(B)(N) The “W” Syndrome

Figure 1: The “W” Syndrome

Drama. They call it “investing” but it’s nothing of the sort and the entire US market is “wounded”, “confused”, “shocked” and “awed” because they don’t know what’s going to happen next; we call it the “W” Syndrome and the only antidote is to “invest safely” but they don’t know how to do that either – it’s “too expensive”, they say; please see Figure 1 on the right for the “W” Syndrome in the Dow Jones Industrial Companies (and it’s the same story in the S&P 500 companies).

Of course, we always invest safely – we want 100% capital safety guaranteed and a hopeful but not necessarily guaranteed return above the rate of inflation – that’s our definition of “investing” and we know how to get what we want regardless of the market.

But the banks, analysts, and pundits have some other ideas and so we thought that we’d take a look at these random ideas for today for more of that “W”-type action because that’s how the rich get even richer (Bloomberg, June 7, 2016, Fortunes of Ultra-Wealthy to Grow Fastest as Stocks Recover) – and so do we.

Are you buying or selling today? And who is doing it?

The only thing that the companies in today’s “W” Syndrome Portfolio have in common is that “somebody mentioned them for good or ill in some news report today”.

That does not seem like a strong investment criteria and a lot of people would call it reckless or cavalier, but it’s neither reckless nor cavalier and it is as good a standard as any analyst or pundit or bank can give us because they don’t make their money by being right even half of the time (witness the “W” Syndrome) but just by being because investments are sold and not bought and this portfolio is probably a typical portfolio for a lot of people who have been sold and are buying them for good or ill (a long or short position).

But the fact is that it doesn’t matter what we buy as long as we “invest” in it and in our case, “investing” means that we have to run it as a (B)-class portfolio because (in our case) investments are always bought but never sold until the market tells us what they want to pay for the stocks that we own and we’re stopped-out on them; please see below.

It’s about me?

To put it another way, the “stock market” is not about the companies in it – those are just the assets, the “inventory”, and the “underlying” – the market is really about you, the wannabe “investor”, and what you will buy or sell at which prices, and how much money you have to spend on your idea.

The “W” Syndrome Portfolio

These are all great companies – about thirty of them, just check their websites – and they’ve all been run up by the investors for reasons which we’ll never know; and they’ve all been run down for some other reasons which we’ll also never know because in all of that “investor” action, these companies continue to open their doors every day and do what they’re good at.

However, we never buy the stock of a company for which we don’t know the “price of risk” and for which we can’t establish an active and aggressive stop/loss policy which can be implemented in several ways depending on our needs for liquidity; please see the examples below.

The “price of risk” is defined by the Theory of the Firm and can be most colorfully described as “the least stock price at which a company is likeable” (Goetze 2006); it’s a calculation in the Theory of the Firm and it’s never zero unless we’re thinking about buying the common stock of a bankrupt company (and even then there could be an active market for the stock), and the theory provides us with an easy to use “heuristic” which we usually describe as “a stock chart, a ruler, and a good eye” and that’s something that anybody can learn and apply to any stock, mutual fund, or ETF.

Of these thirty-one companies, all of them are “investment grade” today by our standard, but for four of them (Under Armour Incorporated, Apple Incorporated, PayPal, and Foot Locker) which are on our “watch list” for more good than ill.

In aggregate, these companies have a current market value of $2.7 trillion and they returned 18% on the shareholders equity ($554 billion) last year whereas most mutual funds, ETFs, and hedge funds returned net nothing (or less) last year but for a few “accidents”; and they earned $100 billion last year and gave 30% of it to the shareholders for a current dividend yield of 1.15%.

We don’t know if they’ll do it again this year, nor do we know what the investors will pay for that whether they do or don’t, but we have to “invest” – we need an income from our money and we can’t pay our bills in cash for long – and that’s our problem for today; please click on the illustrations below and again to make them larger as required.

Exhibit 1: (B)(N) The “W” Syndrome Portfolio

Figure 1.1: AGU Agrium Incorporated (B+) |

Figure 1.2: GOOGL Alphabet Incorporated Class A (B+) |

Figure 1.3: AMZN Amazon.com Incorporated (B+) |

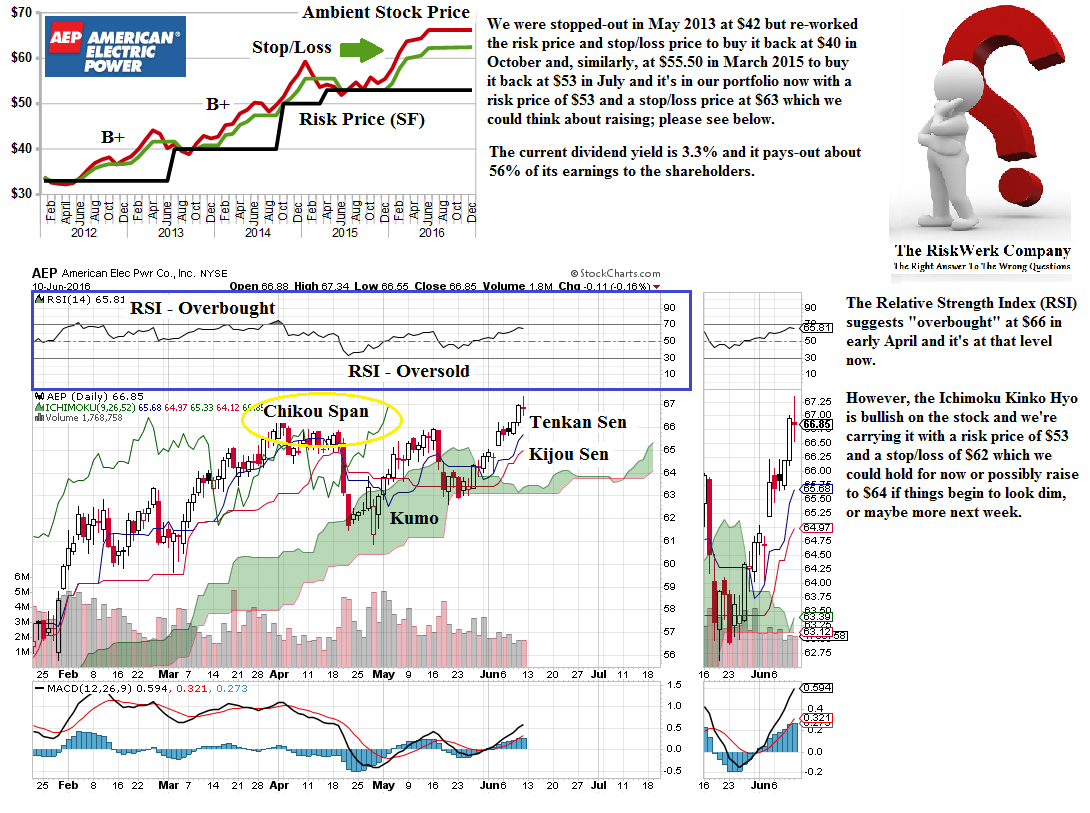

Figure 1.4: AEP American Electric Power Company Incorporated (B+) |

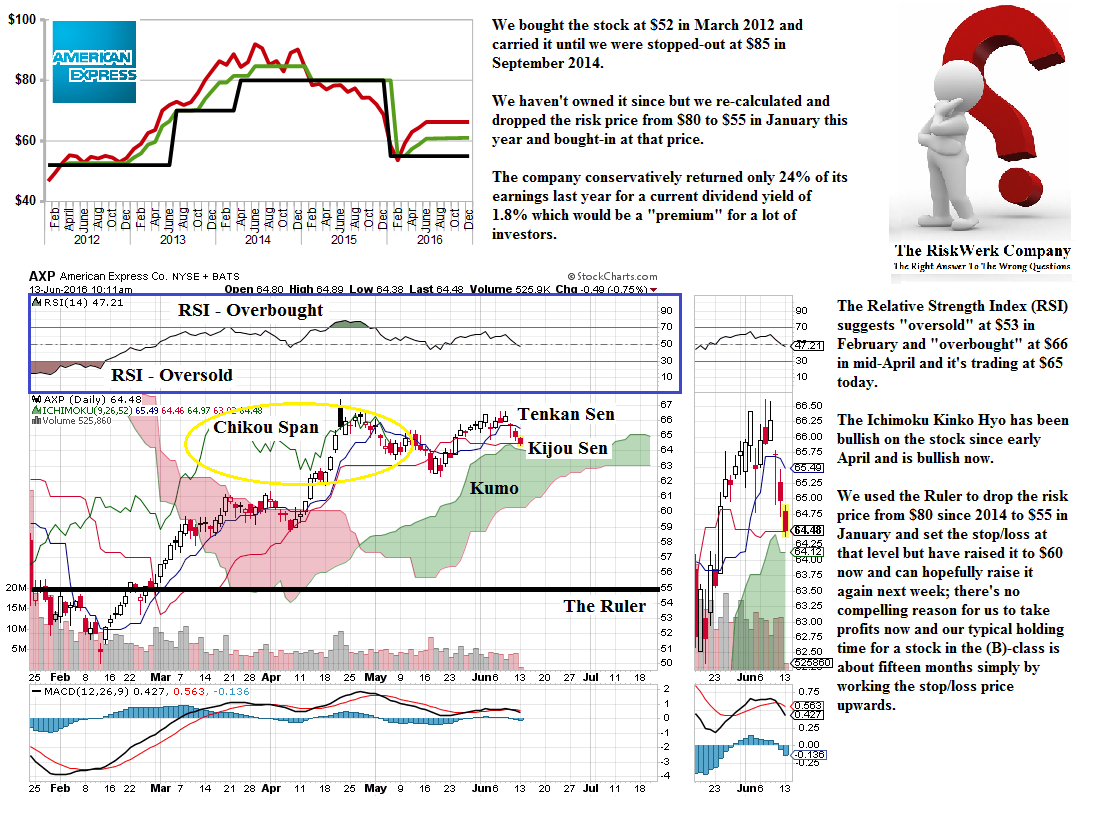

Figure 1.5: AXP American Express Company (B+) |

Figure 1.6: BUD AnheuserBusch InBev SA NV ADR (B+) |

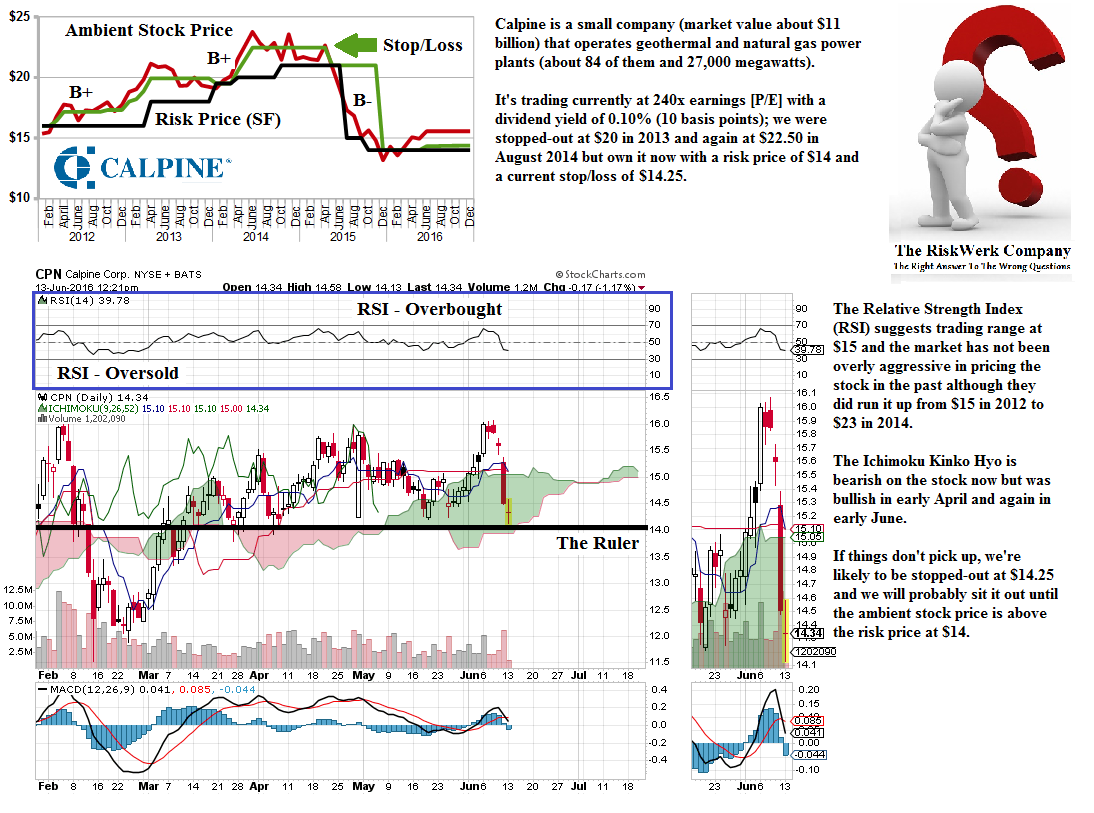

Figure 1.7: CPN Calpine Corporation (B+) |

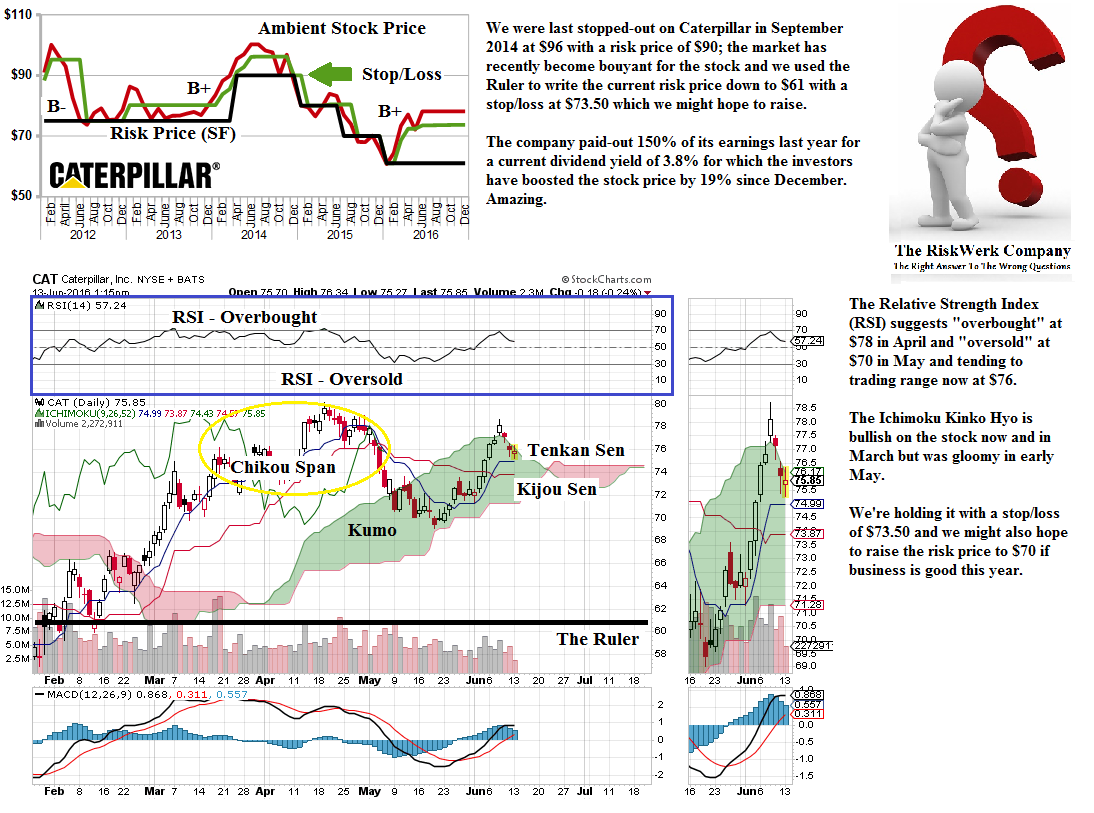

Figure 1.8: CAT Caterpillar Incorporated (B+) |

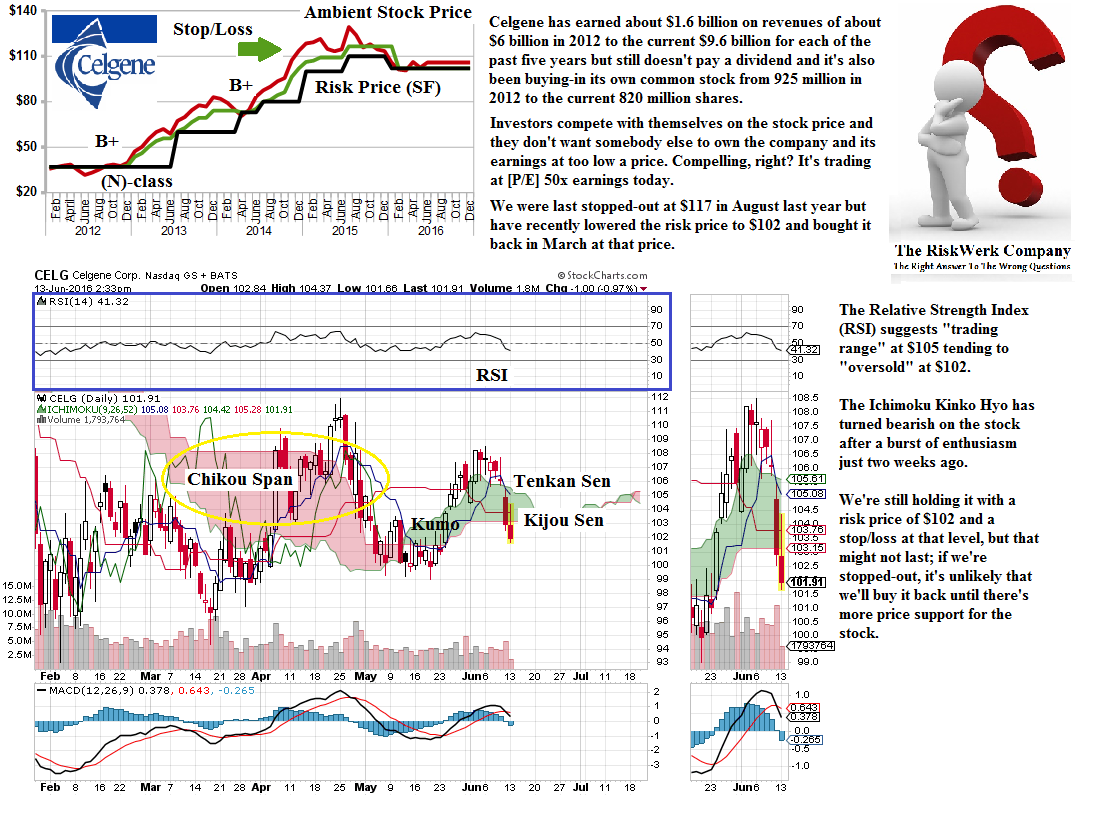

Figure 1.9: CELG Celgene Corporation (B+) |

Figure 1.10: STZ Constellation Brands Incorporated (B+) |

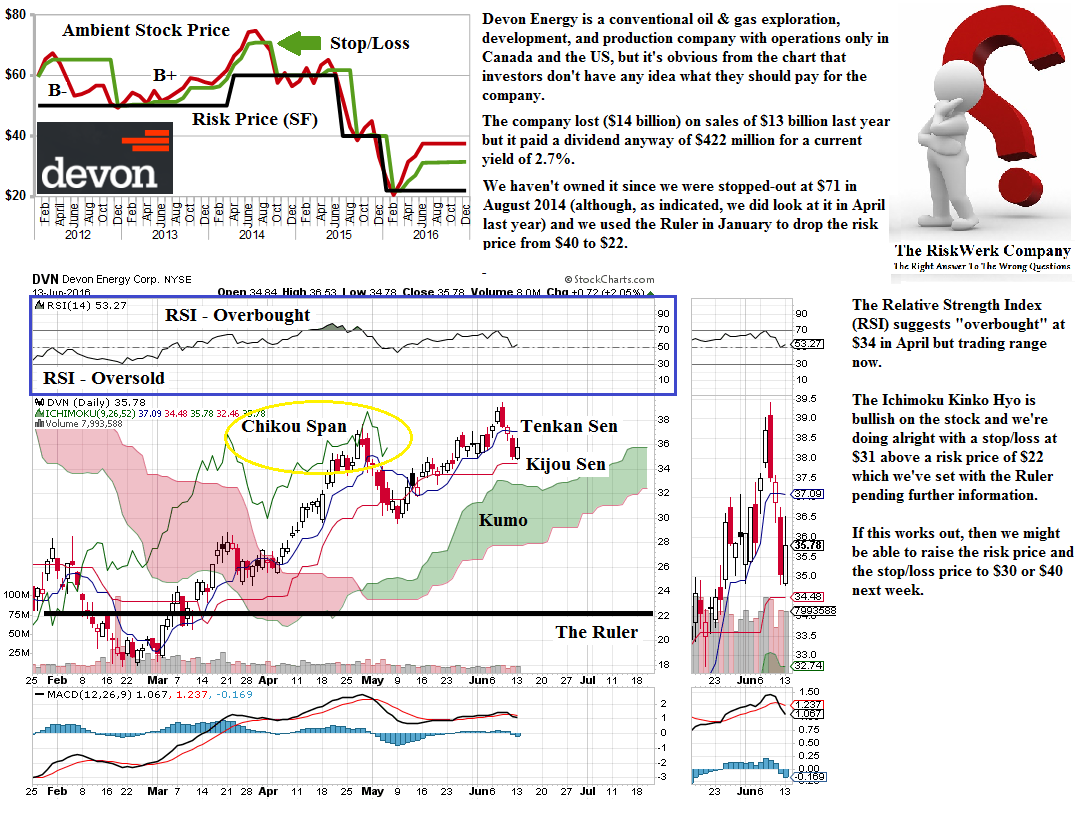

Figure 1.11: DVN Devon Energy Corporation (B+) |

Figure 1.12: FB Facebook Incorporated Class A (B+) |

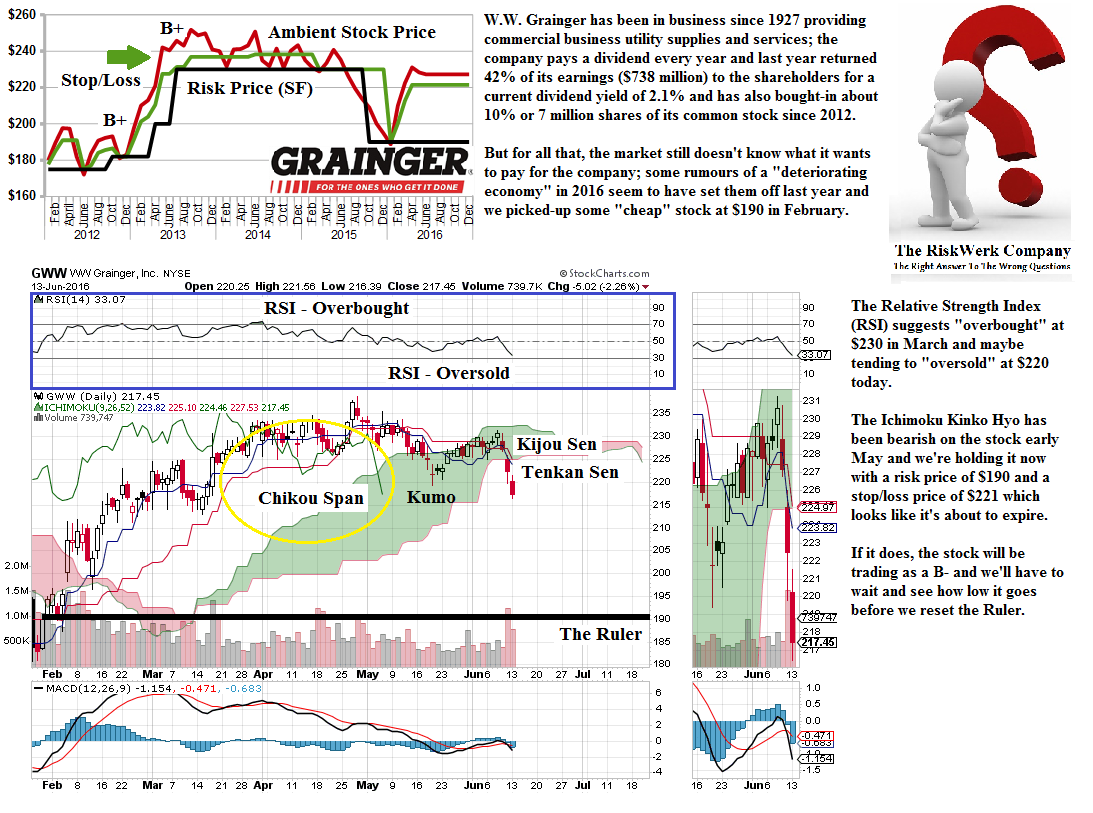

Figure 1.13: GWW W.W. Grainger Incorporated (B+) |

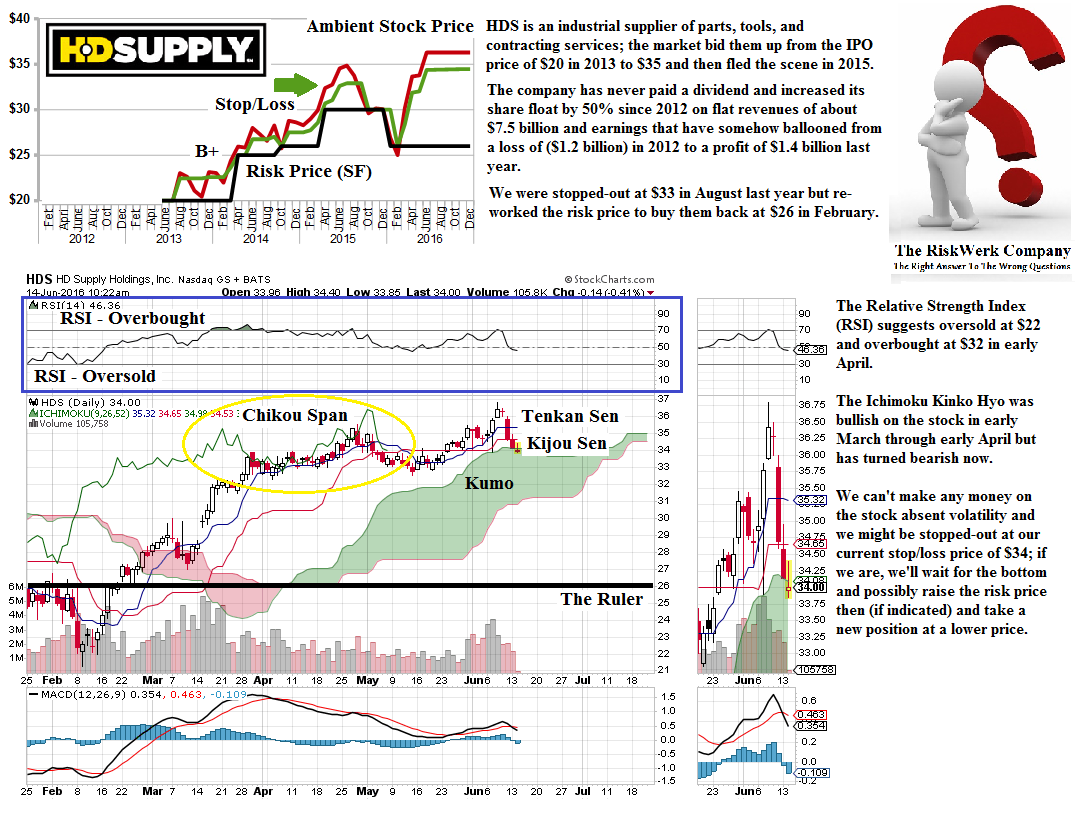

Figure 1.14: HDS HD Supply Holdings Incorporated (B+) |

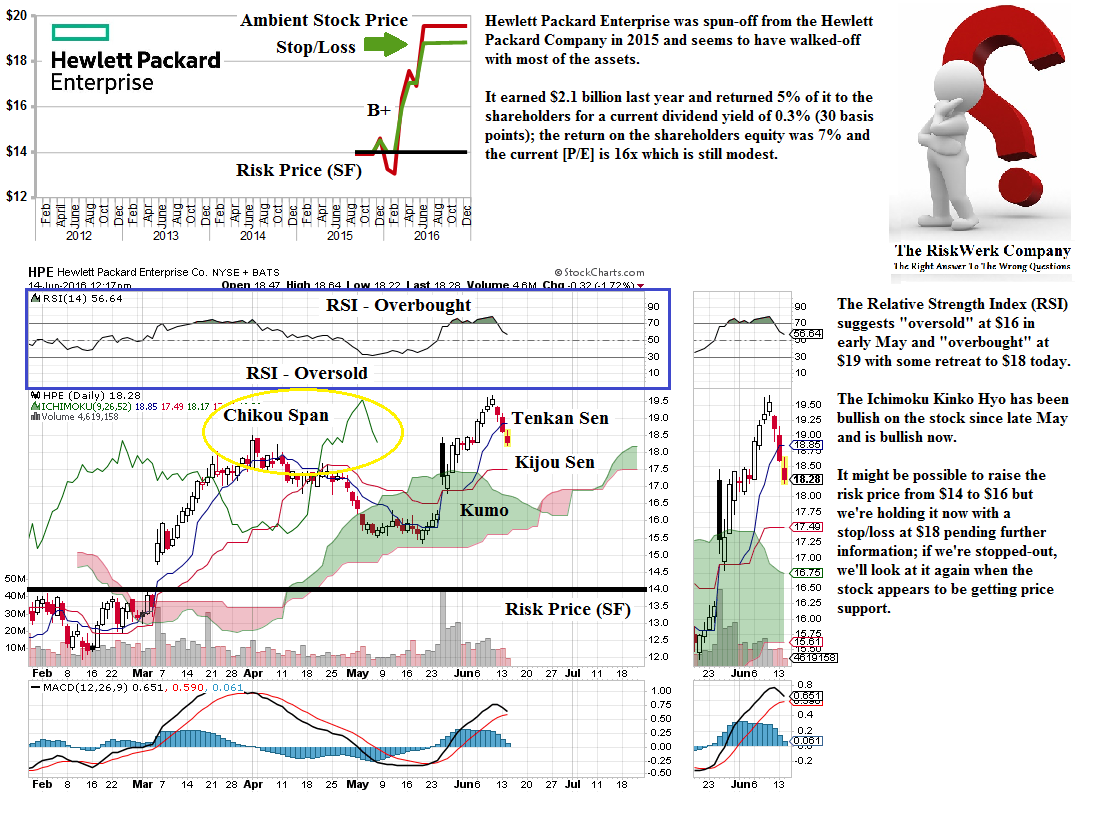

Figure 1.15: HPE Hewlett Packard Enterprise Company (B+) |

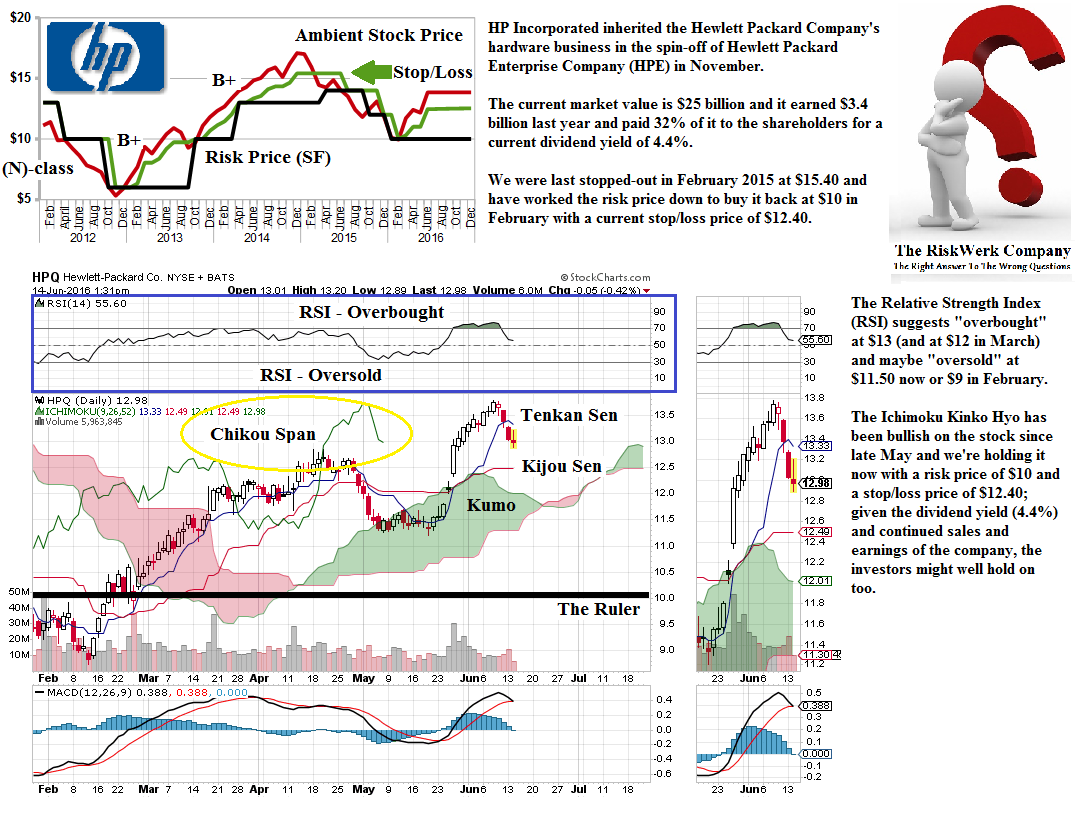

Figure 1.16: HPQ HP Incorporated (B+) |

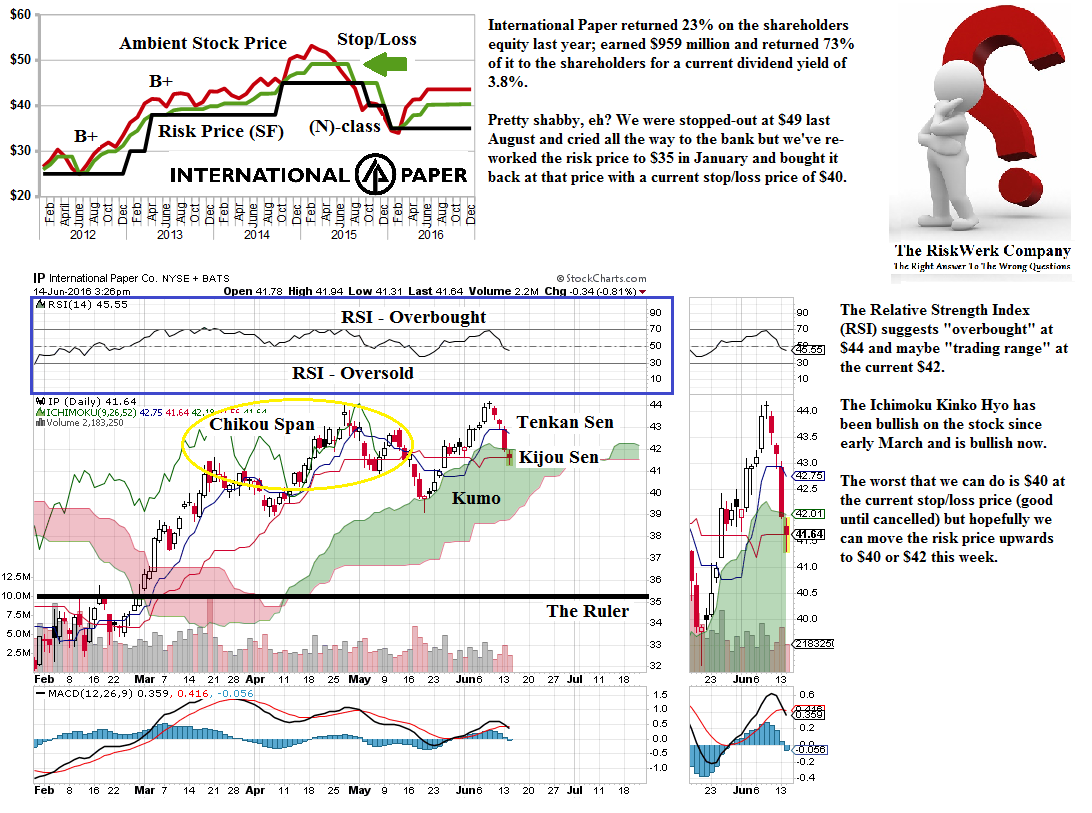

Figure 1.17: IP International Paper Company (B+) |

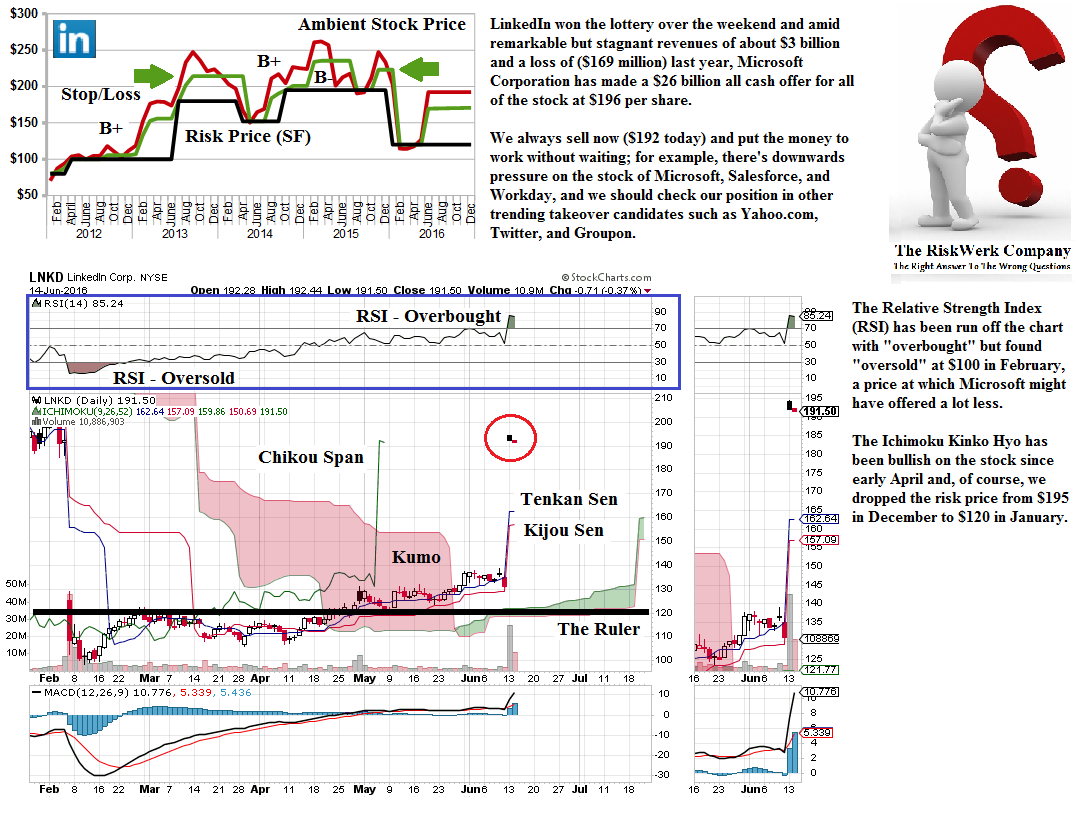

Figure 1.18: LNKD LinkedIn Corporation Class A (B+) |

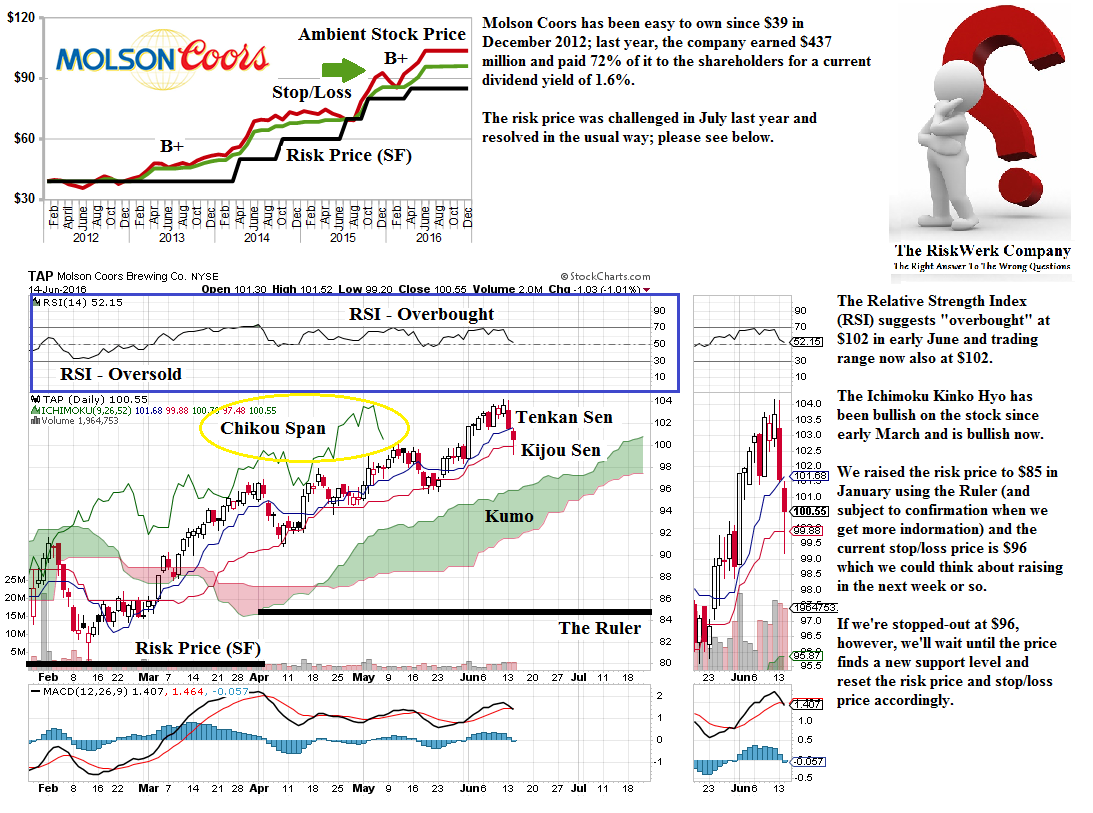

Figure 1.19: TAP Molson Coors Brewing Company Class B (B+) |

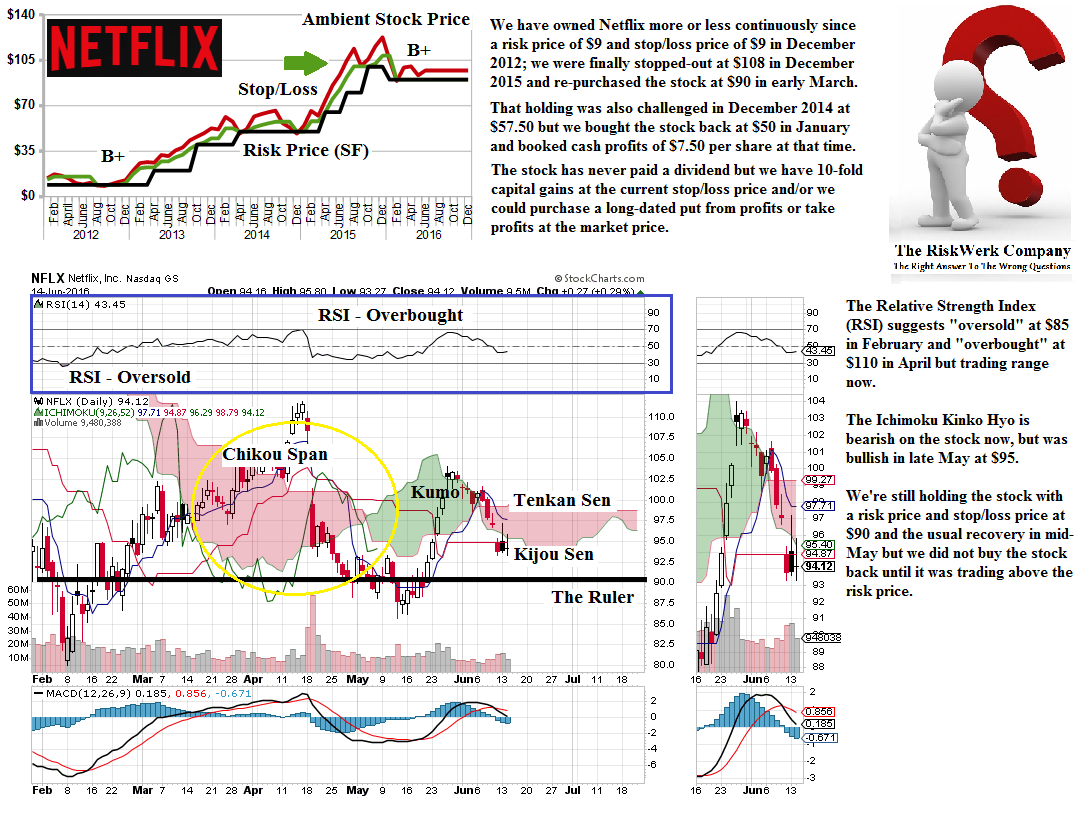

Figure 1.20: NFLX Netflix Incorporated (B+) |

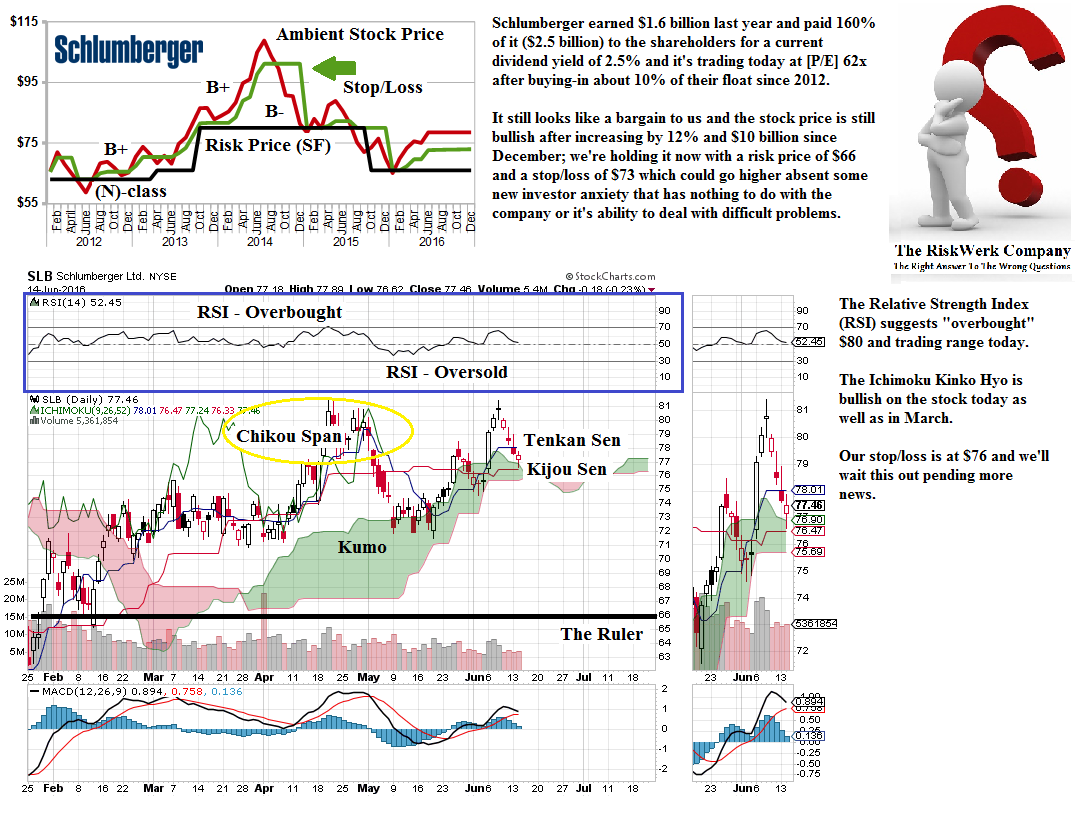

Figure 1.21: SLB Schlumberger Limited (B+) |

Figure 1.22: SGYP Synergy Pharmaceuticals Incorporated (B+) |

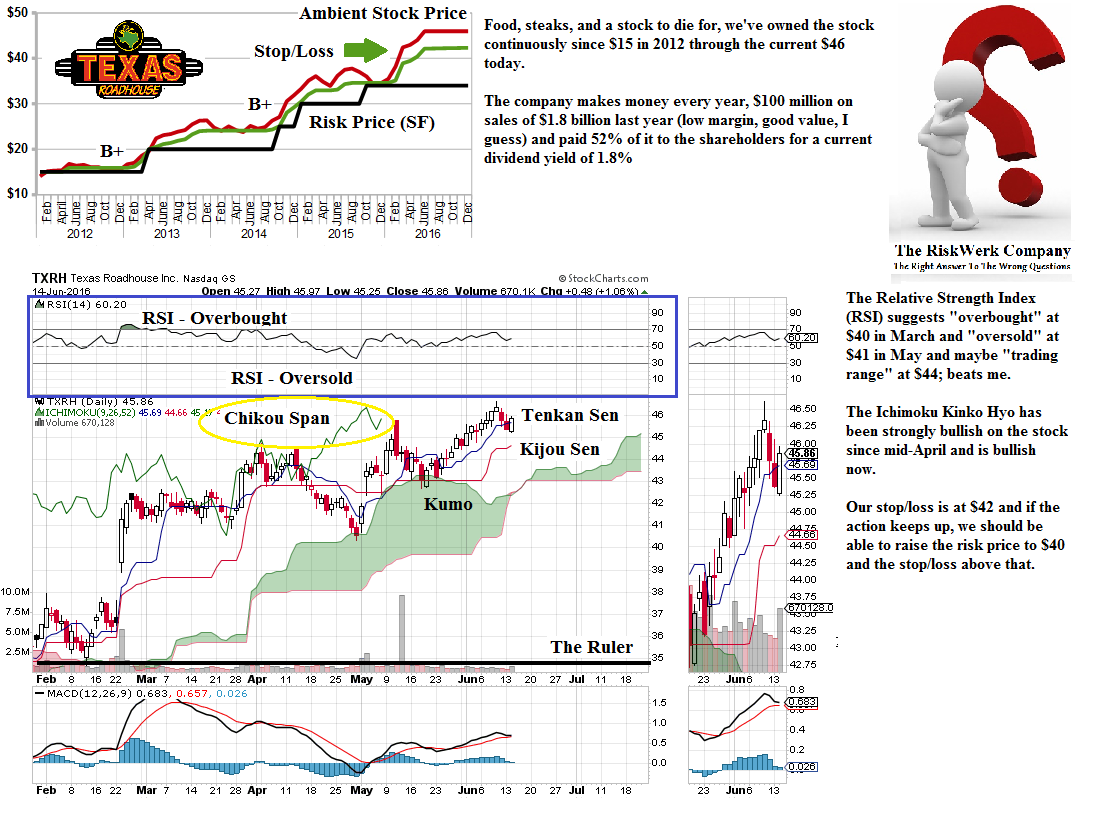

Figure 1.23: TXRH Texas Roadhouse Incorporated (B+) |

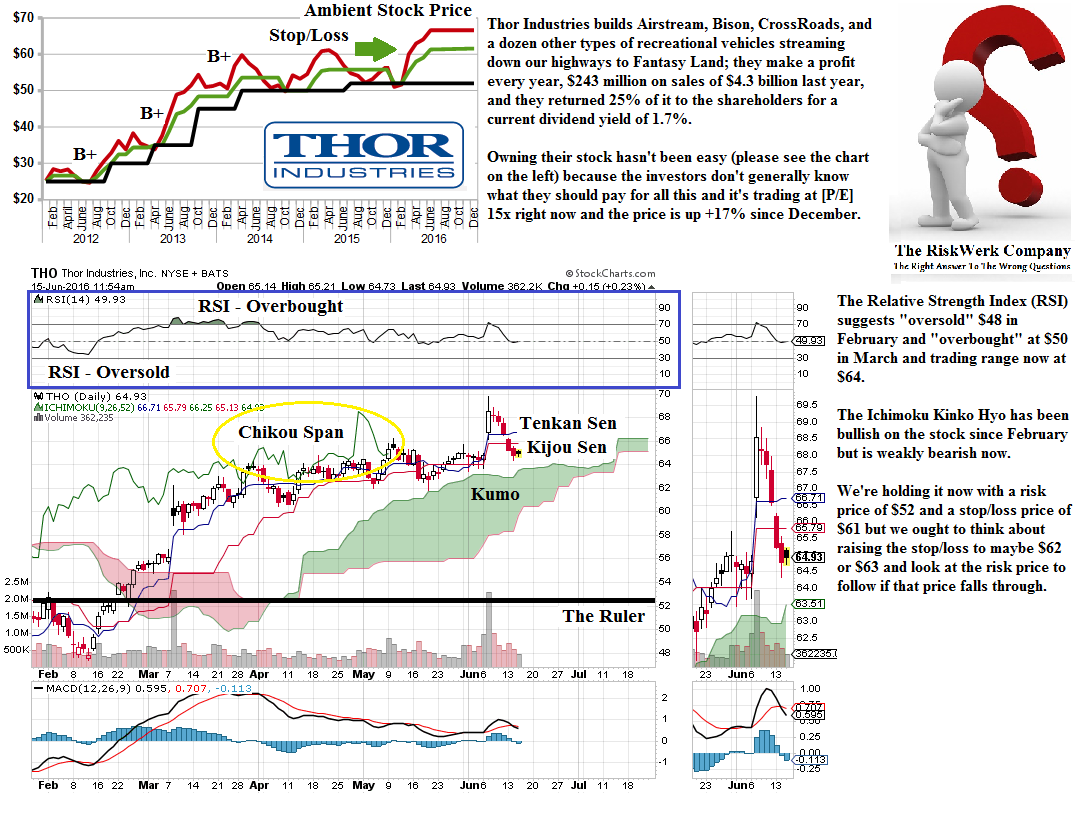

Figure 1.24: THO Thor Industries Incorporated (B+) |

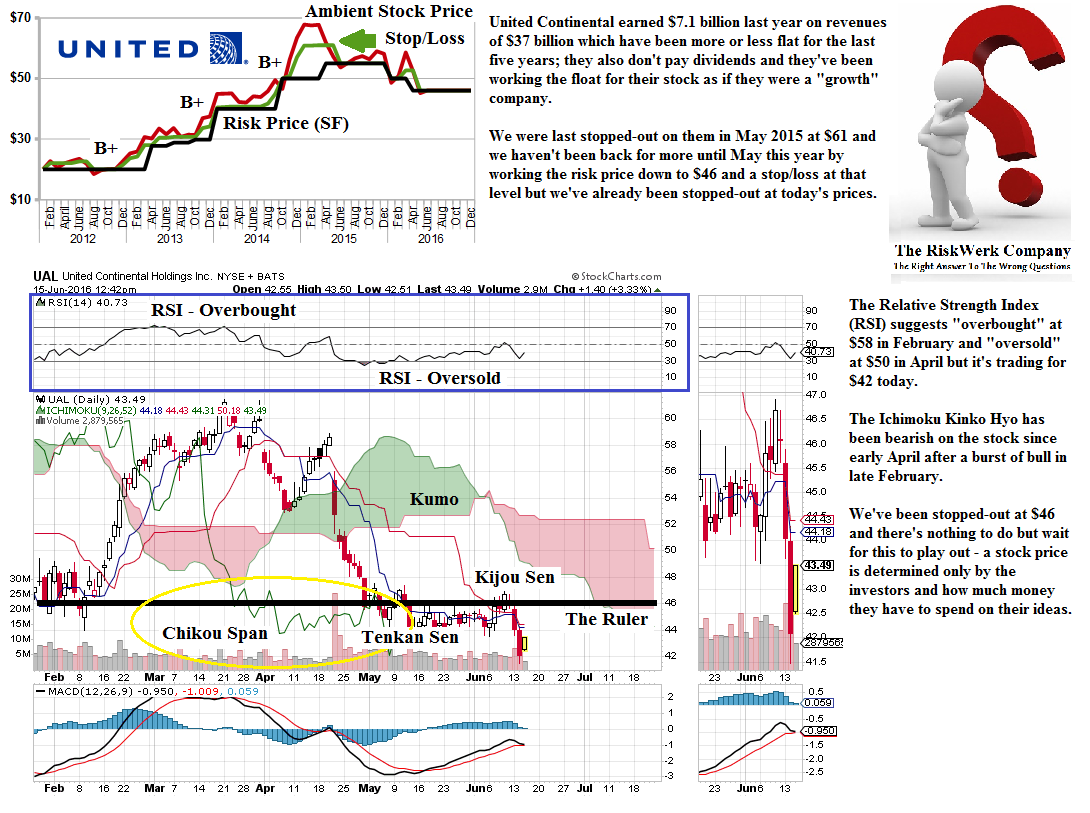

Figure 1.25: UAL United Continental Holdings Incorporated (N) |

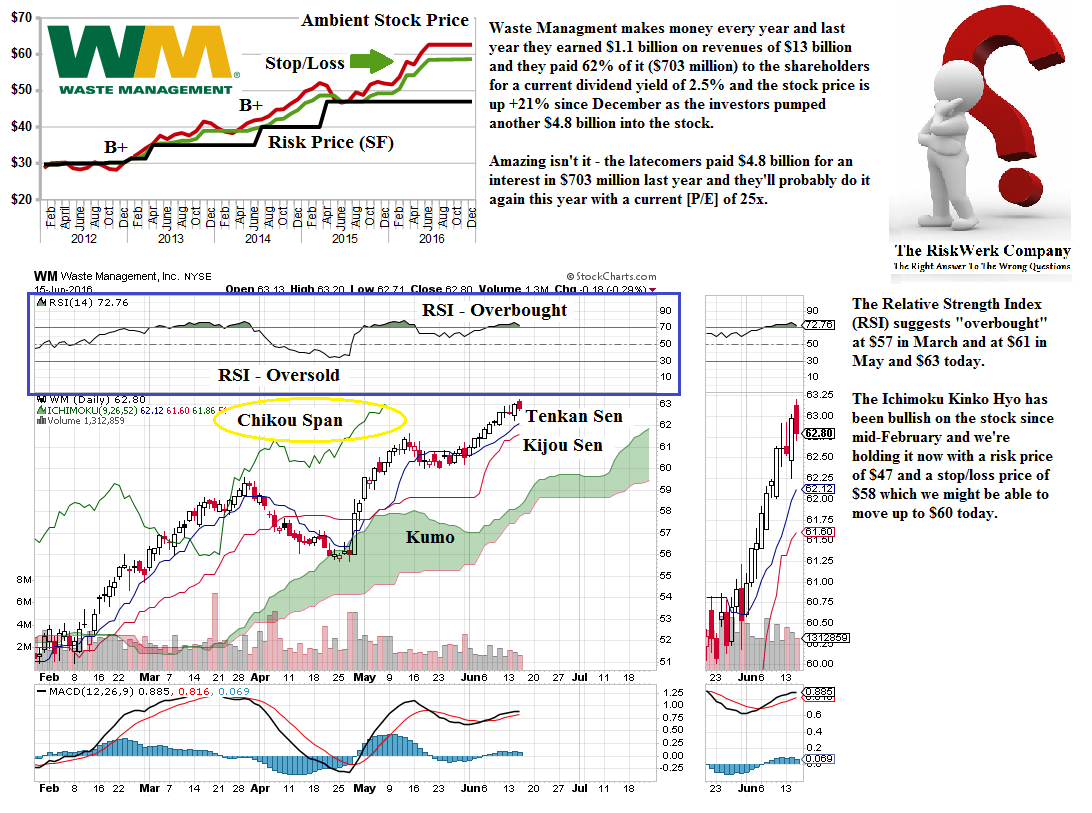

Figure 1.26: WM Waste Management Incorporated (B+) |

Figure 1.27: UA Under Armour Incorporated Class A (N) |

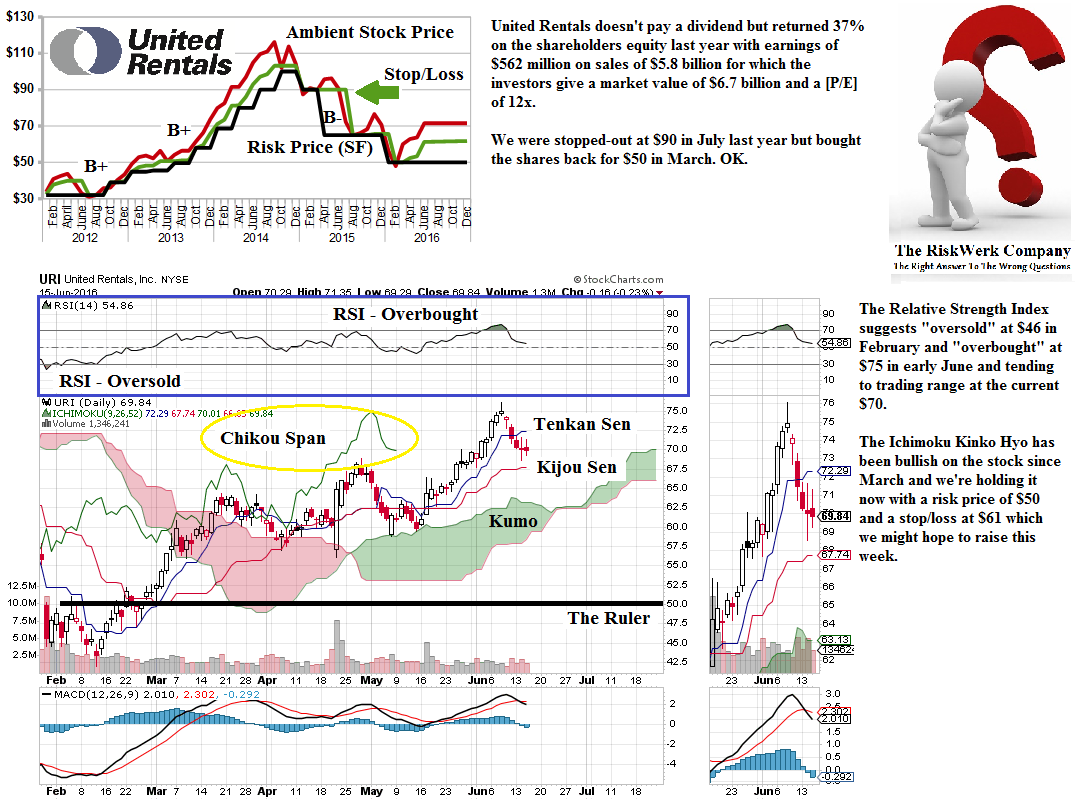

Figure 1.28: URI United Rentals Incorporated (B+) |

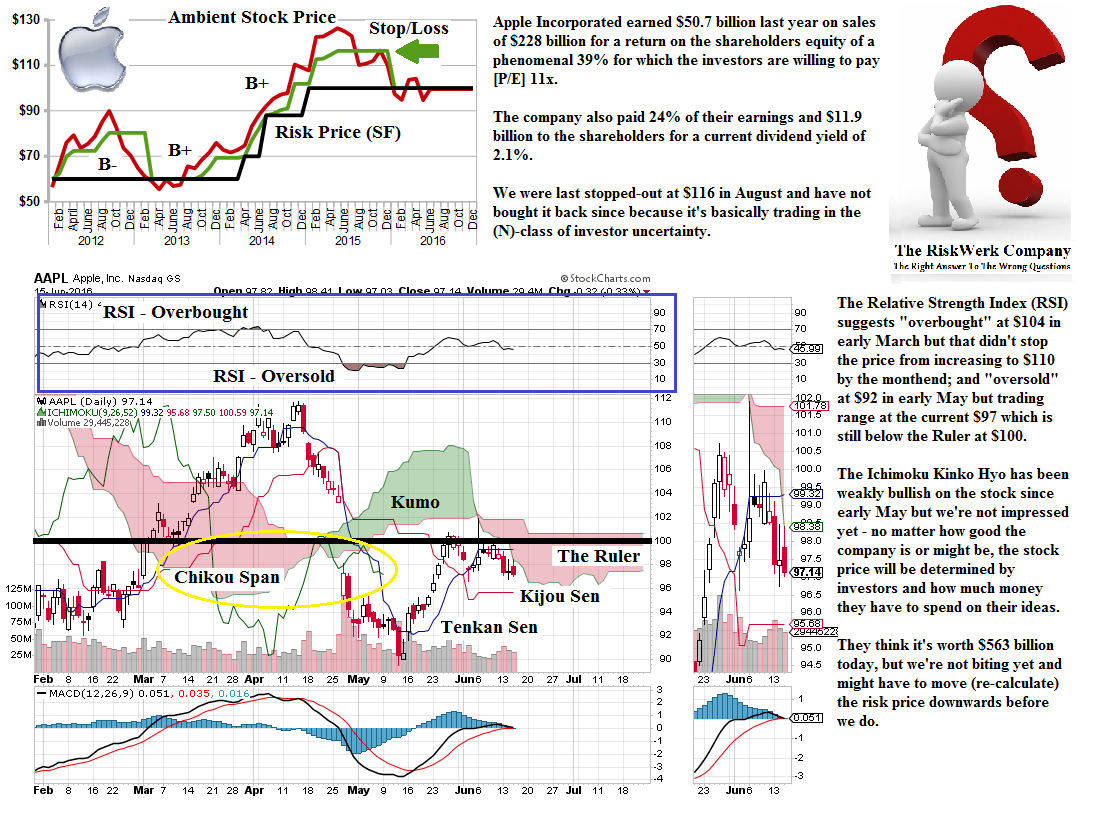

Figure 1.29: AAPL Apple Incorporated (N) |

Figure 1.30: PYPL PayPal Holdings Incorporated (N) |

For more examples of the (B)-class portfolio in difficult markets, please see our recent Posts on Steel, Green Energy and The Coal War; the Canadian Mines have also taken-off – please see our recent Post “(B)(N) Extreme Economics – The (New) Canadian Mines” for a heads-up on that.

And for more information and examples of the Free Market Yield and the terms that we have used above, please see our Posts “(P&I) The Dismal Equation (Ecclesiastes 9:1)” and “(B)(N) S&P 100 Volatility Risk and The Full Moon” and “(B)(N) NASDAQ 100 Volatility and The Stone Bunnies“ and for an introduction to The Barometer “(B)(N) What’s A Girl To Do” or “(P&I) The Swiss Franc Debacle“.

And for more information on real “risk management” in modern times and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary and “(P&I) Dividend Risk and Dividend Yield“, and our recent Posts “(P&I) The Profit Box” and “(P&I) The Process – In The Beginning“; and we’ve also profiled hundreds of companies in these Posts and the Search Box (upper right) might help you to find what you’re looking for, such as “(B)(N) TLM Talisman Energy Incorporated” or “(B)(N) ATHN AthenaHealth Incorporated” or “(B)(N) PETM PetSmart Incorporated“, to name just a few.

And for more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice. And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

And for more on what risk averse investing has done for us this year, please see our recent Posts on “(P&I) The Easy (EC) Theory of the Capital Markets” or “(B)(N) The Easy (EC) Theory of the S&P 500“, and the past, The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”). The Canada Pension Bond®™, The Medina Bond®™, The Barometer®™, the Free Market Yield®™ and Extreme Economics®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.