividends and the most common thing that happens if a company doesn’t pay a dividend or reduces its dividend, is that the stock price drops. So what?

There are some companies that don’t pay dividends at all and investors have not stopped buying them but, instead, have called them “growth companies” and bid up their stock prices by enormous multiples relative to the earnings. Please see Exhibit 1 and 2 below.

Exhibit 1: S&P 100 “Growth” Companies – Fundamentals – January 2014

S&P 100 Growth Companies – Fundamentals – January 2014

Exhibit 2: S&P 100 Undervalued “Growth” Companies – January 2014

S&P 100 Undervalued Growth Companies – January 2014

These six companies have long since “grown up” and are presently valued at $1 trillion, produced $29 billion in earnings last year and returned 8.3% on the shareholders equity.

But the only common way that we can make money on them is to sell what we have at a price that is higher than what we paid for it to some other or new shareholders who might never have owned these companies and had nothing to do with “bringing them up”, so to speak.

And what benefit to the company is in that? None unless they sell some new stock out of treasury and serve the pent-up, excess, demand for their stock.

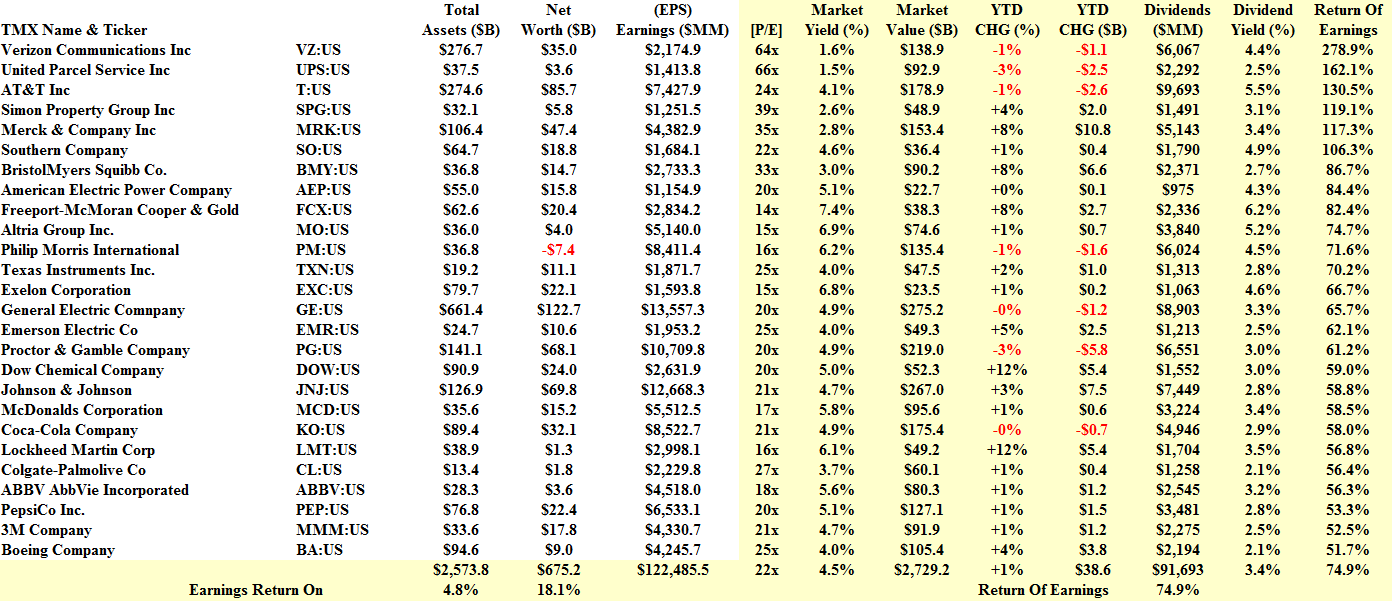

On the other hand, there are twenty-six companies in the S&P 100 that paid out more than 50% of their earnings to the shareholders and we like them even better. Please see Exhibit 3 and 4 below.

Exhibit 3: S&P 100 “Share The Wealth” Companies – Fundamentals – January 2014

S&P 100 Share The Wealth – Fundamentals – January 2014

Exhibit 4: S&P 100 Undervalued “Share The Wealth” Companies – January 2014

S&P 100 Undervalued Share The Wealth Companies – January 2014

These twenty-six companies have an aggregate market value of $2.7 trillion and earned $122 billion last year of which they returned $92 billion to the shareholders for an aggregate return of earnings of 75% and an aggregate dividend yield of 3.4%.

Moreover, the return on the shareholders equity is 18% which is more than twice that of the “Growth” companies (8.3%).

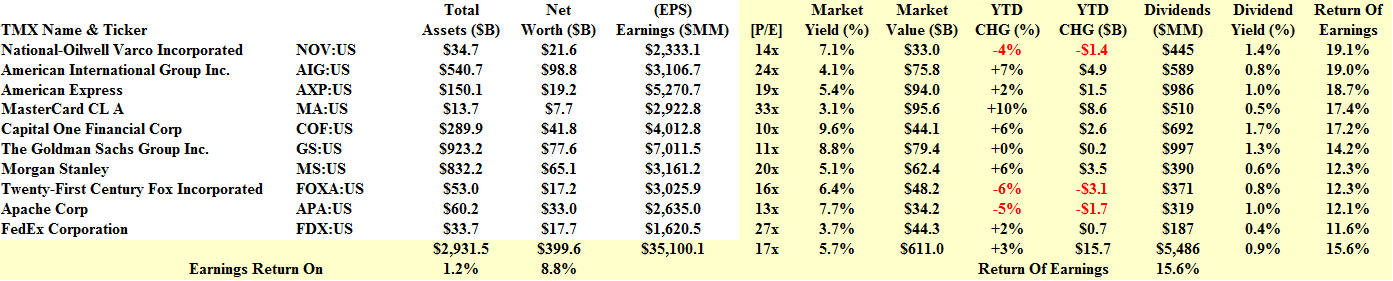

What then of the “misers” – those companies that pay dividends but only return 10% to 20% of their earnings to the shareholders. Please see Exhibit 5 and 6 below.

Exhibit 5: S&P 100 “Misers” – Fundamentals – January 2014

S&P 100 Miser Companies – Fundamentals – January 2014

Exhibit 5: S&P 100 Undervalued “Misers” – January 2014

S&P 100 Undervalued Miser Companies – January 2014

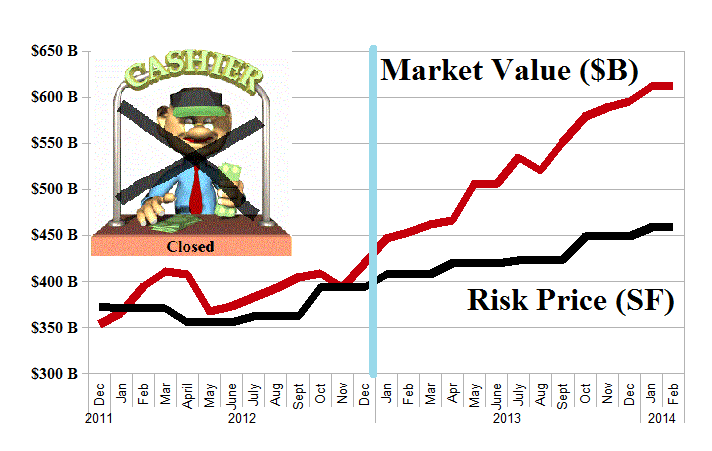

These ten companies, the “Misers”, six of which are banks or financials, earned $35 billion last year but only returned $5.5 billion of it to the shareholders for an aggregate return of earnings of 15%.

The return on the shareholders equity was, however, 8.8% plus a dividend yield of 1% and the market value increased from $440 billion to the current $610 billion for an increase of +23%.

Could it be that some investors don’t know how to earn 10% on their money through their own “enterprise” and rely on companies, however “miserly”, to do it for them?

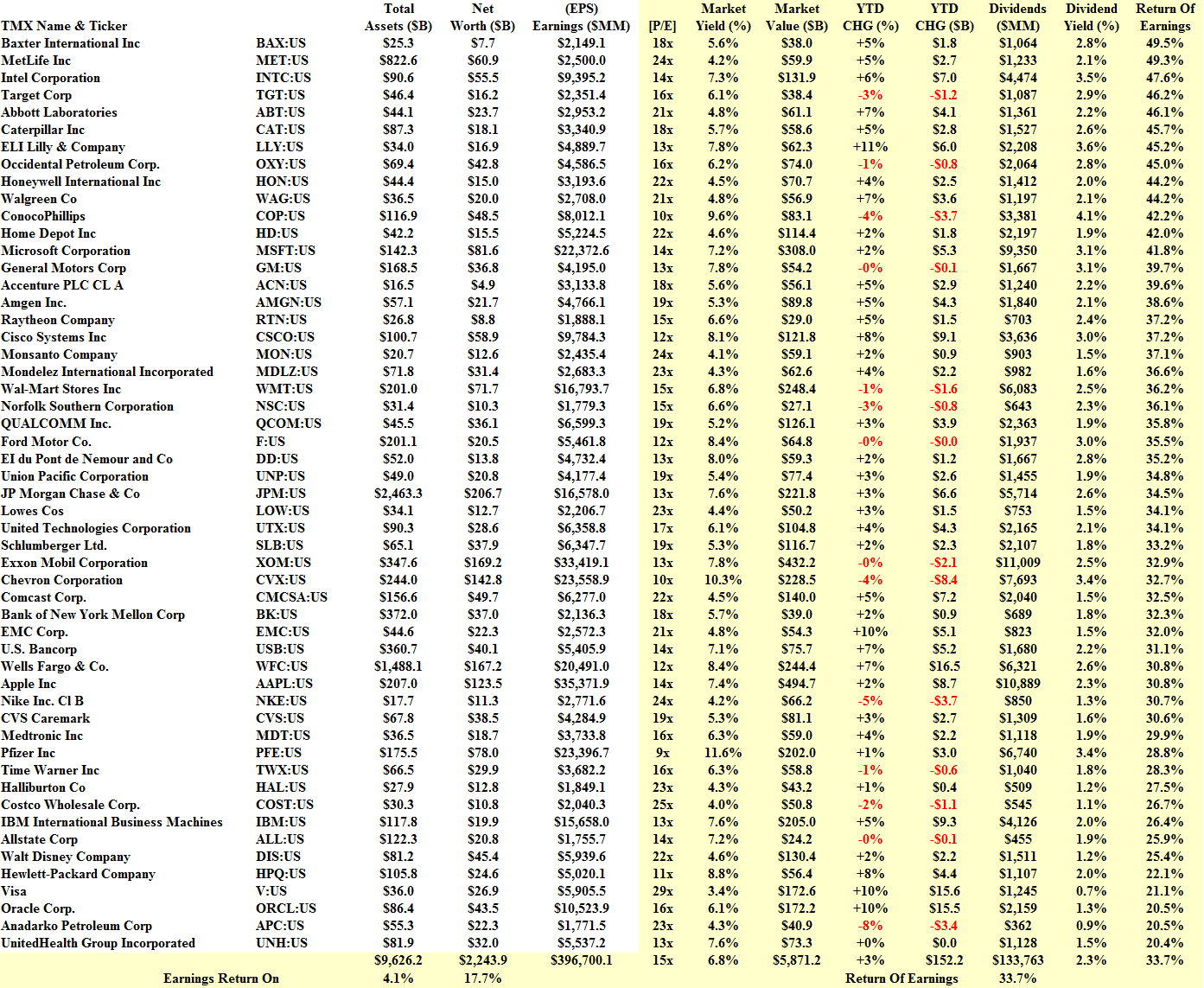

Since we have visited the “growth” companies, “sugar daddies” and the “misers”, what then of those in between that venture to return 20% to 50% of their earnings and whom we might call “prudent”?

Exhibit 6: S&P 100 “Prudent” Companies – Fundamentals

S&P 100 Prudent Companies – Fundamentals – January 2014

Exhibit 7: S&P 100 Undervalued “Prudent” Companies – January 2014

S&P 100 Undervalued Prudent Companies – January 2014

There are 53 companies in the S&P 100 that returned between 20% and 50% of their earnings to the shareholders.

They earned $397 billion last year and paid $134 billion to their shareholders for an aggregate return of earnings of 34% and a dividend yield of 2.3% and the investors have bid up their stock prices from $4.7 trillion last year to the current $5.8 trillion for an increase of +24%.

They also returned 18% on the shareholders equity which is nearly twice what “investors” who also bid on the “misers” seem to think that they can do for themselves.

And one of these “prudent” companies is Apple Incorporated which returned 30% of its earnings and 29% on its shareholders equity but only 7% on its stock price since December 2012.

So what?

Having reviewed all of this and tried to put the best light on shareholder demands for more money, we can only say, so what? We don’t see any evidence of “disservice” to the shareholders in either dividend policy or the payout rate of earnings and our preference is for “prudence”.

After all, if we like the company that much but don’t like the way it’s being run for our benefit, maybe we should buy it and run it ourselves?

For more information and additional references to the theory, please see our Post, The RiskWerk Company Glossary.

And for more on what risk averse investing has done for us this year, please see our recent Posts on The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.