(P&I) World Trade & Trade Productivity

Welcome to the Netherworld!

Drama. An enterprise can grow “horizontally” by acquiring or “absorbing” its competitors, and “vertically” by acquiring its “suppliers” (upstream) and possibly its customers (downstream) who are held in its “thrall” or necessity, so that it could end up “producing by itself for itself”, which is the “goal” and signature of a sovereign state (The Daily Mail, October 13, 2014, The iPhone ruined my country’s economy: Finnish prime minister).

A government which is a sovereign state – not to consider corporations – fails to be the “One World” (producing by itself for itself) as long as it has “suppliers” and, therefore, payables (P); or if it has “customers” for which it has receivables (R), and we describe them both as (P) “what the government (sovereign state) owes” and (R) “what is owed to the government” outside of itself.

Inside of itself, however, where it is expected to govern, it will tend to have the Company D modality (please see below), and it will always be in debt to its people, but it cannot be insolvent, or bankrupt, inside of itself (no matter how bad the situation is for its people) and it has only to deal with the payables outside of itself, and those are acquired and dealt with in trade with other sovereign states.

If a government has only payables, and no or negligible receivables, then we would expect that it would eventually disappear, having “paid itself out”; and if it has only receivables, then its customers will have only payables and they too must eventually “pay themselves out” and disappear.

And in either case, we are left with an “entity” that has no relations outside of itself, neither payables nor receivables that would be due to something outside of itself, and the question is, can such an entity exist? And if not, why not; and if it can, what does it look like?

Buzludzha, Bulgaria – it was a Congress of sorts and cost millions, of lives.

But it’s not a hard question to answer because we already know the answer – we have just the “One World”, our world, and it exists as such because, and only because, we have “Global Trade” and countries that can not compete, or will not compete, or are excluded in global trade, will always wither and die at great expense to its people.

The Non-entity Entity

The state of payables that are vastly in excess of receivables is entirely described by its modality, α=R/P, that is as close to zero as it might be, but for which many of its properties begin to emerge at α<1/e=0.368… which is the Company D modality which we call the “Death Embrace” (please see below), and it is a “low entropy” state – death by freezing, so to speak, and inhabited by the “economically frozen”.

As a less mordant example, the Canadian REITS are all of extraordinarily low entropy (which is the modality) and typify the “kindness” – we let them (our customers) live – but “unkind” economics of “servitude” (to “rent”, in this case) in that region of vastly more payables than receivables.

Having said that, of course, the Canadian REITS are an attractive investment to those who own them (and don’t have to live in them) and a substantial benefit to the bondholders, so that, in fact, there is trade and the REITS are in the business of constantly maintaining and renewing their assets while taking rents as income, which is not unlike what governments do.

Moreover, it is not just low modalities that are a “problem” for both the payers and the payees; for example, the Microsoft Corporation has a modality of α=2.28, and Apple Incorporated, α=2.17, and entire industries have sprung-up to compete with them for their markets, and with just cause and opportunity, because both of these companies provide “defective or deficient products” for which their customers (the payers) have little defense but to go elsewhere.

If it has only receivables and negligible payables, then the entropy becomes high and its properties already begin to emerge if α>e = 2.71828… and those are the properties of the dreaded “heat death” at the end of time, which could arrive a lot sooner if we just make everything look the same, and lots of people have tried to do that with this “ism” or that “ism”, and that world is inhabited by those who have no use for “economics” while they still have the means, and we are used to frantic investors looking for income.

The One World

But we don’t have either of these “One Worlds” today, and we have never had them for long, but there have always been camps on both sides of it, some armed only with “swords”, others armed only with “pens”, and a few that have both but will surely lose both if they pursue the “One World” with their swords, and then with their pens which come-up empty, as affected the Romans, and the Babylonians before them, and the Persians after them, and every “empire” that we have ever seen.

Trade And “Tradism”

The Entropy Law has come to be understood as an “iron law” – with it, we exist, without it, we don’t – and that understanding has only emerged in the last hundred years or so, and there are still lots of physicists and philosophers who are still trying to “explain it” and the physical evidence suggests that it probably does not exist exactly as such at extremely low, very near zero temperatures where there is “no motion” or “time” or even “space”, and extremely high temperatures, vastly exceeding that of the sun, where there is no rest and it is state that describes the timeless universe before the advent of time, space, and entropy; please see The Process for more information on that equation, which is an equation of hope because it explains how any “zero” may become a “one” (ibid, The Daily Mail).

We have shown in the Theory of the Firm that companies form, and governments live, within “the societal standards of risk aversion and bargaining practice”, whatever those might be, at the Company D modality, and that the “currency” also forms at that modality as a consequence of the emergence of trade; please see our Post “(P&I) The Process – The 1st Real Dollar” for more details.

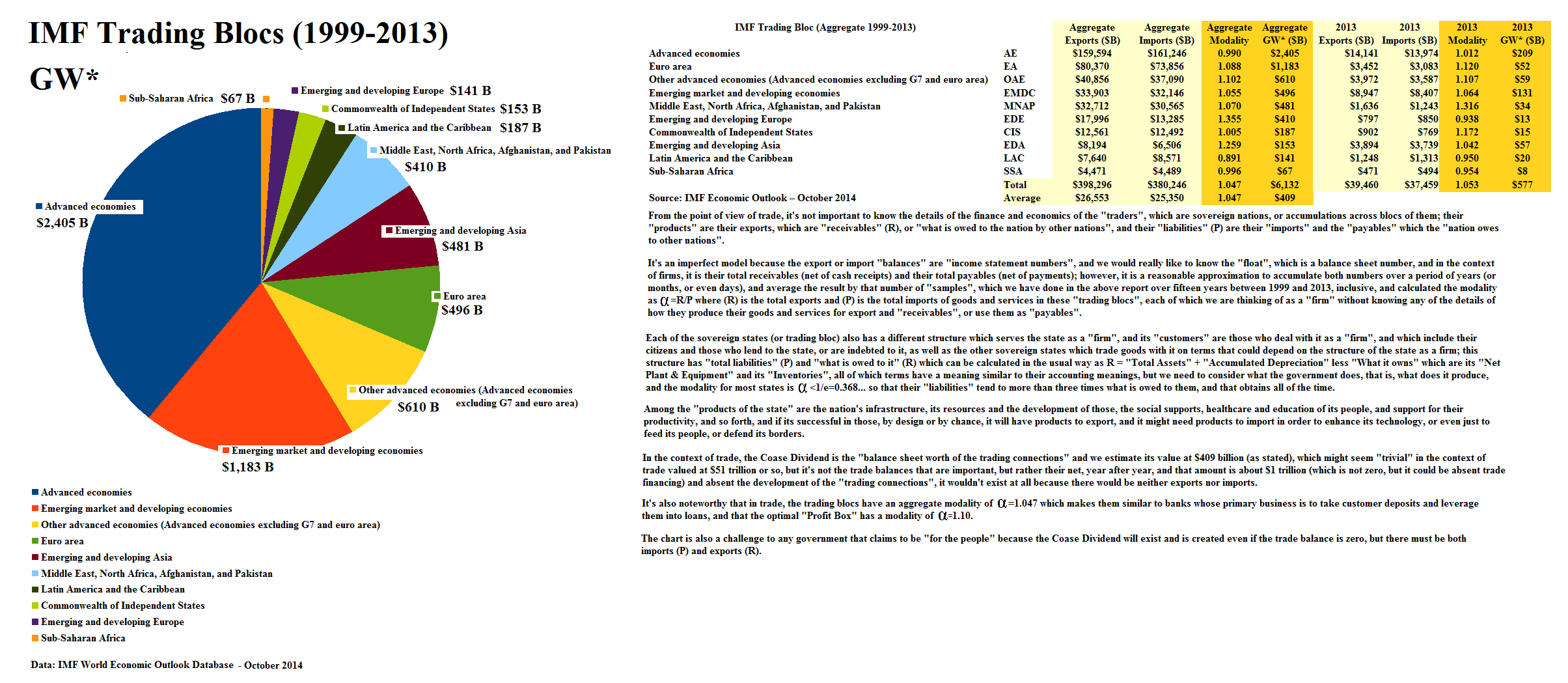

However, the trading blocs that we have today don’t operate at that level – they are not hand to mouth – but are much closer to the Company E modality at α=1, which is the “bank modality” and suggests competition for “deposits” and the income on them, and the evidence suggests that α≈1.10 which is optimal for the “Profit Box” and provides a small, but systemic, excess of receivables (exports) over payables (imports) which is the “profit” of the trade for those who are successful at it; please see Figure 1.1 below.

Exhibit 1: IMF World Trade in Major Blocs

Figure 1.1: IMF Trading Blocs World Economic Outlook Data

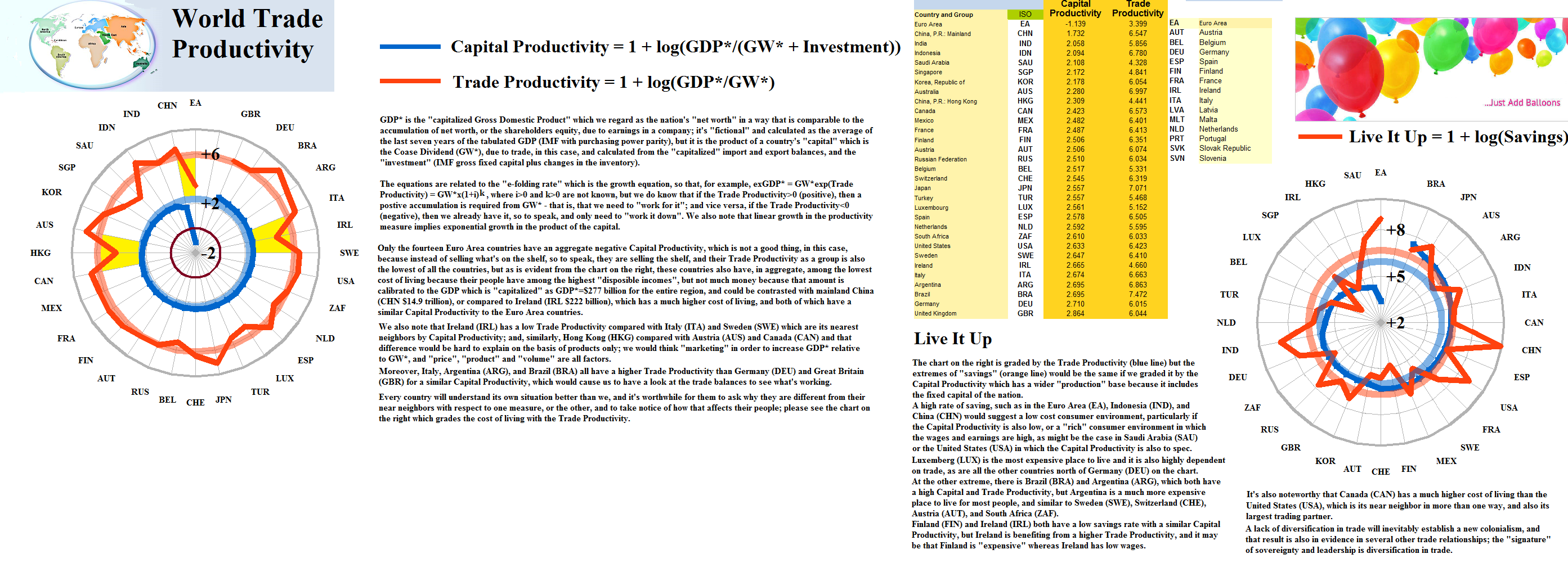

World Trade Productivity & The Best Places to Live It Up

In Figure 1.1 above, we have shown that the Coase Dividend which is the “balance sheet worth of the trading connections” is a rather large number – for these trading blocs, it’s $577 billion on a current and enduring basis, against a current net trade balance of about $2 trillion, or 28%, and even 34% if it is accumulated over a longer period of time, which it does because it’s a balance sheet number and an asset to the nation simply because it has trade.

If we add the Coase Dividend to the country’s “Total Investment” (as defined by the IMF World Economic Outlook Database) which is representative of the country’s “total capital formation” including the fixed assets at cost and the inventories, then we have an estimate of N* which is defined for firms as N* = GW* + “Fixed Assets (at cost)” + “Inventory” where the fixed assets and inventory are usually similar to the accounting definitions if we allow for their purpose which is to support the “production” of the “firm” and in this case, it is the “production” of receivables (exports) and payables (imports) in trade.

It’s natural to ask to what extent does trade support the GDP and the savings of the country, and we can define the “Capital Productivity” = 1 + log(GDP*/N*) where GDP* is the “capitalized GDP” measure that we used to calculate GW*, and we are thinking of N*, which is basically the “fixed capital” and the “inventories” for consumption or export, plus the Coase Dividend due to trade, as “supporting” the GDP*; if we omit the fixed capital and the inventories, and consider only GW*, then we have the “Trade Productivity” = 1 + log(GDP*/GW*); please see Figure 2.1 below.

The IMF also maintains information on “savings”, which we can think of as our accumulated income net of what we require to live, and there are some places that seem to be really expensive places to live, and we need to wonder where it all comes from, and how will they keep it; please see Figure 2.1 below.

Exhibit 2: World Trade Productivity & Emigration/Immigration Policy (Live It Up)

Figure 2.1: World Trade Productivity

For more information on the “Five Equations of State”, and an introduction to the terms that we have used here, please see our Post “(B)(N) Through the Looking-Glass“, and for the really hard rocks, the Theory of the Firm which is based on The Process.

And for more information on real “risk management” in modern times and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary and “(P&I) Dividend Risk and Dividend Yield“, and our recent Posts “(P&I) The Profit Box” and “(P&I) The Process – In The Beginning“; and we’ve also profiled hundreds of companies in these Posts and the Search Box (upper right) might help you to find what you’re looking for, such as “(B)(N) TLM Talisman Energy Incorporated” or “(B)(N) ATHN AthenaHealth Incorporated” or “(B)(N) PETM PetSmart Incorporated“, to name just a few.

And for more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice. And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

And for more on what risk averse investing has done for us this year, please see our recent Posts on “(P&I) The Easy (EC) Theory of the Capital Markets” or “(B)(N) The Easy (EC) Theory of the S&P 500“, and the past, The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.