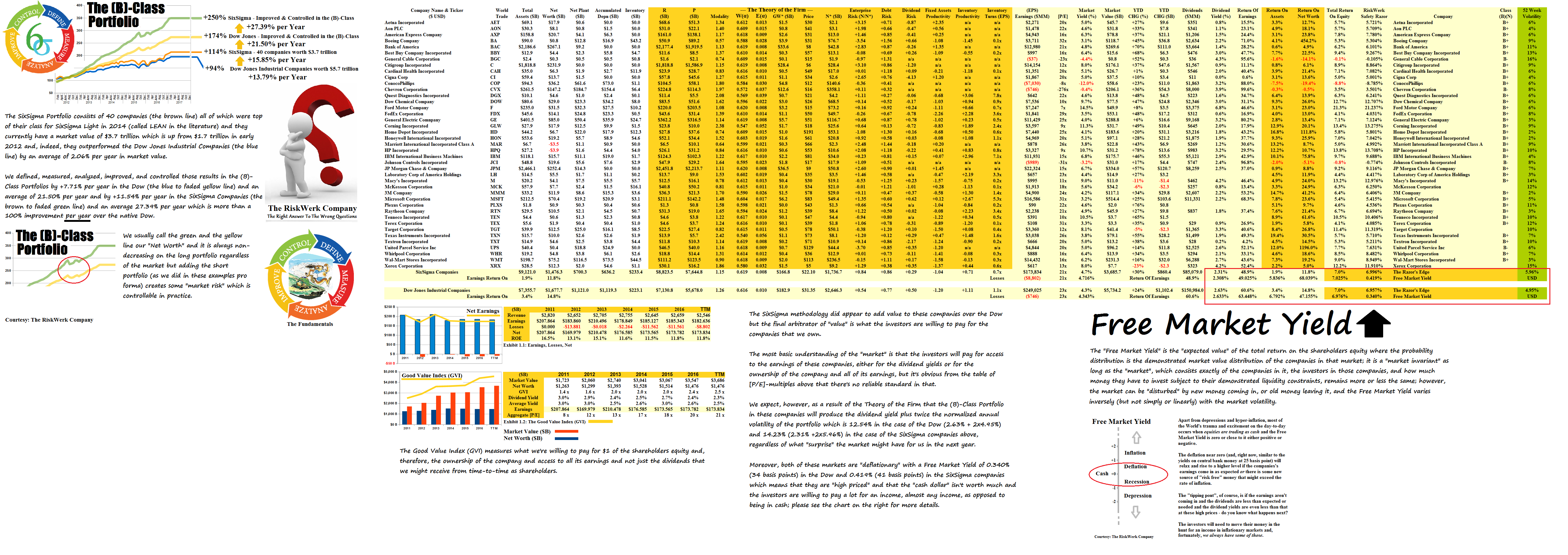

(B)(N) The Fastest Food in America

Good for Six Sigmas

Drama. There are some cost-cutting wizards afoot who think that trimming the operating costs and tightening-up the management and service staff in fast food will boost the “shareholder value“.

But how much “shareholder value” do they expect to create if the investors don’t really know what they should pay for a company or its stock or its earnings (please see below)?

And even the Gold Standard of smart management, Six Sigma, doesn’t add-up to much more “shareholder value” although we can hope that it will create more and better jobs than in the absence of a chorus and a choir to sing it and we can hope that what’s done today won’t come undone tomorrow.

There’s a similar fiction in governments which think that they’re doing their job and should be paid for it by “balancing budgets” but even Henry Ford knew that it was a good idea to pay your employees more so that they could afford to buy your cars and one of the last companies to make “buggy whips” made the best buggy whips ever before it filed for bankruptcy (The New York Times, January 9, 2010, Failing Like a Buggy Whip Maker? Better Check Your Simile).

However, the chart below shows that SixSigma did indeed add value – about 2% per year above the Dow which is a 15% improvement over the Dow’s 14% per year average returns for the last five years.

But adding the (B)-Class portfolio and working the investors and their money regardless of what they were investing in almost doubled the Dow to an average of 27% per year and a more than six-fold improvement (100% over 15%) and Six Sigmas of “shareholder value” with no capital risk at all.

And we were paid to do that and we can do it again today in the same way; please see below and click on the illustrations and again to make them larger as required.

Exhibit 1: The Six Sigmas and the (B)-Class Portfolio

The Fastest Food in America

The thirty companies in our fast food portfolio are already adding a lot of value to the ownership; that is, they’re competitive with both the Dow and the SixSigma companies above and they have a current aggregate dividend yield of 2.6% and [P/E]-multiple of 30x which beats both the Dow (2.6% and 23x) and the SixSigma companies (2.3% and 21x) in their market value and what the investors are willing to pay for it.

But we’re also expecting a very tough investment year this year because all of these companies, in aggregate, are showing deflationary Free Market Yields in the range of 30 to 50 basis points and very low expected price volatilities in the range of 5% to 6% this year which will limit our profits to about 15% (the dividend rate plus twice the expected volatility) in the absence of “special situations” such as the evangelists (as above) who might show-up in our otherwise free markets and want to mess with our fast food.

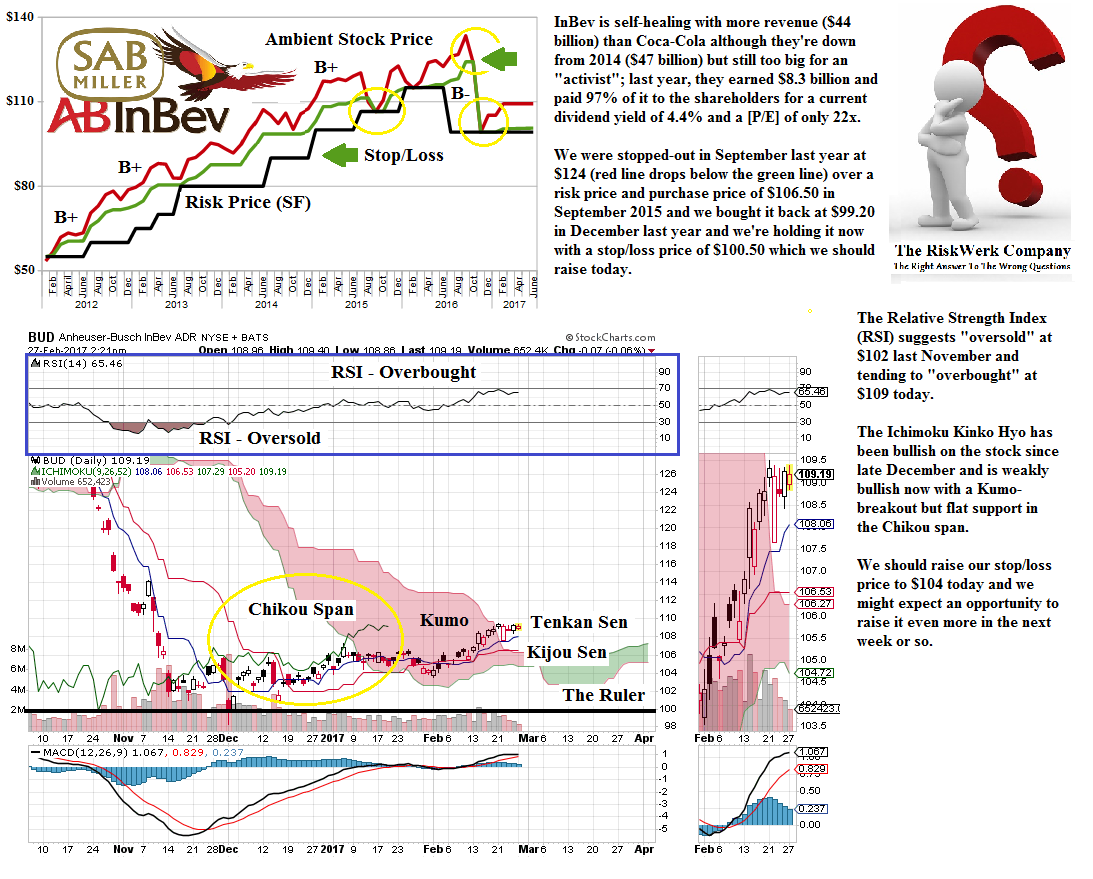

Exhibit 2.1: BUD Anheuser-Busch InBev SA NV (B+) |

Figure 2.2: AEFES.IS Anadolu Efes (B+) |

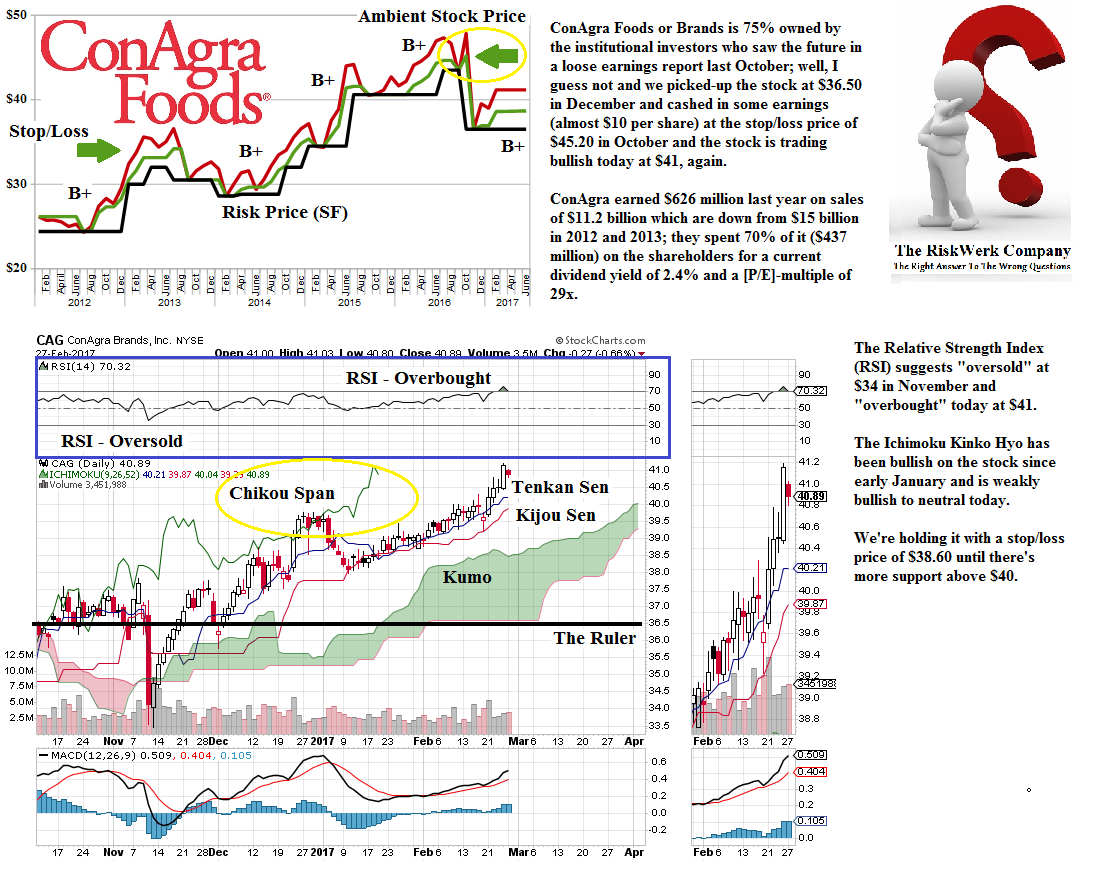

Figure 2.3: CAG ConAgra Foods Incorporated (B+) |

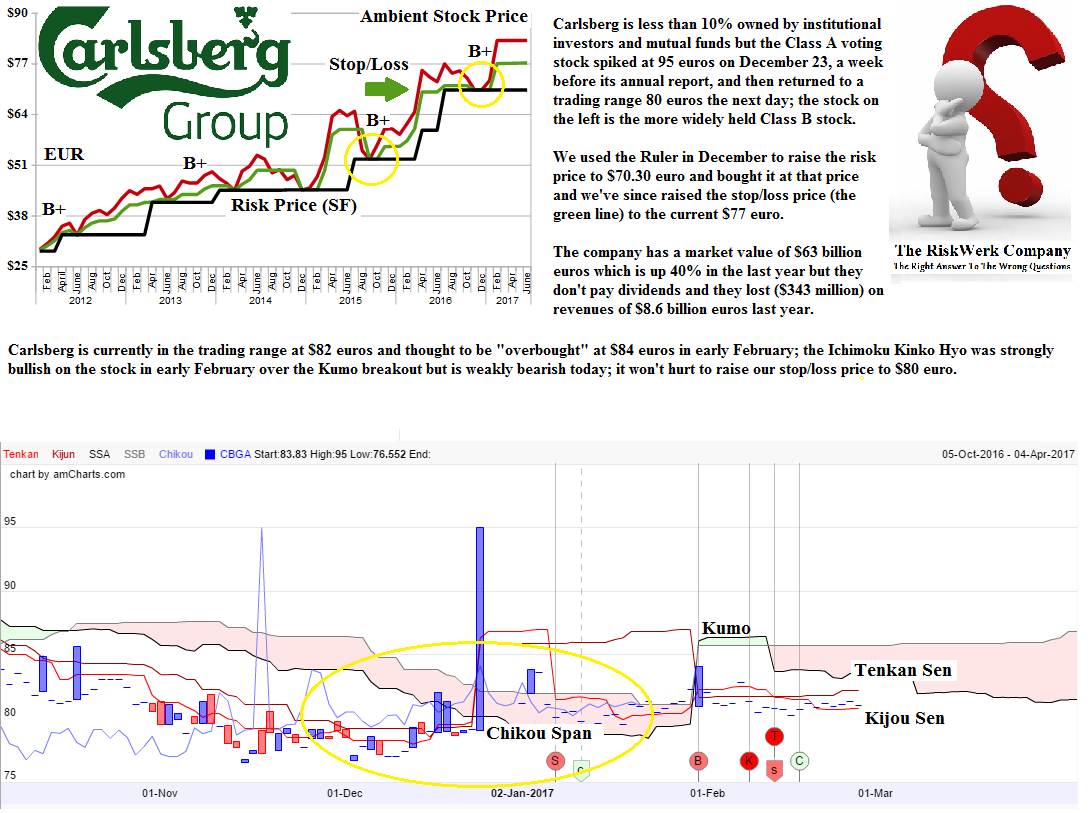

Figure 2.4: CBGB.F Carlsberg AS Class B ADR (B+) |

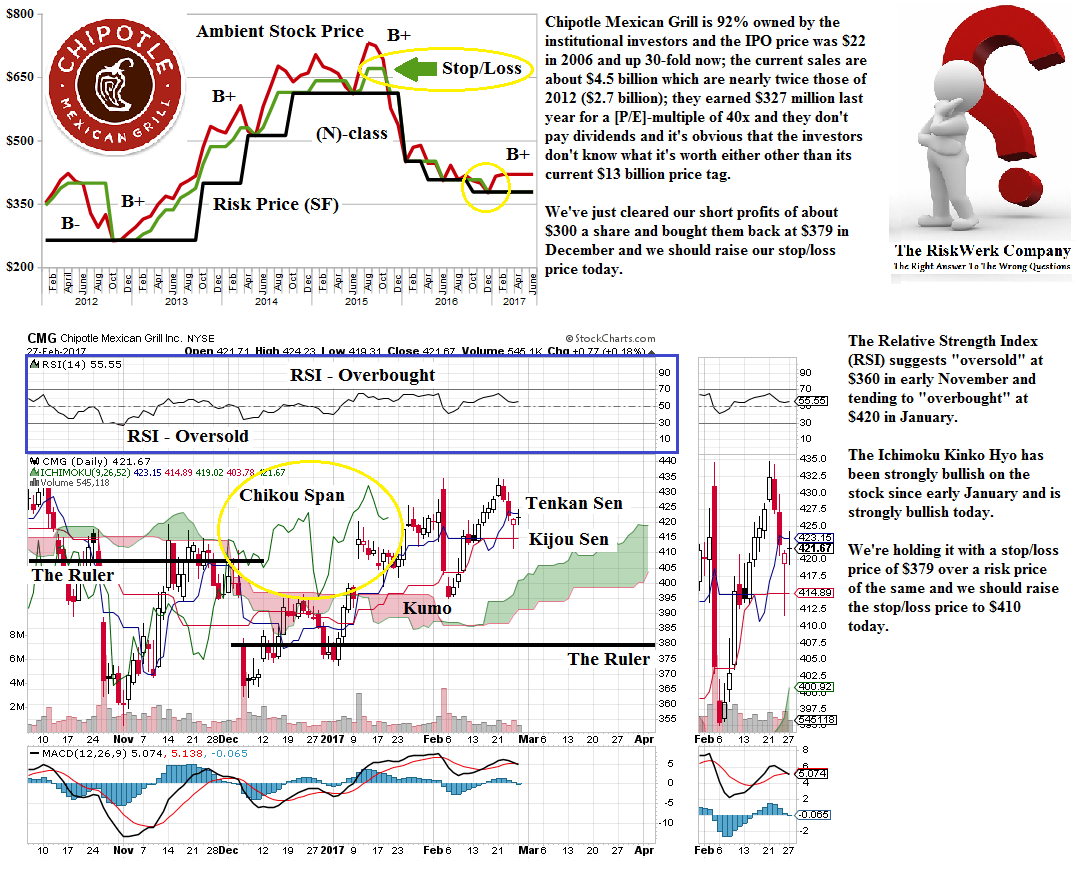

Figure 2.5 CMG Chipotle Mexican Grill (B+) |

Figure 2.6: CPB Campbell Soup Company (B+) |

Figure 2.7 DEO Diageo PLC ADS (B+) |

Figure 2.8: GIS General Mills Incorporated (B+) |

Figure 2.9: HEIA.AS Heineken NV ADR |

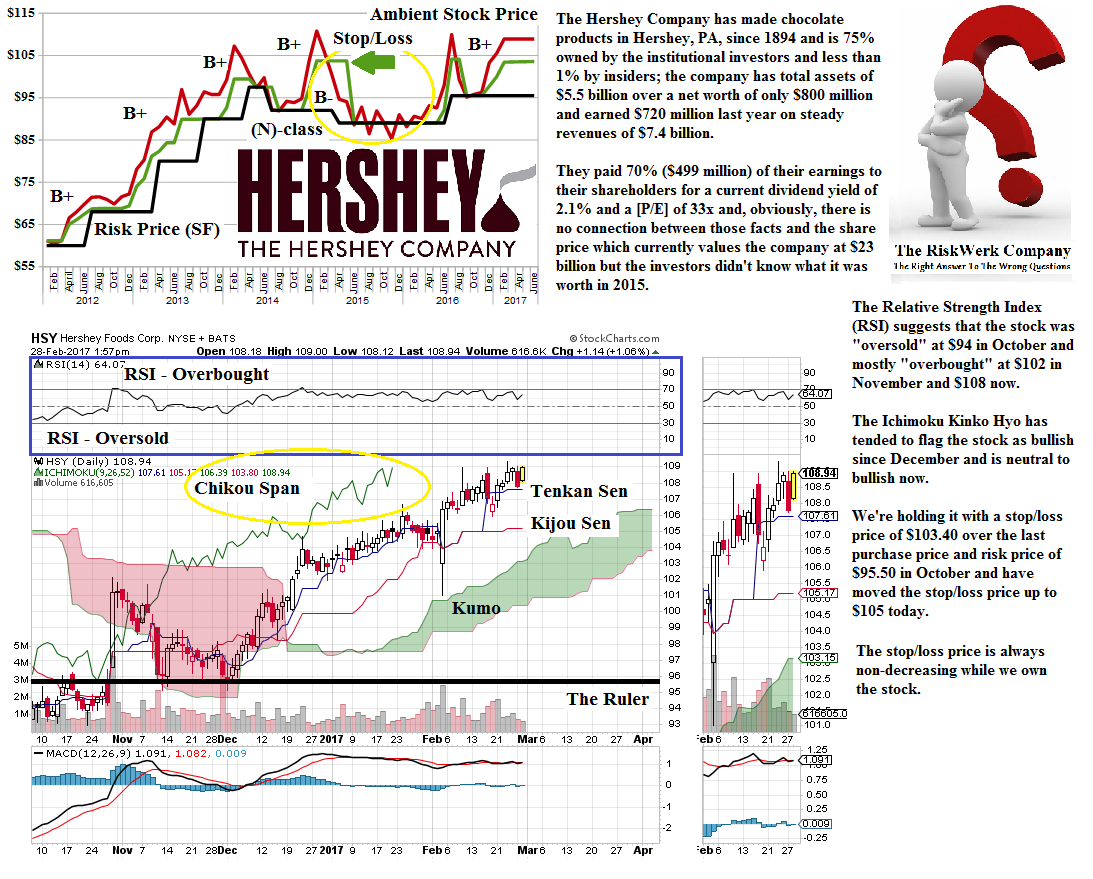

Figure 2.10: HSY Hershey Foods Corporation (B+) |

Figure 2.11: JACK Jack in the Box Incorporated (B-) |

Figure 2.12: K Kellogg Company (B+) |

Figure 2.13: KO Coca-Cola Company (B+) |

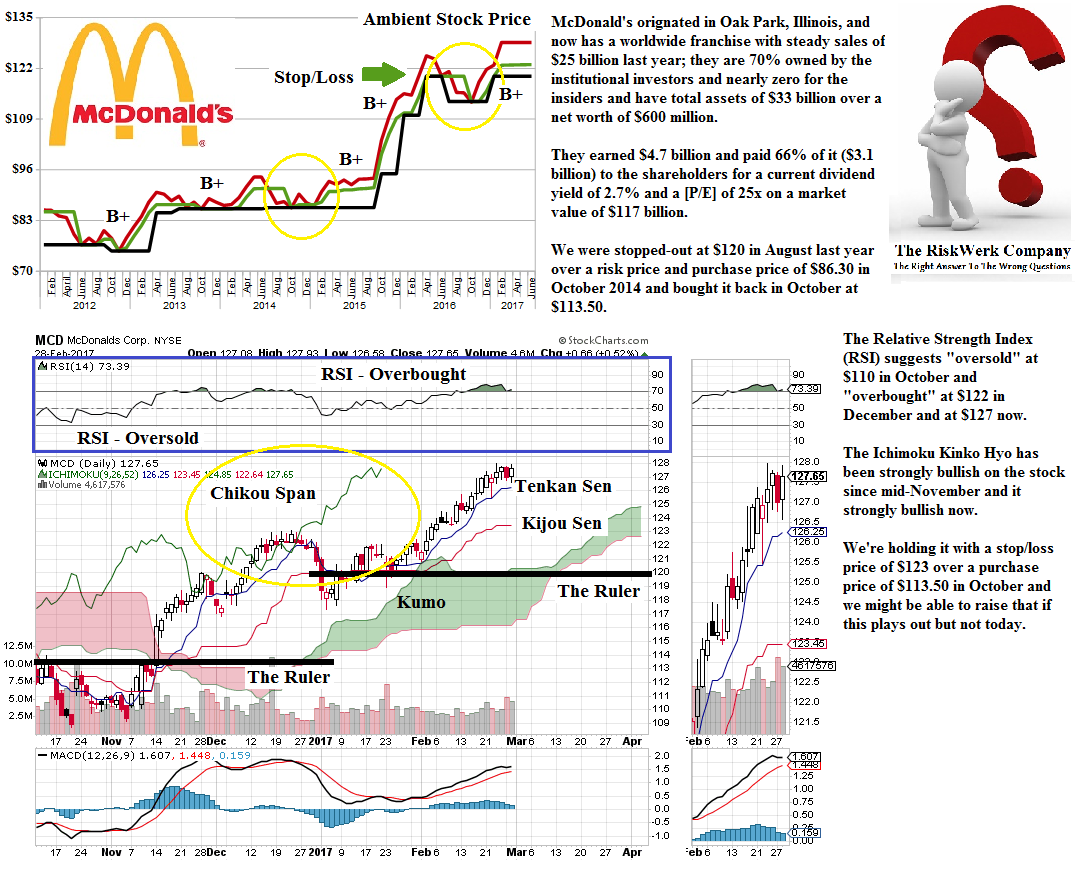

Figure 2.14: MCD McDonald’s Corporation (B+) |

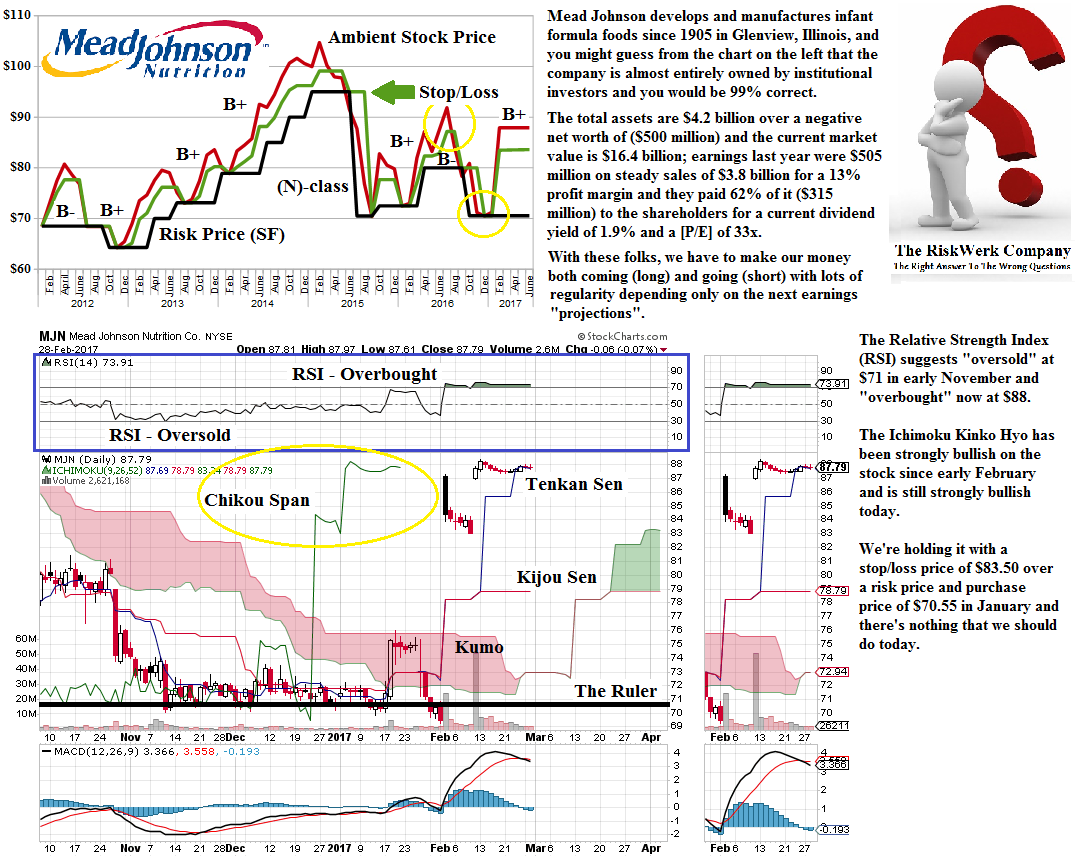

Figure 2.15: MJN Mead Johnston Nutrition Company (B+) |

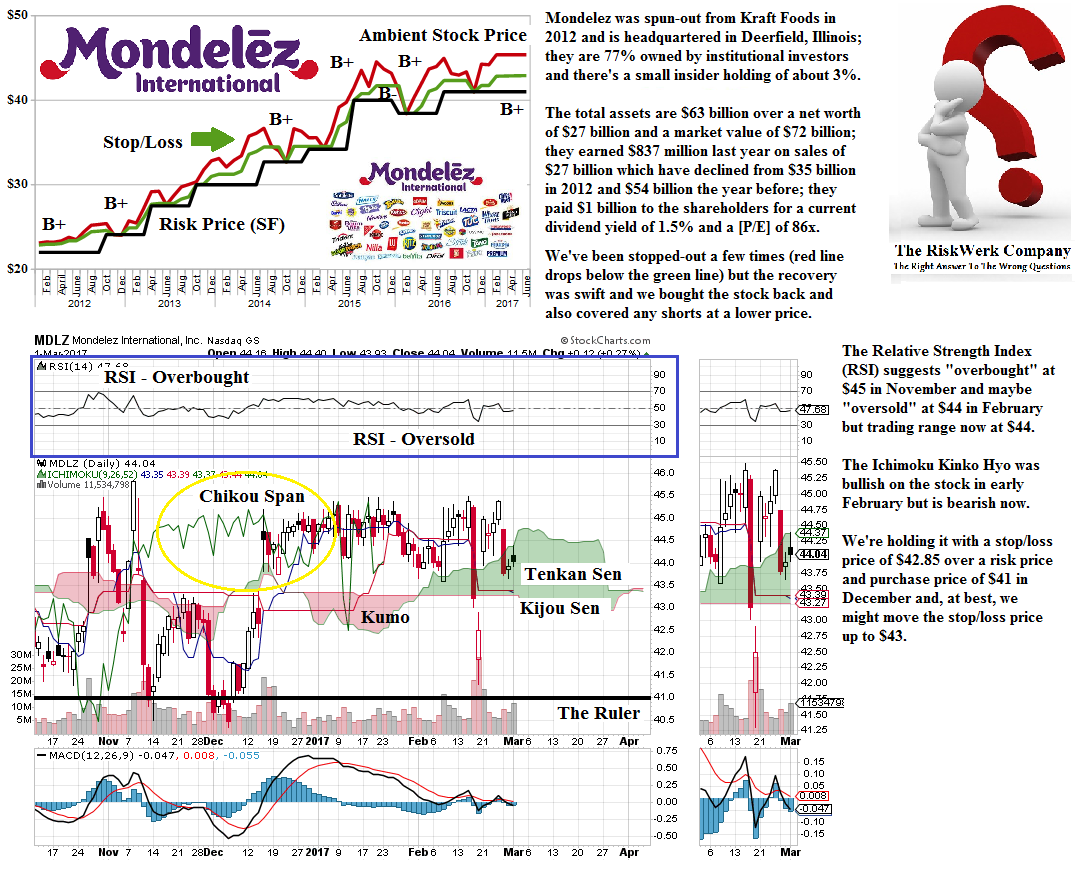

Figure 2.16: MDLZ Mondelez International Incorporated (B+) |

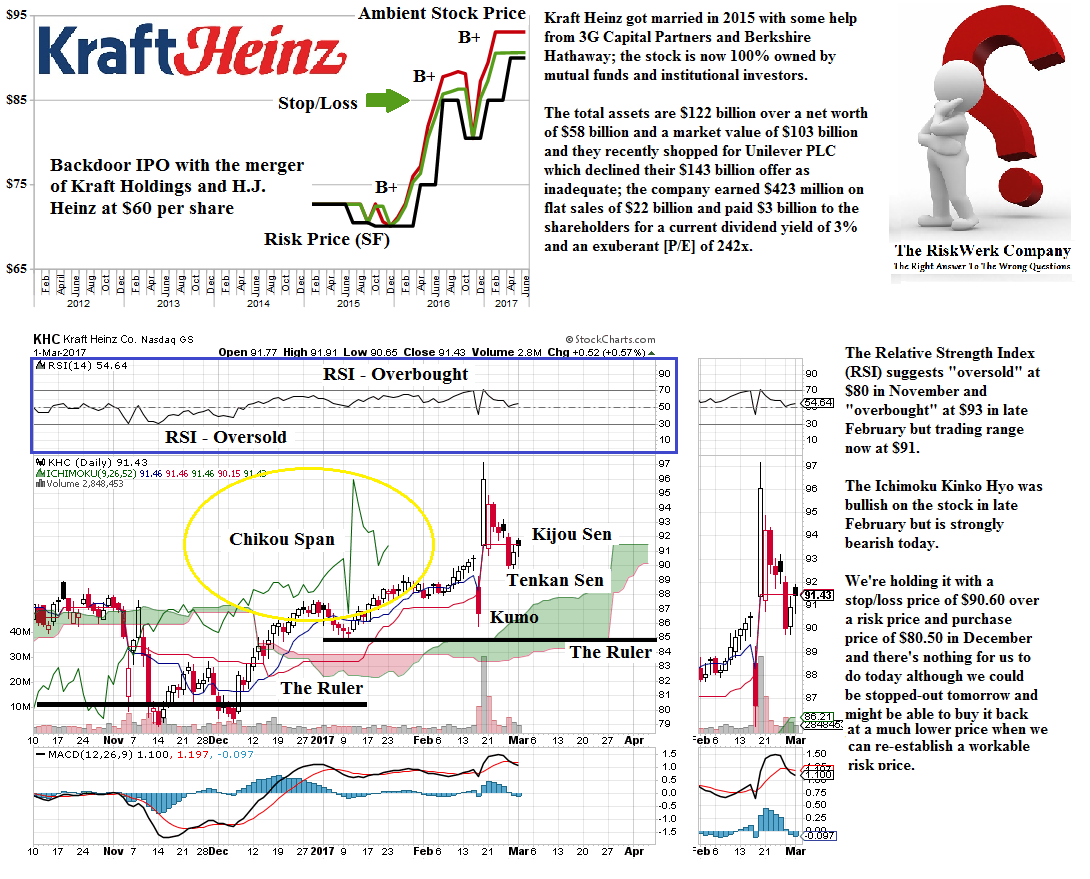

Figure 2.17: KHC The Kraft Heinz Company (B+) |

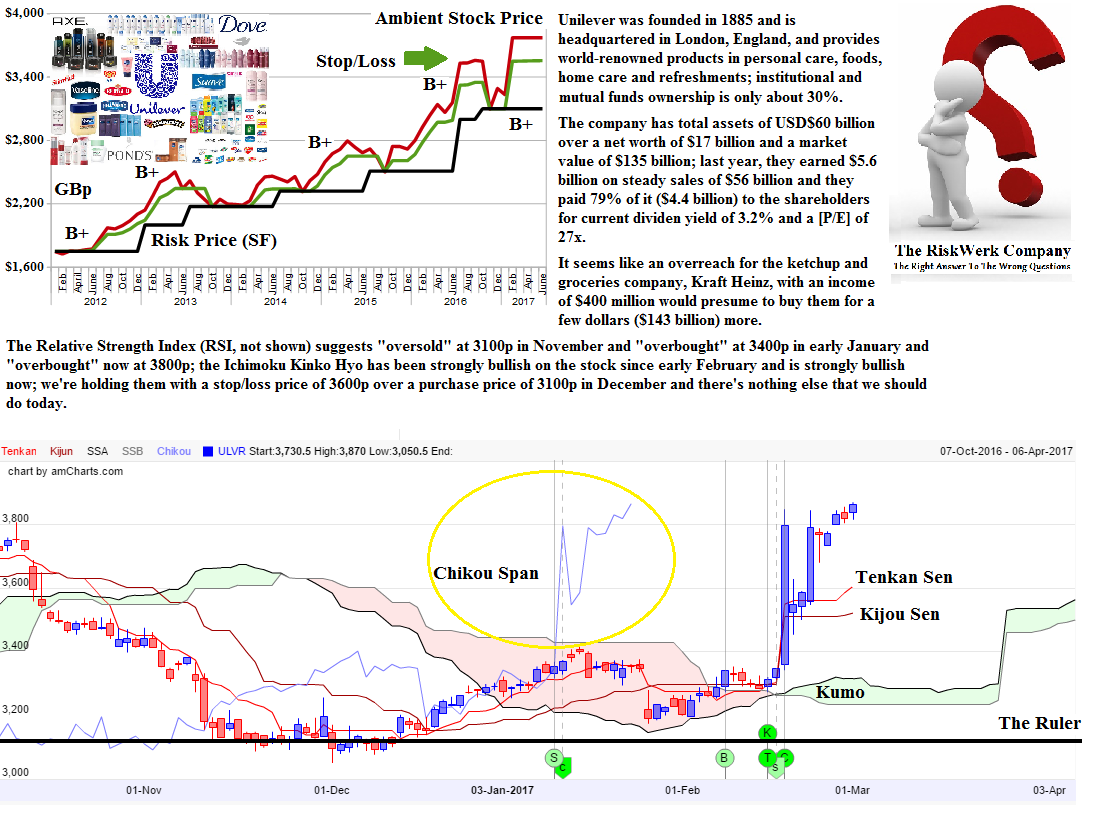

Figure 2.18: ULVR.L Unilever PLC (B+) |

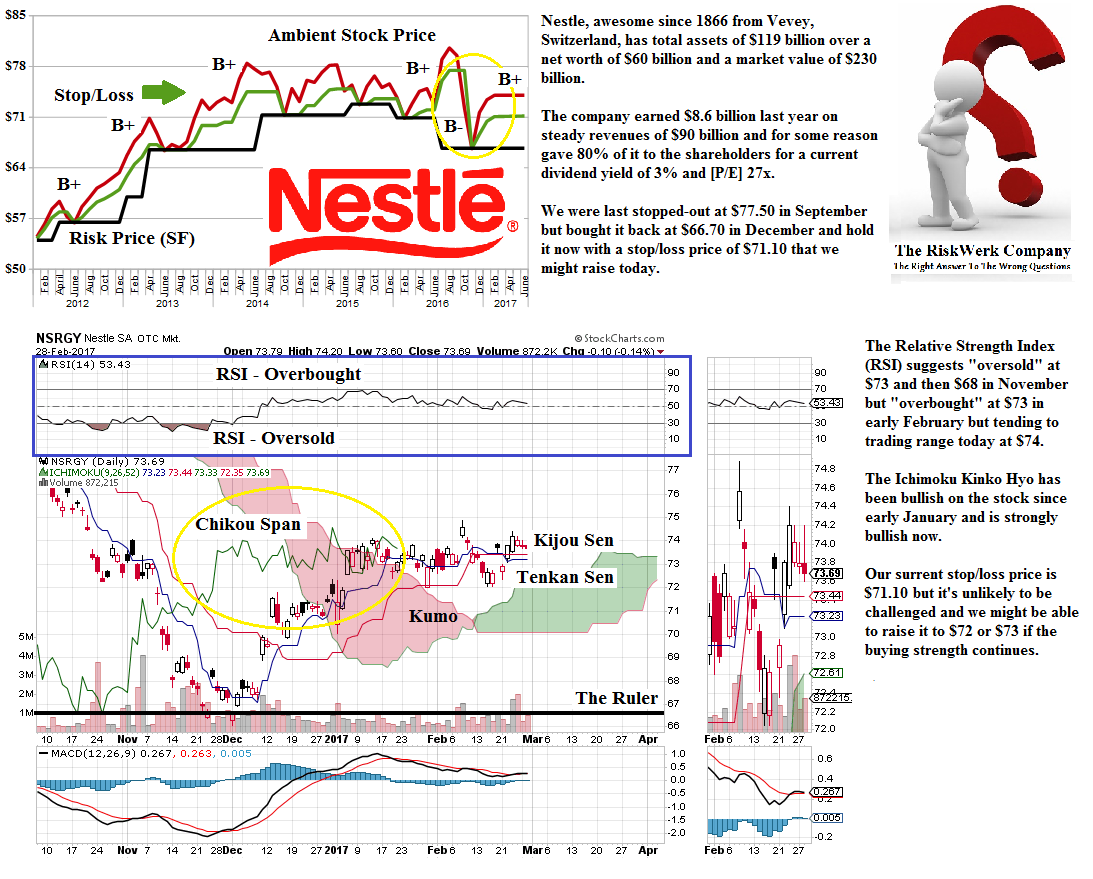

Figure 2.19: NSRGY Nestle SA ADR (B+) |

Figure 2.20: PEP PepsiCo Incorporated (B+) |

Figure 2.21: PLKI Popeyes Louisiana Kitchen Incorporated (B+) |

Figure 2.22: QSR Restaurant Brands International Incorporated (B+) |

Figure 2.23: RI.PA Pernod Ricard SA |

Figure 2.24: SHAK Shake Shack Incorporated (B+) |

Figure 2.25: SONC Sonic Corporation (B+) |

Figure 2.26: SYY Sysco Corporation (B+) |

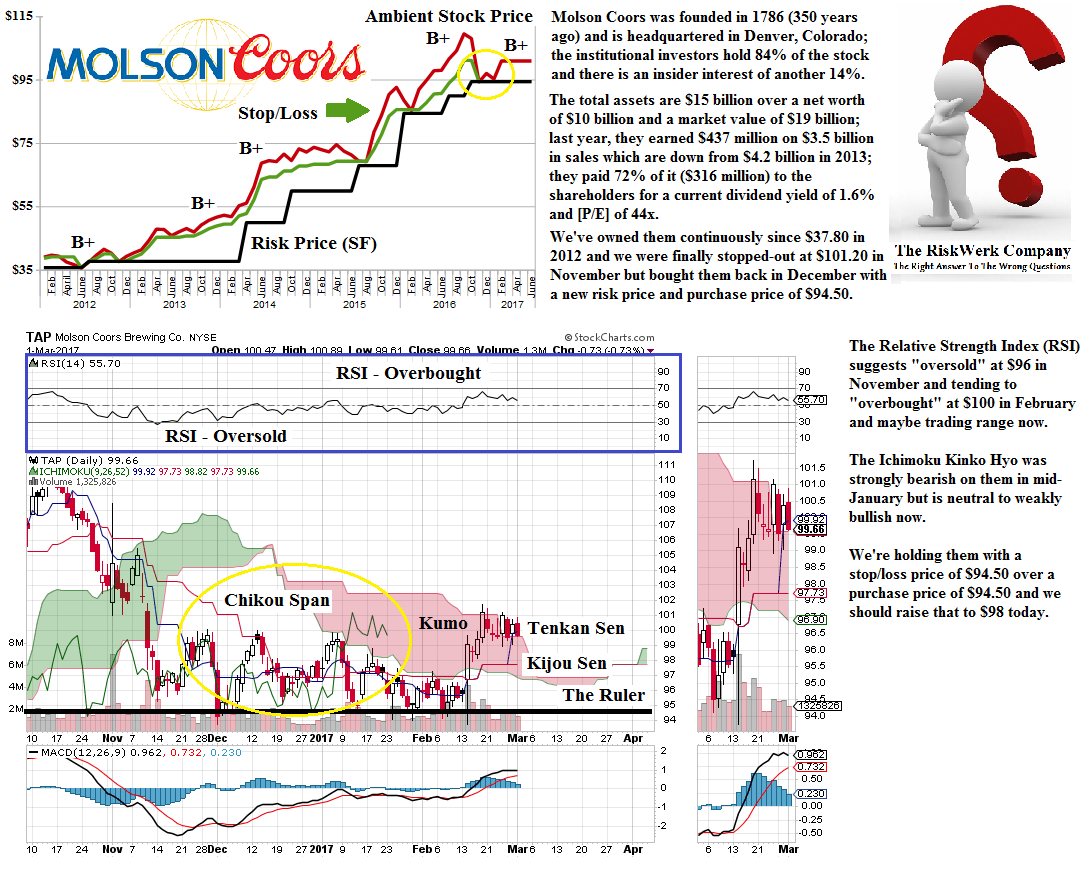

Figure 2.27: TAP Molson Coors Brewing Company Class B (B+) |

Figure 2.28: TSN Tyson Foods Incorporated Class A (B+) |

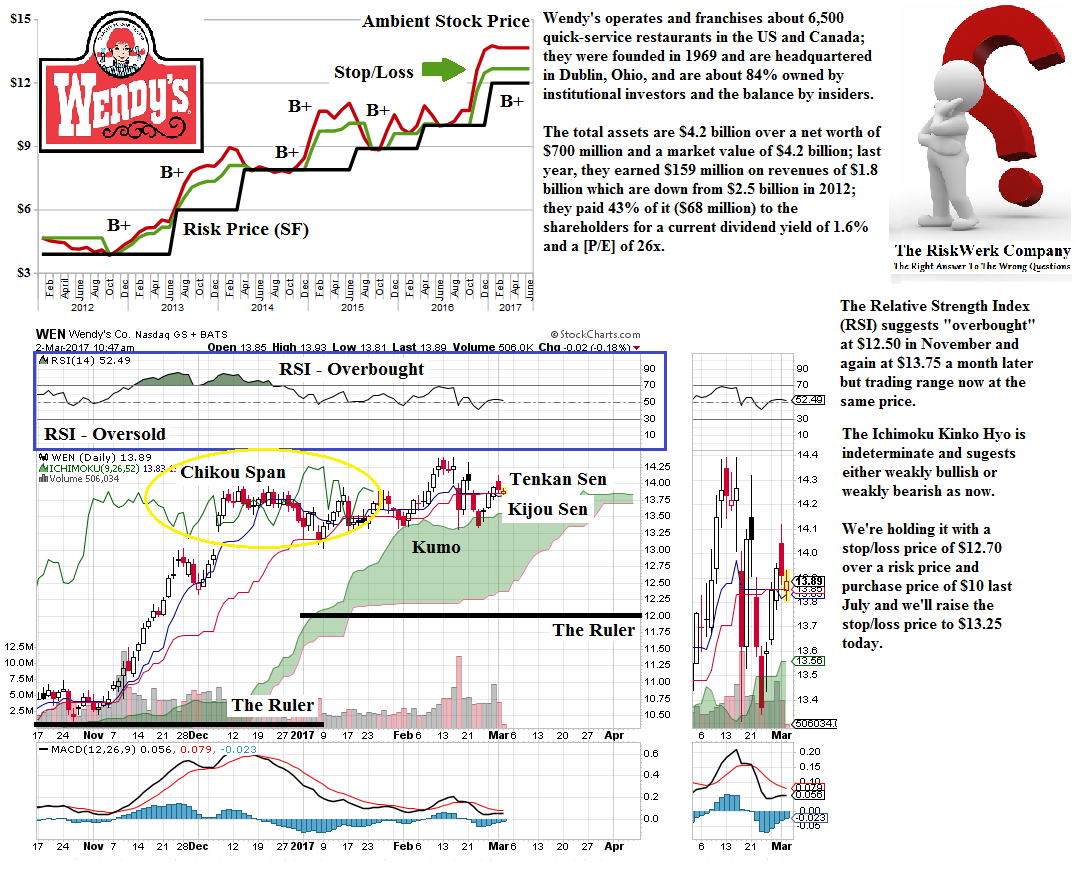

Figure 2.29: WEN The Wendy’s Company (B+) |

Figure 2.30: YUM Yum! Brands Incorporated (B+) |

For more examples of the (B)-class portfolio in difficult markets, please see our recent Posts on”The “W” Syndrome“, Steel, Green Energy, UFOs and the High Flying Techs, and The Coal War which is heating-up again now; and the Canadian Mines have also taken-off – please see our recent Post “(B)(N) Extreme Economics – The (New) Canadian Mines” for a heads-up on that as well as The Great Rotation & Twenty Hot Canadians 2017.

And for more information and examples of the Free Market Yield and the terms that we have used above, please see our Posts “(P&I) The Dismal Equation (Ecclesiastes 9:1)” and “(B)(N) S&P 100 Volatility Risk and The Full Moon” and “(B)(N) NASDAQ 100 Volatility and The Stone Bunnies“ and for an introduction to The Barometer “(B)(N) What’s A Girl To Do” or “(P&I) The Swiss Franc Debacle“.

And for more information on real “risk management” in modern times and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary and “(P&I) Dividend Risk and Dividend Yield“, and our recent Posts “(P&I) The Profit Box” and “(P&I) The Process – In The Beginning“; and we’ve also profiled hundreds of companies in these Posts and the Search Box (upper right) might help you to find what you’re looking for, such as “(B)(N) TLM Talisman Energy Incorporated” or “(B)(N) ATHN AthenaHealth Incorporated” or “(B)(N) PETM PetSmart Incorporated“, to name just a few.

And for more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice. And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

And for more on what risk averse investing has done for us this year, please see our recent Posts on “(P&I) The Easy (EC) Theory of the Capital Markets” or “(B)(N) The Easy (EC) Theory of the S&P 500“, and the past, The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”). The Canada Pension Bond®™, The Medina Bond®™, The Barometer®™, the Free Market Yield®™ and Extreme Economics®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.