(B)(N) Hola! Bola Mexico – Avocados & Auto Parts

Avocados & Auto Parts

Drama. We’re motivated to find “inflationary economies” because the expected return in the (B)-class portfolio in those markets is the dividend yield plus twice the normalized annual volatility of the market.

And we can get those returns and even more with no risk to our capital not because the companies are “special” or that we’re good “stock pickers” (we’re not) but we can do it because the investors are “special” (very special) and that’s a problem that they have and they haven’t learned to deal with it, if ever.

For example, the current dividend yield in the Dow Jones Industrial Companies is about 2.8% and down from higher averages of 3% to 3.5% in the last several years and the current normalized annual volatility is 7.2% so that we would expect (using the formula above) to get about 17% per year in capital gains and dividends by running the (B)-class portfolio in that market – and we do; please see Exhibit 1 below for more details.

But that’s an interesting number – 17% per year, year after year – on our money invested in America’s biggest companies and safer by far than US government bonds which are subject to inflation even as these governments have been trying to “create” inflationary economies and failing to do so when the “inflationary economies” that they’re looking for are right in front of them in the enterprise of their people.

And they can’t pay their social security or pension and medicare benefits, for example, from investment earnings but they have to reach into our pockets for more taxes or more donations for dwindling services (Reuters, October 7, 2016, Share more or face stagnation, ECB tells euro zone countries and P&I, October 16, 2016, Most funds feel dreaded pinch of negative returns).

To get to the “interesting number” takes a little bit of work, but we’re convinced that anybody can do it with just a “stock chart, a ruler, and a good eye” and some money to invest; if you’ve been reading our Posts, you already know that and can just skip to Exhibit 2 and take a well-earned vacation in Mexico or buy all the avocados and auto parts that you might need for your store or plant.

Inflation & Deflation

As another example of inflation, the Brazilian economy is wildly CPI inflationary but the IBRX 50 gave us 26% per year (and our new boots) in the Brazilian reais and the current dividend yield is about 2.7% and the normalized market volatility is 10.3% per year so we might expect +23% per year as a normal return in that market.

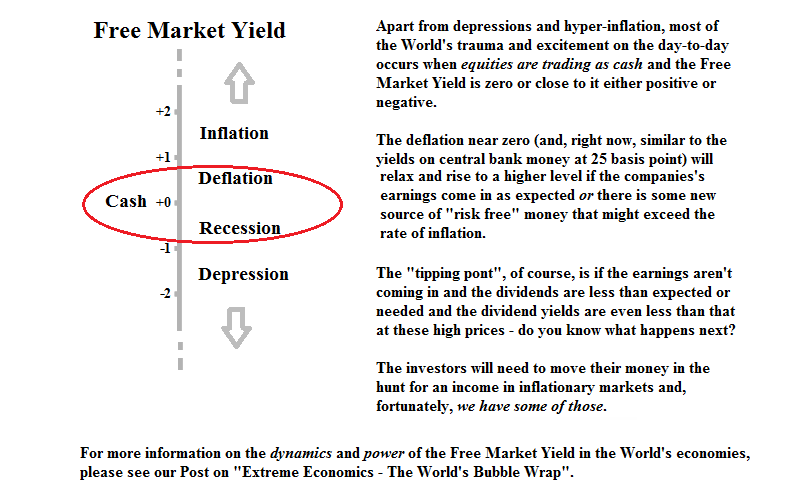

The fundamentals are not difficult but economists only measure CPI (consumer) and PPI (producer) price inflation compared to months ago, and even years ago, and they call that “inflation” but those are only the symptoms of inflation and they are not the causes of inflationary and deflationary economies, including recessions and depressions and hyperinflation.

An “inflationary economy” is one in which the “price of an income” is low and a “deflationary economy” is one in which the “price of an income” is high, and in both cases, we can measure that now by using the currency as our benchmark for what income money can buy.

Figure 1: Inflation & Deflation

For example, if the government wants to pay, or has to pay us 20% per year to borrow our money in its government bonds to pay its bills, that’s an “inflationary economy” because the “price of an income” is just our cash which “earns” 20% invested in government bonds but our money and income will soon be as worthless as the “Jefferson Dollar” in that scenario and that’s exactly what happened in Brazil in the last five years; please see Figure 1 on the right for an overview of the theory and type “inflation” in the Search box for more examples.

Our problem today is that the US and European economies are “deflationary economies” and the “price of income” is high in high-priced stocks and low-yielding bonds.

And we’re also reasonably expecting that the Dow is going to die (please see Exhibit 1 below) and the drums are already beating for it but we don’t know when it will die or when it will have some new convulsion such as the “W-Syndrome” of last year (Bloomberg, October 7, 2016, Goldman Sachs’s Cohn Calls Central Banks an ‘Ineffective Cartel’ and CNBC, October 13, 2016, Here’s what could pop the stock-market bubble).

Hola! Bola Mexico

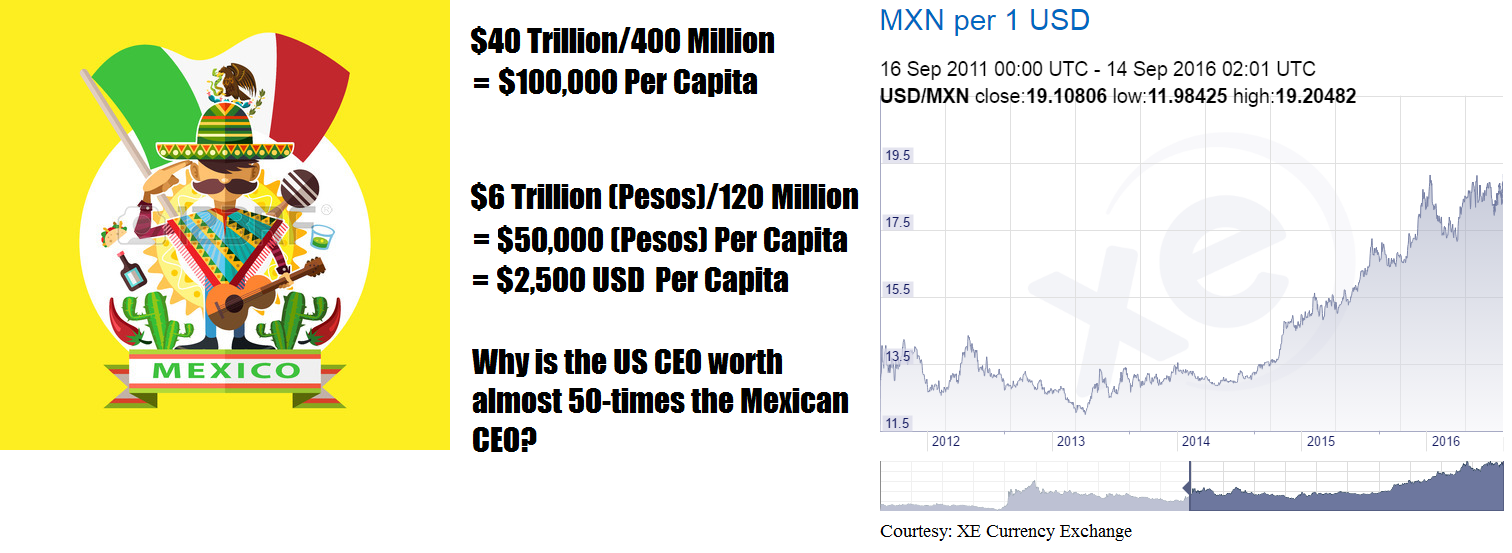

The North American stock markets in New York and Toronto are worth about $40 trillion right now which is more than 100-times the worth of the Mexican Bolsa in Mexico City (about $6 trillion pesos at twenty pesos to the dollar); why then should we care to invest there?

Only Two Cents, You Say?

The problem is that there are only about 400 million people in Canada and the US and 120 million people in Mexico, so by what fantasy do our stock markets maintain a nearly 50-fold difference per capita in the “worth” of our companies and their stocks?

Moreover, the Mexican peso (MXN) traded at about 10 pesos to the dollar a decade ago and so the peso has become a lot cheaper in US dollars, but the peso has not changed that much in terms of how it affects the people and their spending power with a targeted inflation rate of about 3% per year and GDP growth in constant dollars or per capita that is similar to the US and the US dollar has become vastly overvalued and “high priced” as above in the hunt for an “income” on it.

Will you be taking dollars or pesos today, sir?

Both, thank you, because we know that the US dollar has a lot of air in it and there are a lot of countries with a lot of people who are catching up to us fast and we can only defend the dollar (short of bombing them) by buying theirs because they don’t need to buy ours at these high prices and they can do a lot more on their own, just as we did fifty years ago and China is doing now (TheStreet, October 24, 2016, Germany Faces Tough Choices As China Funds Target Tech Sector).

Figure 2: The Dead Dow

And, of course, we don’t know when the North American CEO who claims to be worth more than 50-times the average Mexican CEO is going to be fired, but it’s happening now and in process and the Dow is slowing down with or against the other major World markets; please see Figure 2 on the right.

Nor is the Dow exactly “dead” but most of the World cannot afford to buy its iconic products and churning new versions among those who can is not a strong growth proposition.

And the Dow is currently “overvalued” as more money is pouring into it on declining revenues, declining earnings, and dividend yields maintained at 2% to 3%, on average, by increasing the payout rates to above 60% of the earnings; please see Exhibit 1 below for more details.

The Perpetual Bond

We call the full market (B)-class portfolio “The Perpetual Bond” because it reflects the economy of a country and it works like a capital-safe government bond on risk (inflation or currency exchange is the only exposure) and that’s a game changer because the heuristic is guaranteed to work in any market.

For example, if we’re buying avocados and auto parts in Mexico, then we have a chance to participate in that economy and earn our pesos there and not just buy them forward; please see Exhibit 2 below for an example of how that works.

We could also take still larger markets to our advantage and it’s only notional that the Dow Jones Industrial Companies and the BMV Bolsa Mexico are sufficiently representative of their “entrenched” industrial and financial economies.

However, our investment returns in the Dow and the BMV Bolsa Mexico are already very similar at about 16% (or more) per year in the Dow in dividends and capital gains in dollars and 18% (or more) per year in the Bolsa in pesos (about twenty pesos to the dollar) and our indifference to these markets can be explained not by culture or productivity but by the market factors which are due to the investors (the “special” investors, as above) and how much money they have to invest and when they will need it in cash to pay their bills and those imperatives are the same everywhere; please see Exhibit 1 and 2 below for more details (and click on them to make them larger as required).

Exhibit 1: The Dead Dow – Fundamentals & Cash Flow Summary

Exhibit 2: Hola! Bola Mexico – Fundamentals & Cash Flow Summary

For more examples of the (B)-class portfolio in difficult markets, please see our recent Posts on”The “W” Syndrome“, Steel, Green Energy and The Coal War which is heating-up again now; and the Canadian Mines have also taken-off – please see our recent Post “(B)(N) Extreme Economics – The (New) Canadian Mines” for a heads-up on that.

And for more information and examples of the Free Market Yieldand the terms that we have used above, please see our Posts “(P&I) The Dismal Equation (Ecclesiastes 9:1)” and “(B)(N) S&P 100 Volatility Risk and The Full Moon” and “(B)(N) NASDAQ 100 Volatility and The Stone Bunnies“ and for an introduction to The Barometer “(B)(N) What’s A Girl To Do” or “(P&I) The Swiss Franc Debacle“.

And for more information on real “risk management” in modern times and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary and “(P&I) Dividend Risk and Dividend Yield“, and our recent Posts “(P&I) The Profit Box” and “(P&I) The Process – In The Beginning“; and we’ve also profiled hundreds of companies in these Posts and the Search Box (upper right) might help you to find what you’re looking for, such as “(B)(N) TLM Talisman Energy Incorporated” or “(B)(N) ATHN AthenaHealth Incorporated” or “(B)(N) PETM PetSmart Incorporated“, to name just a few.

And for more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice. And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

And for more on what risk averse investing has done for us this year, please see our recent Posts on “(P&I) The Easy (EC) Theory of the Capital Markets” or “(B)(N) The Easy (EC) Theory of the S&P 500“, and the past, The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”). The Canada Pension Bond®™, The Medina Bond®™, The Barometer®™, the Free Market Yield®™ and Extreme Economics®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.