(P&I) Extreme Economics – Brazil IBRX 50

Figure 1: The RiskWerk Primer on Inflation and Deflation

Drama. The US government isn’t going to give us any more money for borrowing our US dollar this year but that’s not the preference of the entrenched wealth which always wants more rent for their money and they’re now wondering when they’re going to get paid but the future is cloudy, very cloudy (NYT, September 17, 2015, Fed Leaves Interest Rates Unchanged).

But Brazil will give us more money for our money, if that’s any help, and they have import bills to pay and foreign debt to pay and 200 million people to feed every day.

And the Brazilian economy is in a recession, maybe a depression (Canada take note) and it’s wildly inflationary with respect to the US dollar (please see Figure 1 on the right above and click on it and again to make it larger as required) but as shareholders in Brazilian companies all we really need to worry about (please see below) is that our companies don’t go bankrupt while we own their stock.

Of course, we might wonder how we can have an inflationary economy in a depression (please see below) and it’s hard (or accidental) to make a quick buck on capital gains because our money is evaporating as soon as we buy the stock and we certainly don’t want to have a liquidity problem too soon if we’re borrowing money to buy or leverage our stocks on margin in a depression while we’re also paying double-digit rates on our debt.

And we’re also converting our US dollars into Brazilian Reals (BRL) and we’re potentially borrowing Brazilian Reals (or reais) on margin as well and we need to wonder what it’s going to cost us in investment returns to pay our bills in US dollars.

We’ve therefore set ourselves the difficult problem of discovering how to earn an income in a depression by buying and holding or selling the stocks of the companies involved.

Figure 2: Axis of Power and the Trans-Pacific Partnership

And just to be clear, the economy that we’re talking about in the depression is a portfolio of stocks and it includes all of the companies that are in the portfolio, all of the investors who have an interest in those stocks, and how much money they have to invest in reals and dealing with the exchange rate problem is a different problem but it pivots on our ability to earn an income in a depression.

Of course, we can take all of the stocks in the World if we want to but in almost any portfolio we can find a depression, a recession, deflation, and inflation (please see Figure 1 above) and we need to know how to deal with all of that and earn an income in any of that because the good times don’t always roll and the World is now shifting from an East-West axis between Europe and North America (which took a few hundred years to develop) to a Middle East – Russia – China axis with India in the middle and Southeast Asia below it and a re-arming Japan on the Far East and a Trans-Pacific Partnership (TPP) that reaches all the way to Central America.

Oh oh – should we bomb them?

But war is the usual solution to inflation (wars cost money and they’re risky, very risky) and there’s scant reason for inflation and easy money to return to the US or Europe because technology is replacing jobs in middle management so that all we have are the executive cadre, the sales people, the technology gurus of all sorts and the automated production process, and the box-packers but we need to take care of all of them because we need consumers as well as producers to support our growth.

Brazil IBRX 50

Exhibit 1: (B)(N) Brazil IBRX 50 – Risk Price Chart

Figure 1.1: (B)(N) Brazil IBRX 50 – Risk Price Chart

The Sao Paulo IBRX 50 lost 30% of its value in USD this year and 50% since last year and it has a Free Market Yield of 2.276% which is comparable to Taiwan (2.264% with only half the volatility) and a dividend yield of 4% to 5% at the current prices and a payout rate of 80% and an annual demonstrated volatility of 48%.

How are we supposed to make money in this?

The Depression

It’s undoubtedly true that we can make money in a rising market or a merely volatile one and there are always lots of those but there is no market that rises forever and few that rise for more than a few years until the fundamentals in earnings and dividends can catch-up to the prices that investors have paid for them.

But a depression always results in a wealth transfer from investors (and many other people in terms of their savings and houses or properties, for example) who can’t earn an income and have to sell their assets at low prices (or work for low wages) to pay their bills and make pension payments (and buy food and pay the rent, so to speak) to the others, those who have money (and wealth) and don’t have a liquidity problem and can afford to buy those assets at low prices if and when they want to.

But if they don’t buy them and don’t pay wages and the people can’t eat, then they can expect a revolution and a change of government and when they do buy them, then they have the problem of obtaining an income from what they bought and that’s the beginning of a recovery and an inflationary but growth economy.

Brazil is expected to have a decline in its GDP of about 2.7% this year (which is horrendous but the causes are well understood) and that’s down from a previous forecast of 1.1% and the trade deficit is growing as is the fiscal deficit (Barron’s, September 24, 2015, Brazil’s Economy: No Speedy Recovery) and the government has said that it will ” use any weapon at their disposal to calm the exchange rate market”.

How are they going to do that?

Figure 3: Brazil CPI Inflation Since 1980

There aren’t any weapons if the government has to print money to pay its bills. One of the problems is that the government is charging (only) 6% (and it has been thinking about raising it ibid Barron’s) for the overnight regulatory money but the banks are lending it out at 20% or more to consumers and how is the government going to lower that rate if it can’t pay its own bills without that income?

And, obviously, it pays to be in debt in an inflation (currently CPI 9%) or hyperinflation if we can repay our debt in relatively worthless reals and the Brazilians who can are “living it up” on the day-to-day by necessity – what choice do they have – but when will the lights go out? And how will that happen?

Although the banks are profiting from this situation, an influx of new money in reals or an influx of new money in US dollars or a foreign currency to buy the “cheap” reals and pay-off or pay down the debts will leave them sitting with a lot of cheap cash on their balance sheets.

What Brazil needs to do is recover (please Figure 1 above) the productivity of its industry and increase the quality and quantity of its exports and source and increase the import of cheaper goods for the consumers or produce them at home; the depression will “solve” some of those problems as people lose their jobs and can’t afford to buy things at premium prices and lose their loans and their houses and maybe their families.

What Brazil needs to do is recover (please Figure 1 above) the productivity of its industry and increase the quality and quantity of its exports and source and increase the import of cheaper goods for the consumers or produce them at home; the depression will “solve” some of those problems as people lose their jobs and can’t afford to buy things at premium prices and lose their loans and their houses and maybe their families.

We didn’t have a problem pulling +100% out of this market and doubling our money since 2012 but now we’re sitting on a lot of reals and we only own three of the companies in the (B)-class portfolio and our reals are worth 50% less than they were in 2012 – but we can buy more of the stocks at any time and collect our dividends and wait while Brazil figures out how to feed its 200 million people; the assets are selling at 1/5th of their balance sheet value and the market value is no more than the net worth.

Exhibit 2: (B)(N) Brazil IBRX 50 – How are we supposed to make money in this?

Figure 2.1: (B)(N) Brazil IBRX 50 – How are we supposed to make money in this?

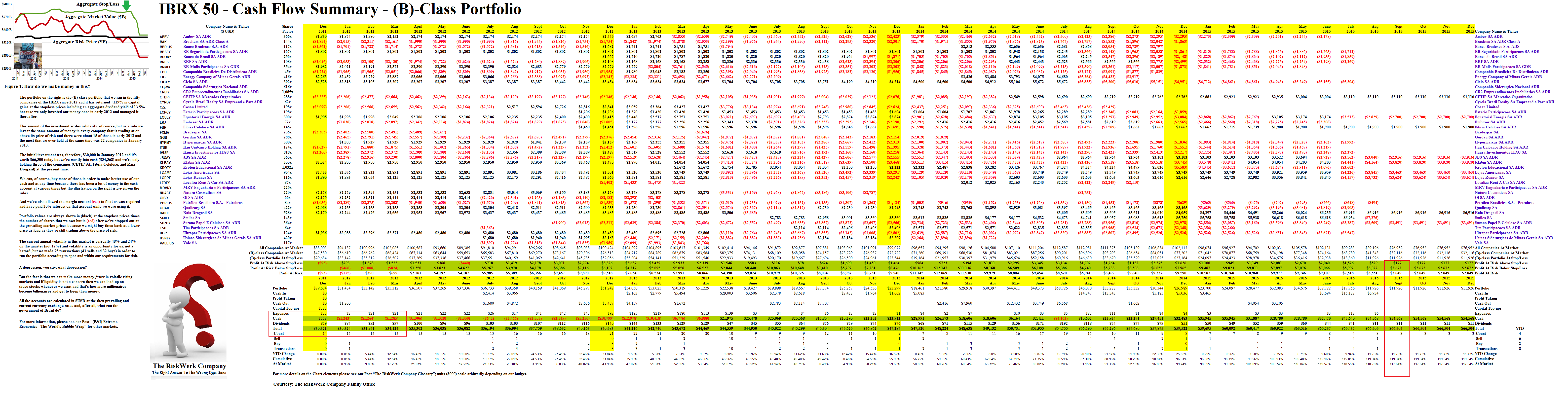

Exhibit 3: (B)(N) Brazil IBRX 50 (B)-class Portfolio Cash Flow Summary

Figure 3.1: (B)(N) Brazil IBRX 50 – How do we make money in this – Cash Flow Summary

For more information and examples of the Free Market Yield and the terms that we have used above, please see our Posts “(P&I) The Dismal Equation (Ecclesiastes 9:1)” and “(B)(N) S&P 100 Volatility Risk and The Full Moon” and “(B)(N) NASDAQ 100 Volatility and The Stone Bunnies“ and for an introduction to The Barometer “(B)(N) What’s A Girl To Do” or “(P&I) The Swiss Franc Debacle“.

And for more information on real “risk management” in modern times and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary and “(P&I) Dividend Risk and Dividend Yield“, and our recent Posts “(P&I) The Profit Box” and “(P&I) The Process – In The Beginning“; and we’ve also profiled hundreds of companies in these Posts and the Search Box (upper right) might help you to find what you’re looking for, such as “(B)(N) TLM Talisman Energy Incorporated” or “(B)(N) ATHN AthenaHealth Incorporated” or “(B)(N) PETM PetSmart Incorporated“, to name just a few.

And for more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice. And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

And for more on what risk averse investing has done for us this year, please see our recent Posts on “(P&I) The Easy (EC) Theory of the Capital Markets” or “(B)(N) The Easy (EC) Theory of the S&P 500“, and the past, The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”). The Canada Pension Bond®™, The Medina Bond®™, The Barometer®™, the Free Market Yield®™ and Extreme Economics®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.