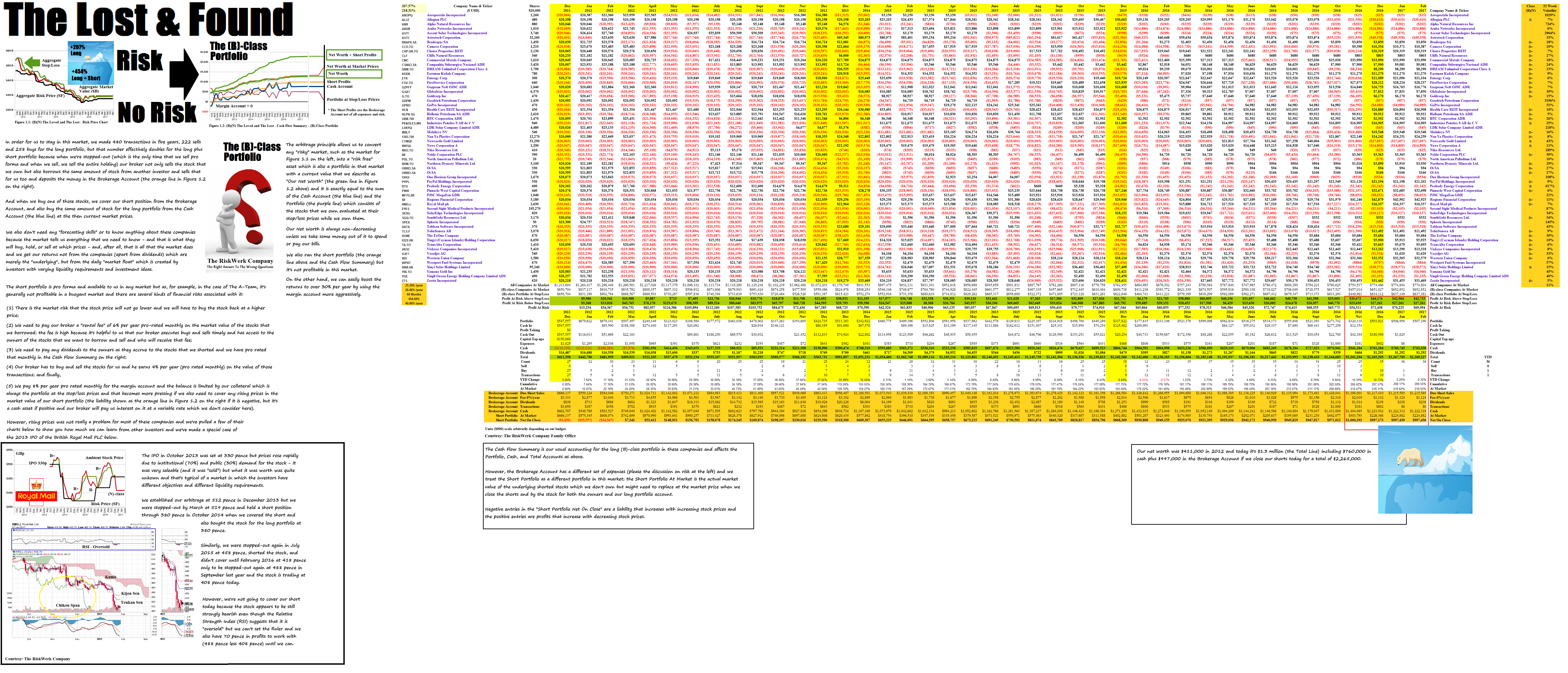

(B)(N) The A-Team vs The Lost & Found

If there’s a bear market coming, please hurry.

Drama. There are about seventy-five stocks in our World Trade Portfolio on which we were stopped-out less than six times in the last five years for an average of only once a year and sometimes they lingered as a (B-) stock for a few months until we could buy them back at a lower price and there was nothing for us to do until we could.

We’ll call them “The A-Team” and everybody likes them – everybody likes good earnings and good dividends – and those stocks are trading now at mostly high prices and they are expensive to buy and we have to wonder about the upside; please see below for more details.

But that’s only the tip of the iceberg because there are another more than five hundred of these World Class stocks that have traded positively in our (B)-class portfolio for more than 80% of the time in the last five years and, therefore, for more than fifty months of the last sixty and we have owned them for as long as we could maintain our usual risk price, stop/loss price, and market price arbitrage on them and if the investors sold us out, we gave them our stock and we took their money.

Simple but we’ll explain below how that works because that’s where the money is and not so much in good earnings and good dividends which belong to the company and not to the “stock price” which could be anything at all.

For example, the A-Team that everybody liked returned +224% in dividends and capital gains in the last five years in our (B)-class portfolio and we still own most of them for an average return of +26% per year and we have more than tripled our wealth with no risk at all thanks to the “market” which we think of as our friend and not our enemy.

But below the tip of iceberg, there is “The Iceberg” and over 1,000 companies in our World Trade Portfolio that were much harder to hold on to but we didn’t lose any money in trying; we never do because that’s our first rule in investing – don’t lose your money – and it’s a simple equation: if we lose 50% of our money, we have to earn 100% on what’s left just to break even. How are we going to do that?

Thank you, Wall Street.

And, indeed, at the very bottom of the iceberg there are (or there were pending bankruptcy or delisting for some of them) sixty companies that have lost nearly 50% of their aggregate market value since 2012, and much more for some of them, and although the investors aren’t sure whether they like them or not at these low prices, they’ve bid them up by 17% in the last twelve months and so we’ve called them “The Lost & Found”.

And we love them because the long and short portfolio in those stocks has returned +454% on our money and an average of +40% per year for five years and they have more than quintupled our wealth with no risk at all – awesome – and we know exactly how to do it again and again with just a stock chart, a ruler, and a good eye as long as there is a market somewhere.

Unsinkable, they said.

And the moral of this story is that if you’re not getting 20% or more per year on your investments, or in your “risky” pension plans made “riskless” for you, they say, then you’re not an investor – you’re a passenger and the trip that you bought is to the Food Bank and it’s not to New York like they said.

The A-Team

Three of the companies on the A-Team have been acquired and are no longer trading (Tenaga Nacional Berhad, Jarden Corporation, and Lorillard) and two of them (both listed in Mexico and trading in pesos) are currently trading as a (B-) and we’ve been stopped-out on them and we’re waiting to buy them back at a lower price (please see below) but all of the others are currently trading as a (B+) and, therefore, at a “high price”.

But that was also true in 2012 at much lower prices that seemed high then and we knew that they were “high” because they were all trading above their price of risk and we could establish our usual risk price, stop/loss price, and market price arbitrage on them.

And although the aggregate market value of these companies has increased by +140% and an average of 20% per year since 2012 by just buying and holding, it’s unlikely that they’ll do it again this year and we expect about +14% in the (B)-class portfolio based on their current normalized annual volatility (6% per year) and dividend yield (1.6%) but the buy and hold investors on what they like need to buckle-up because they could be getting a lot less than that.

On the other hand, the (B)-class portfolio in these same companies has produced +224% at the current stop/loss prices and an average of +26% per year so far and we can afford a slack year if there is one.

Exhibit 1: The A-Team

Arbitrage |

Figure 1.1: GAPB.MX Grupo Aeroportuario del Pacifico de CV ADR (B-) |

Figure 1.2: PINFRA.MX Promotora Y Operadora de Infraestructura SAB de CV ADR (B-) |

The Lost & Found

The most celebrated and strangest portfolio consists of the sixty companies that we dredged from the bottom of the iceberg and the long part of it returned only +207% (sorry) and an average of 25% per year in the (B)-class portfolio but it’s a small market now worth only $300 billion which has lost nearly 50% of its value since 2012.

But the long portfolio also served as the collateral for the short portfolio that we ran in parallel with the same companies that we had been stopped-out on and the combined portfolio (long plus short) returned +454% and an average of 40% per year with no risk at all and we could take out all of our investment ($400,000) in cash by the end of 2013, and again two years later, and it would have made no difference in how we ran the portfolio for the last three years – it’s a perpetual bond that might never stop paying us and it runs itself with a little help from our ruler now and then.

And it gets worse.

Thank you again, Wall Street

We’re currently positioned in thirty-six of these companies and the indicated market volatility is 11% with a current dividend yield of 2.6% so that we can expect a return of about +25% (the dividend yield plus twice the volatility) in the next year.

Thank you again, Wall Street. How long do you think that you can keep doing this? And when will you give us the Bear Market?

Exhibit 2: The Lost & Found

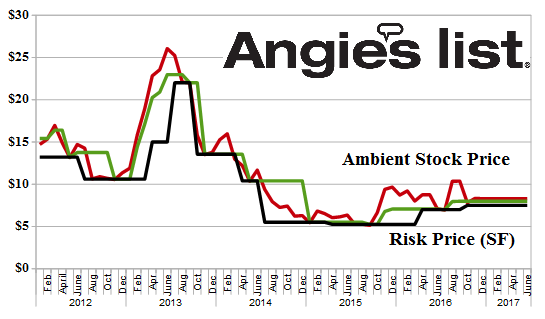

Figure 2.1 ANGI Angie’s List Incorporated (B+) |

Figure 2.2: ARR Armour Residential REIT Incorporated (B+) |

Figure 2.3: CCO Cameco Corporation (B+) |

Figure 2.4: CSIQ Canadian Solar Incorporated (B+) |

Figure 2.5: DRM DREAM Unlimited Corporation Class A (B+) |

Figure 2.6: KODK Eastman Kodak Company (B+) |

Figure 2.7: 0322.HK Tingyi (Cayman Islands) Holding Corporation (B+) |

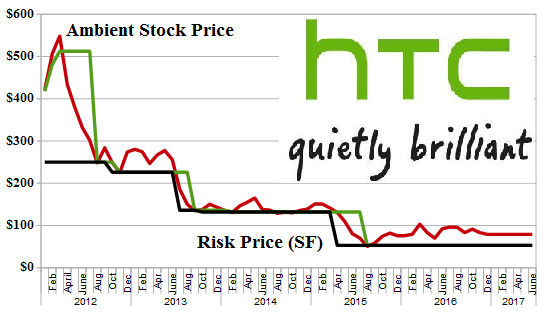

Figure 2.8: 2498.TW HTC Corporation ADR (B+) |

Figure 2.9: CLF Cliffs Natural Resources (B+) |

Figure 2.10: CQWA Companhia Siderurgica Nacional ADR (B+) |

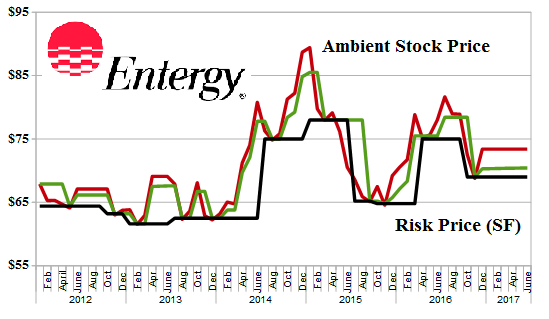

Figure 2.11: ETR Entergy Corporation (B+) |

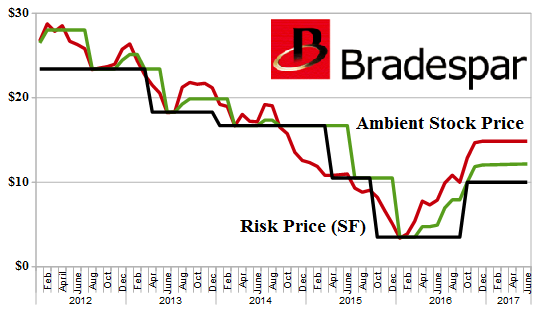

Figure 2.12: FXMA Bradespar SA (B+) |

Figure 2.13 G Goldcorp Incorporated (B+) |

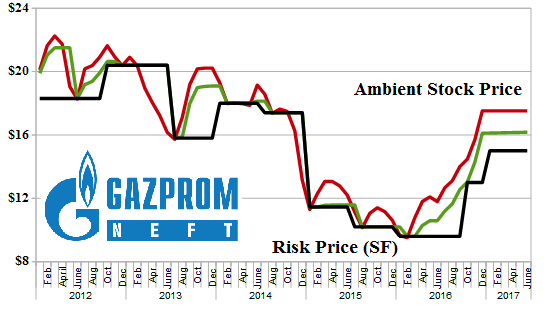

Figure 2.14: GZPFY Gazprom Neft OJSC ADR (B+) |

Figure 2.15: HLPN Hellenic Petroleum SA ADR (B+) |

Figure 2.16: OIBR Oi SA (B+) |

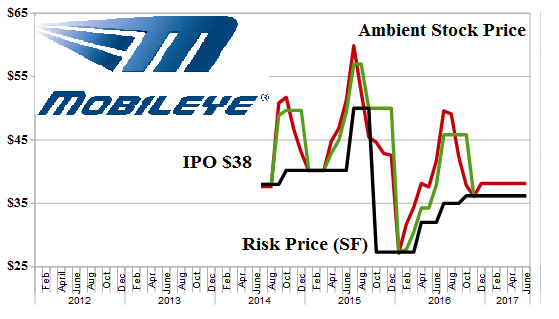

Figure 2.17: MBLY Mobileye NV (B+) |

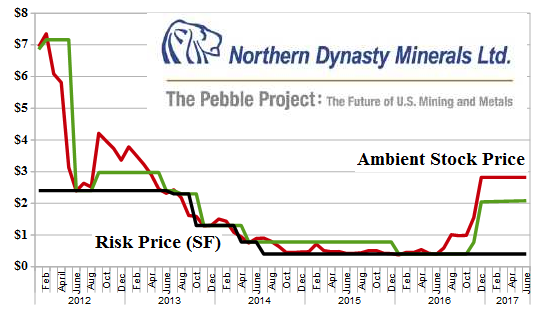

Figure 2.18: NDM Northern Dynasty Minerals Limited (B+ |

Figure 2.19: NE Noble Corporation (B+) |

Figure 2.20: RMG.L Royal Mail PLC (B-) |

Figure 2.21: SGQ SouthGobi Resources Limited (B+) |

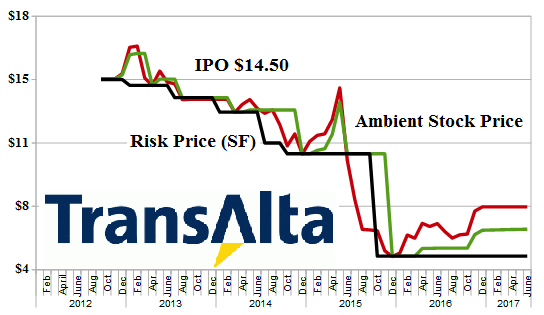

Figure 2.22: TA TransAlta Corporation (B+) |

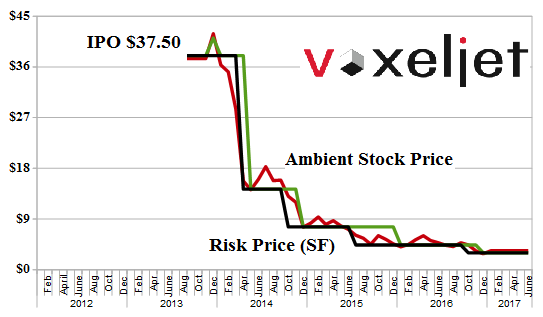

Figure 2.23: VJET VoxelJet AG (B+) |

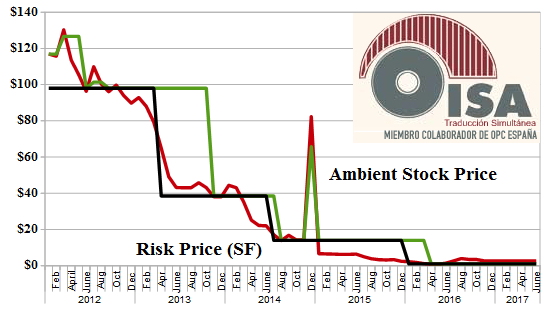

Figure 2.24: PE&OLES.MX Industrias Penoles SAB de CV |

For more examples of the (B)-class portfolio in difficult markets, please see our recent Posts on”The “W” Syndrome“, Steel, Green Energy, UFOs and the High Flying Techs, and The Coal War which is heating-up again now; and the Canadian Mines have also taken-off – please see our recent Post “(B)(N) Extreme Economics – The (New) Canadian Mines” for a heads-up on that as well as The Great Rotation & Twenty Hot Canadians 2017.

And for more information and examples of the Free Market Yield and the terms that we have used above, please see our Posts “(P&I) The Dismal Equation (Ecclesiastes 9:1)” and “(B)(N) S&P 100 Volatility Risk and The Full Moon” and “(B)(N) NASDAQ 100 Volatility and The Stone Bunnies“ and for an introduction to The Barometer “(B)(N) What’s A Girl To Do” or “(P&I) The Swiss Franc Debacle“.

And for more information on real “risk management” in modern times and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary and “(P&I) Dividend Risk and Dividend Yield“, and our recent Posts “(P&I) The Profit Box” and “(P&I) The Process – In The Beginning“; and we’ve also profiled hundreds of companies in these Posts and the Search Box (upper right) might help you to find what you’re looking for, such as “(B)(N) TLM Talisman Energy Incorporated” or “(B)(N) ATHN AthenaHealth Incorporated” or “(B)(N) PETM PetSmart Incorporated“, to name just a few.

And for more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice. And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

And for more on what risk averse investing has done for us this year, please see our recent Posts on “(P&I) The Easy (EC) Theory of the Capital Markets” or “(B)(N) The Easy (EC) Theory of the S&P 500“, and the past, The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”). The Canada Pension Bond®™, The Medina Bond®™, The Barometer®™, the Free Market Yield®™ and Extreme Economics®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.