(B)(N) Extreme Economics – Depressions Are In

Canada! Not Just Hockey

Drama. This year’s big winner in the Canadian Mutual Fund Lottery was Toronto-based Logiq Asset Management Incorporated which has managed an enormous one year return of +64% on Canadian drillers and service companies, wannabe gold and silver mines, and materials companies and has leveraged their CAD$150 million fund into a $2.5 billion behemoth with new partners Aston Hill Financial Incorporated, Front Street Capital 2004 and Tuscarora Capital Incorporated all wanting to bask in the nuclear afterglow of yesterday’s Logiq (Bloomberg, December 14, 2016, Top Canada Mutual Fund Manager Bullish on Oil Services for 2017).

Do we sound “disrespectful”? Yes, we are, because that’s how the markets roll – like drunken sailors in the “roll bar” – and if we’re going to be “investors” in their market then we have to roll with them and keep on rolling them like the Kung Fu because the (B)-class portfolio in these same companies in our World Trade Portfolio did better than that – it returned +85% this year and even more for an average of +34% per year for five years to increase our real net worth by +315% at our current stop/loss prices (and +400% at the current market prices which we need to look at today) and it can’t be any less than that no matter how we have to roll next year.

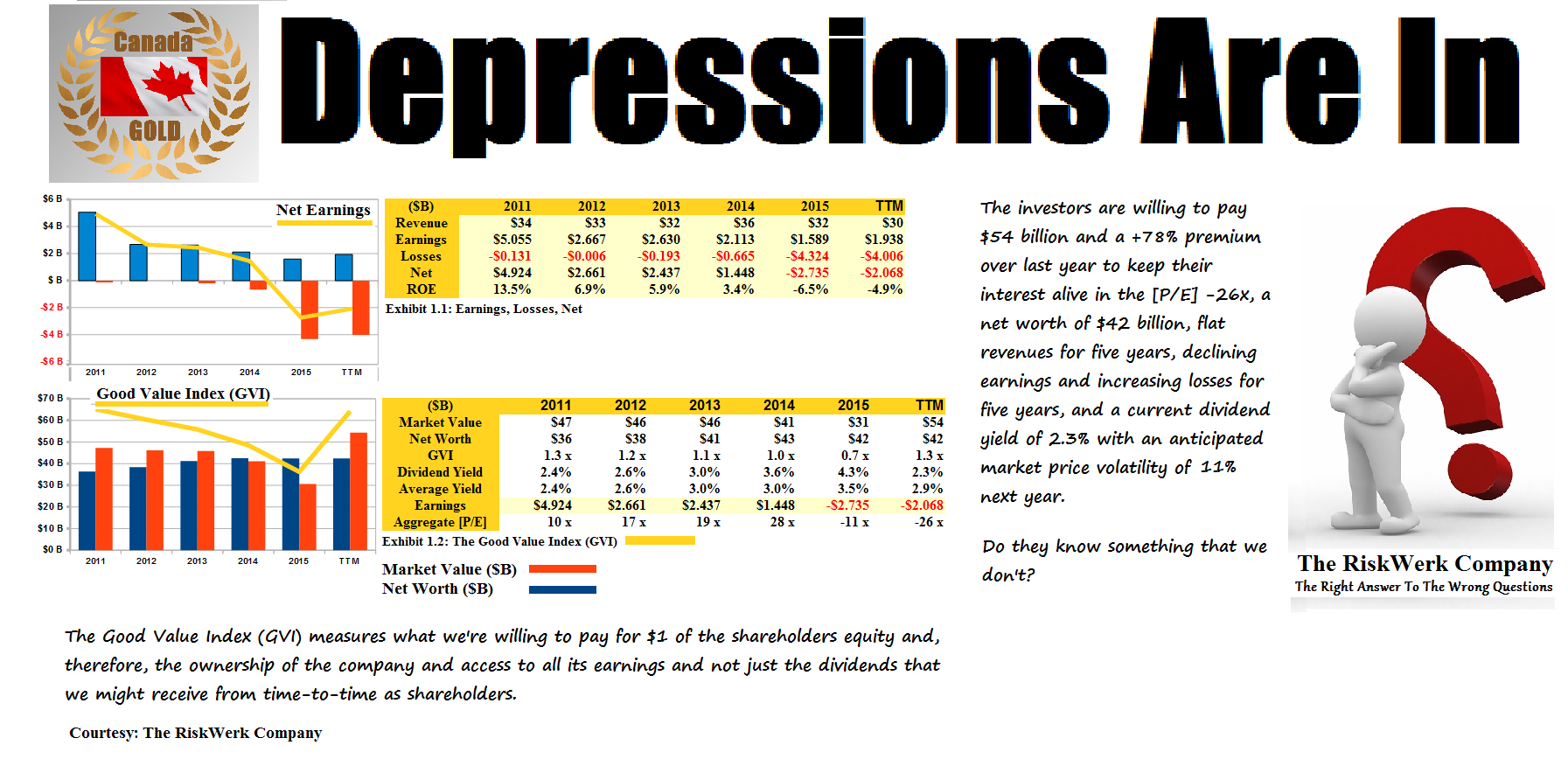

On the other hand, this “market” which consists exactly of those companies, their investors and how much money they have to spend on their ideas and for how long they can keep spending it (like the drunken sailors or not), is in an “economic depression” with flat revenues and increasing net losses for five years straight, sky-high stock prices that are up 78% this year with a negative [P/E] multiple of (-26x) meaning, basically, that the investors are willing to pay $1 for $26 of losses, and it has a Free Market Yield of (-3.4%) with an expected price volatility of 11% next year which could be a good or bad surprise when the celebration is over – after all, the “market” is always right and we need to be in it or be wrong; please see Exhibit 1 below for more information on the “closing time”.

For those of you who just can’t seem to score, we’ve provided some details below on how we’ve improved the game with eighteen of these companies, four of which are already in a melt-down and rolling downhill into Somebody’s Slush Fund; please click on the charts and again to make them larger as required.

Exhibit 1: Depressions Are In – Fundamentals & Cash Flow Summary

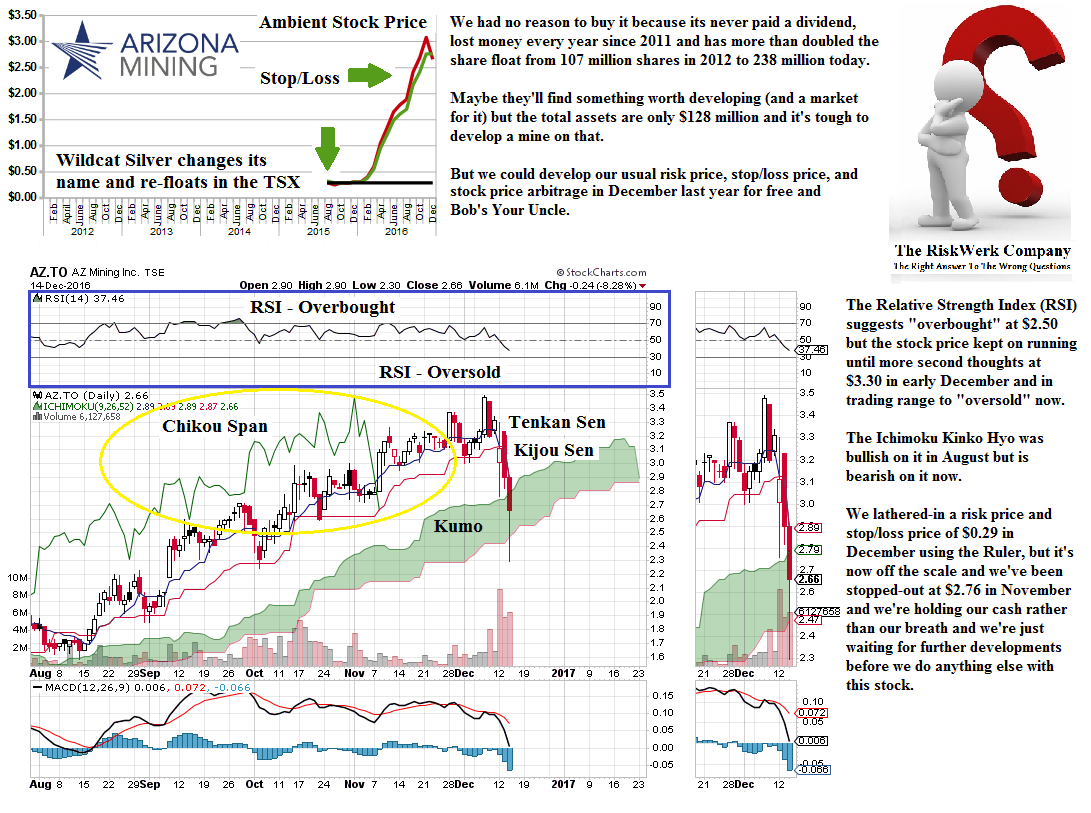

Figure 1.1: AZ Arizona Mining Incorporated (B-) |

Figure 1.2: ACO.X Atco Limited Class I (B-) |

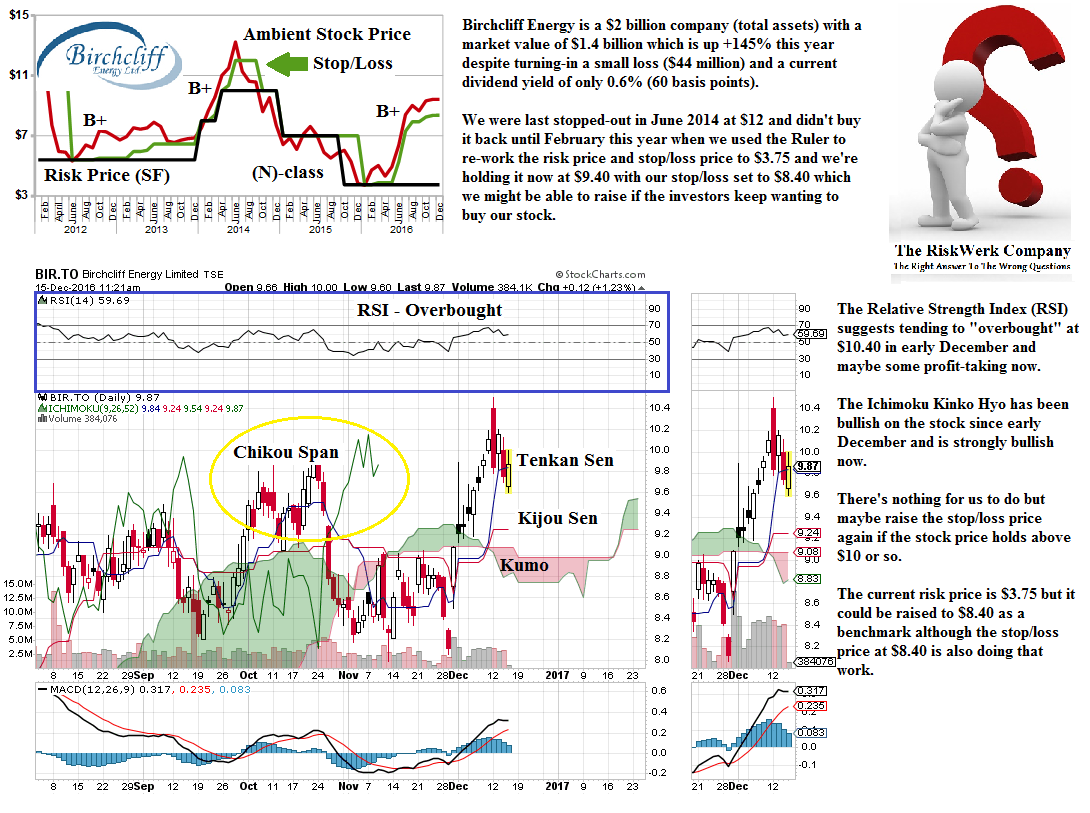

Figure 1.3: BIR Birchcliff Energy Limited (B+) |

Figure 1.4 CFW Calfrac Well Services Limited (B+) |

Figure 1.5: FRC Canyon Services Group Incorporated (B+) |

Figure 1.6: CR Crew Energy Incorporated (B+) |

Figure 1.7: FTS Fortis Incorporated (B-) |

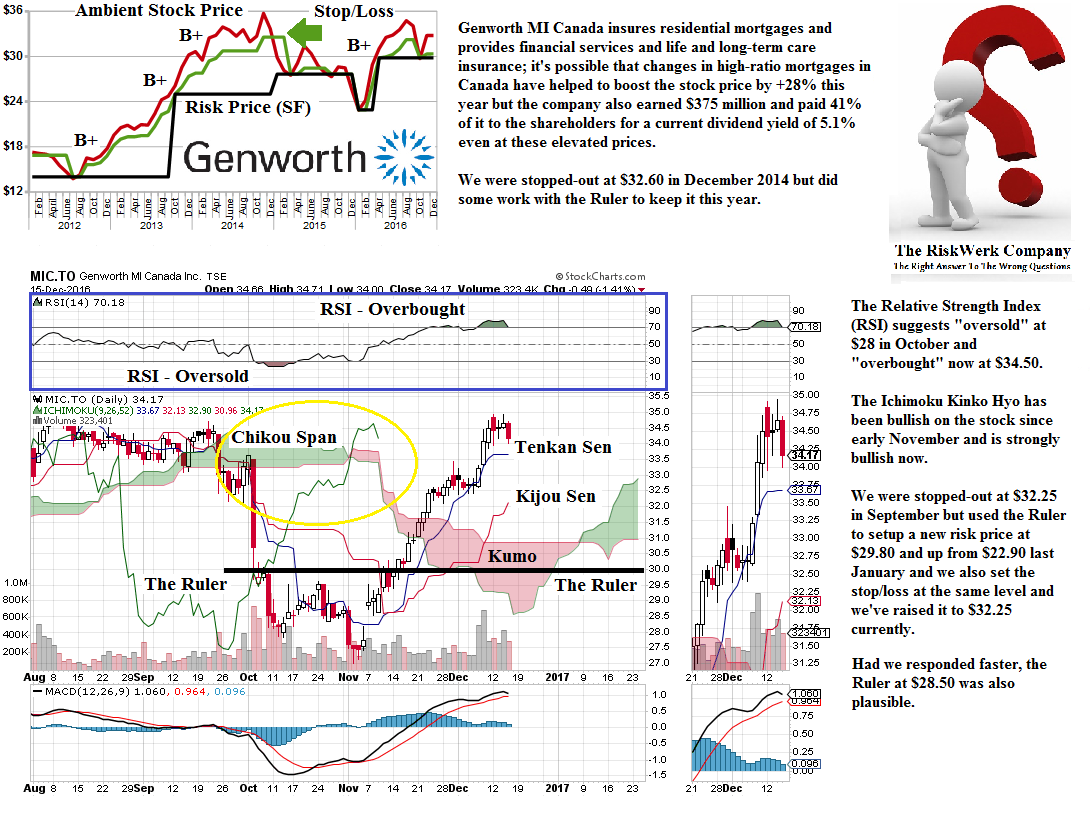

Figure 1.8: MIC Genworth MI Canada Incorporated (B+) |

Figure 1.9: MDI Major Drilling Group International Incorporated (B-) |

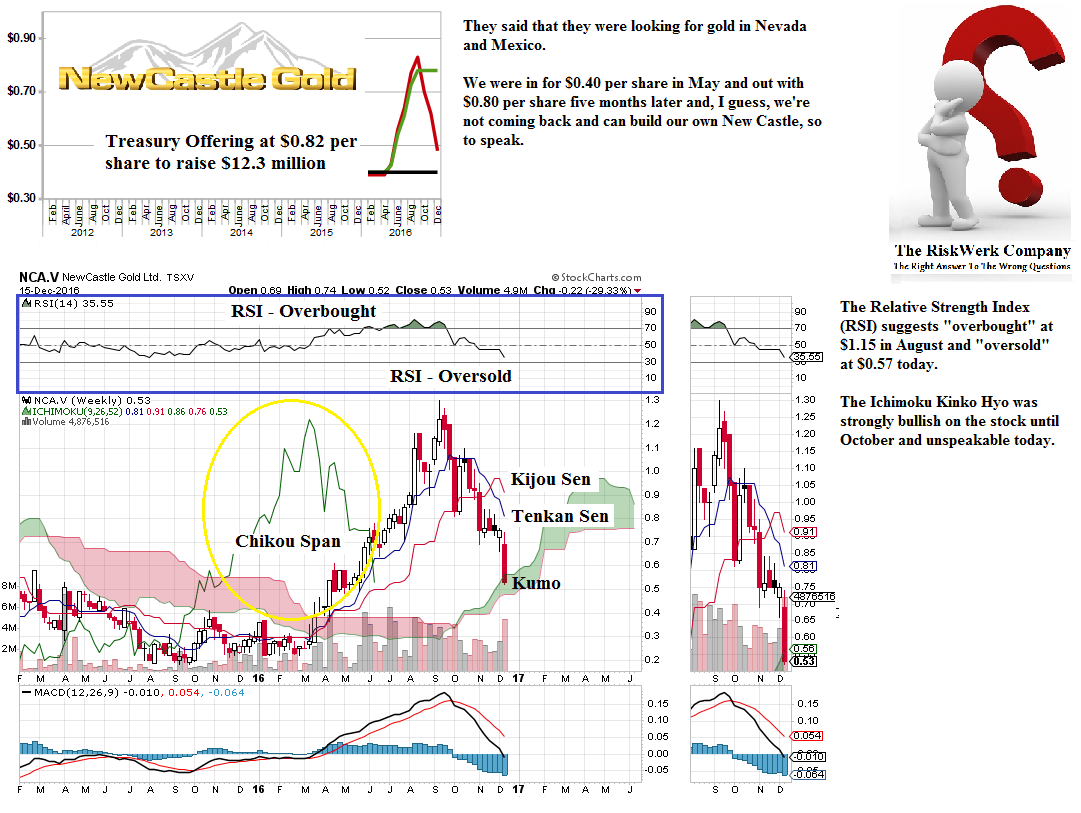

Figure 1.10: NCA.V Newcastle Gold Limited (B-) |

Figure 1.11: PSI Pason Systems Incorporated (B+) |

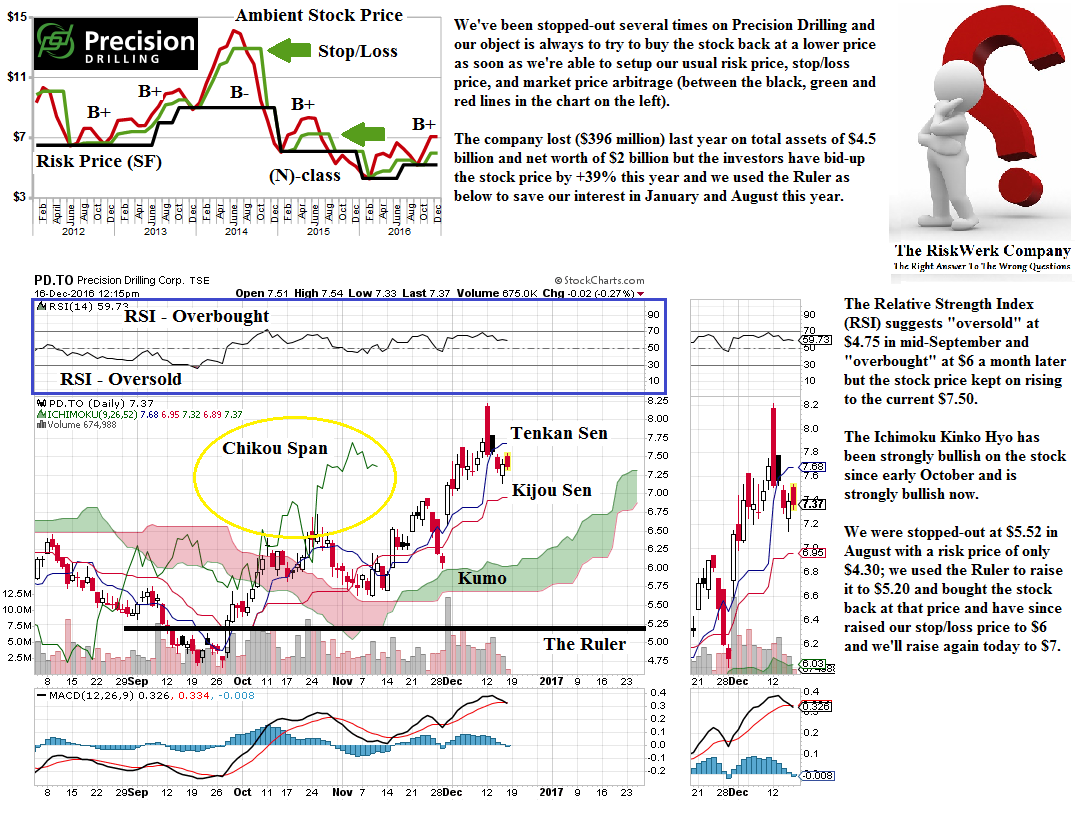

Figure 1.12: PD Precision Drilling Corporation (B+) |

Figure 1.13: SVY Savanna Energy Services Corporation (B+) |

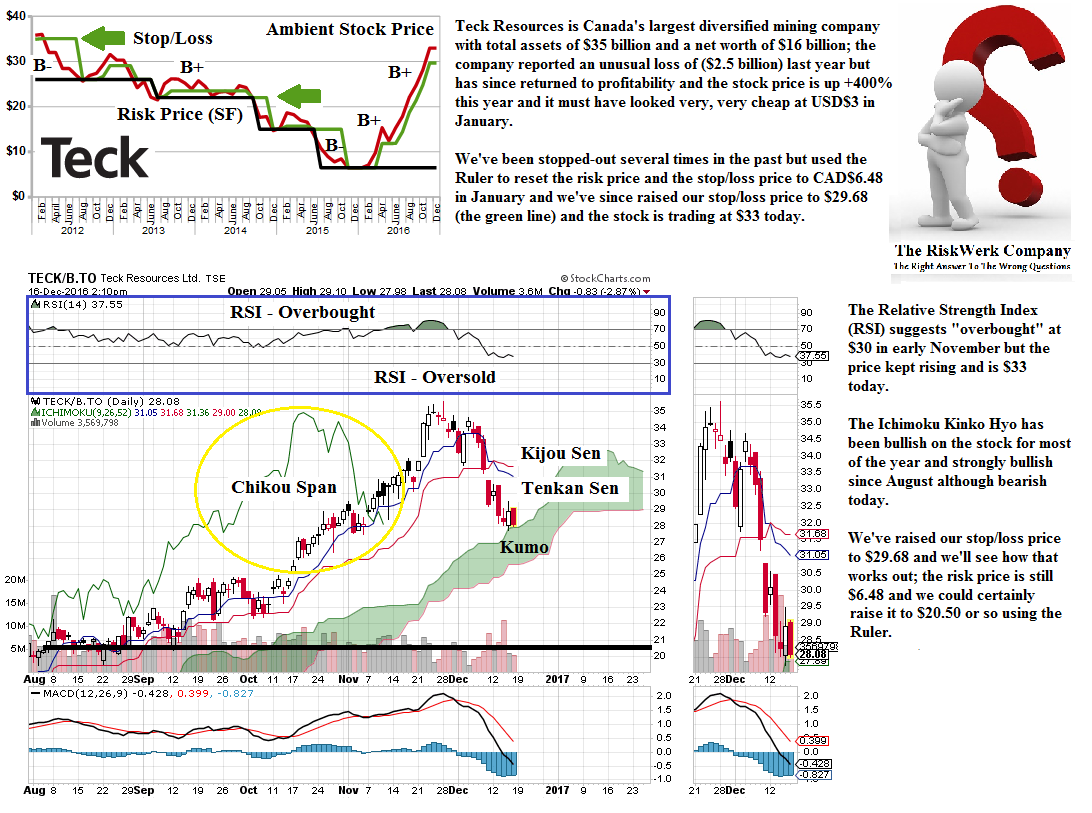

Figure 1.14: TCK.B Teck Resources Limited (B+) |

Figure 1.15: TIH Toromont Industries Limited (B+) |

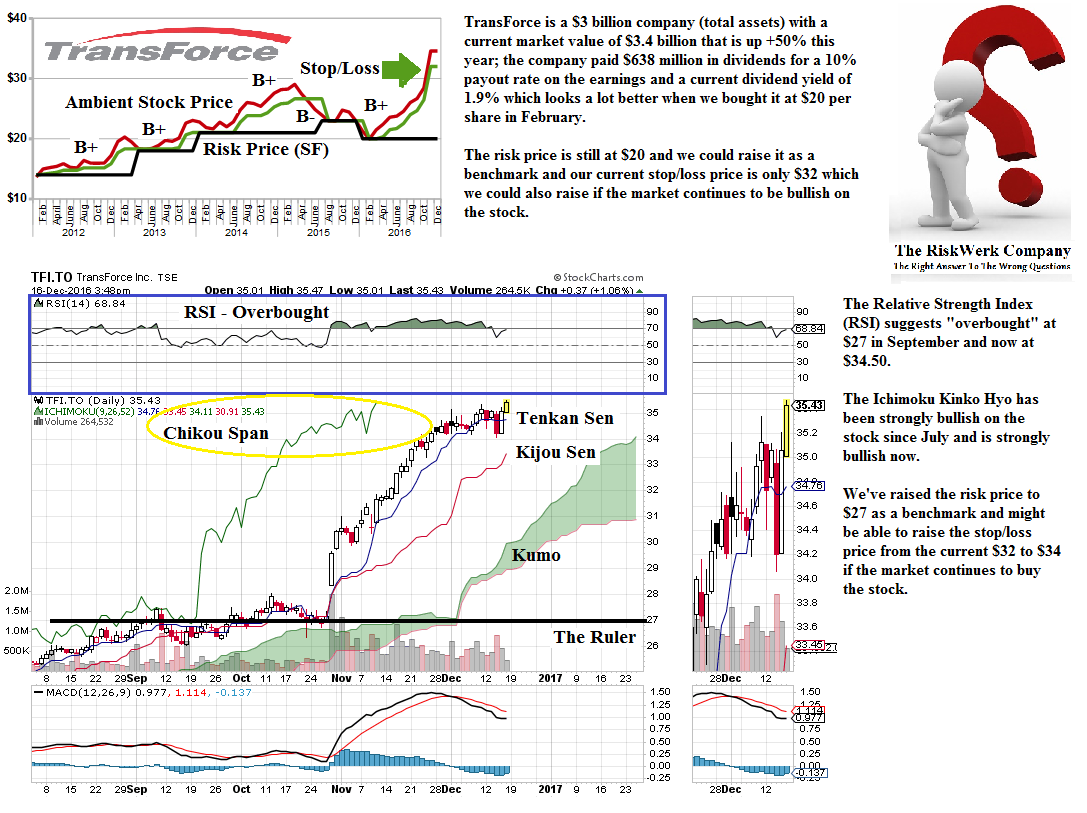

Figure 1.16: TFI TransForce Incorporated (B+) |

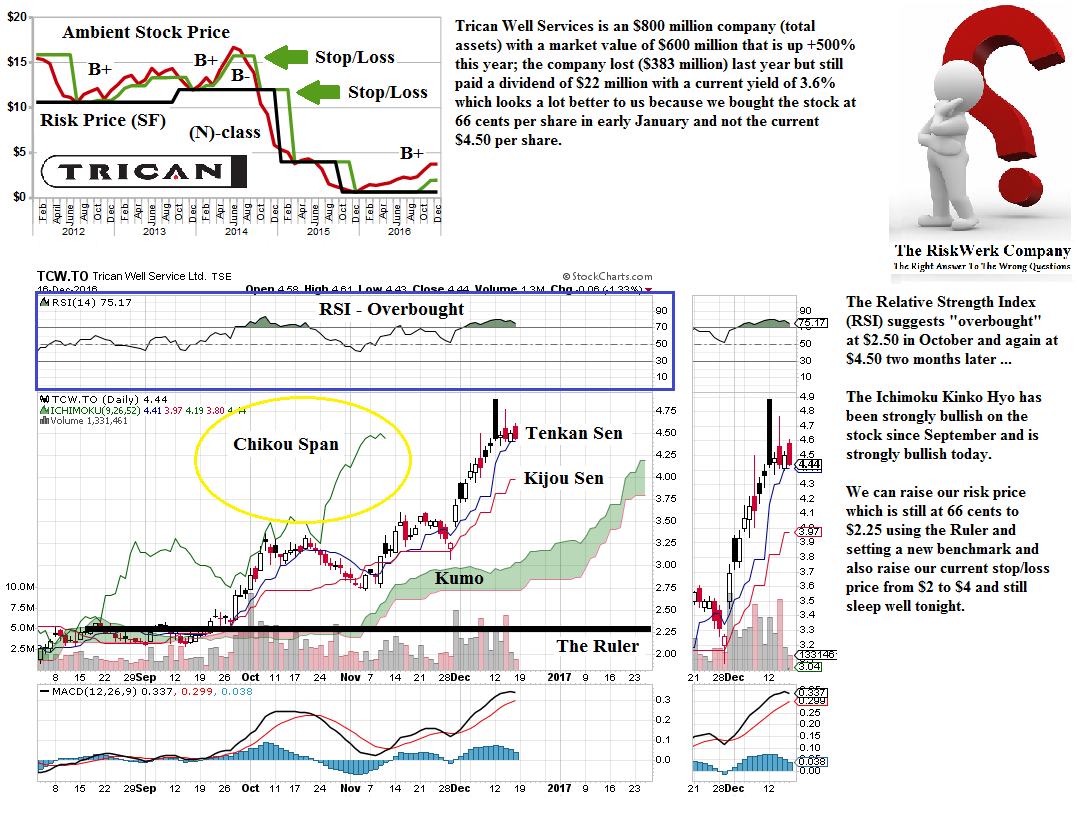

Figure 1.17: TCW Trican Well Service Limited (B+) |

Figure 1.18: XDC Xtreme Drilling Corporation (B+) |

Despite good investment returns, the income problem is different and needs more than just paper money; please see our Post on “The Personal 12% Bond” for more information.

Despite good investment returns, the income problem is different and needs more than just paper money; please see our Post on “The Personal 12% Bond” for more information.

And for more examples of the (B)-class portfolio in difficult markets, please see our recent Posts on”The “W” Syndrome“, Steel, Green Energy and The Coal War which is heating-up again now; and the Canadian Mines have also taken-off – please see our recent Post “(B)(N) Extreme Economics – The (New) Canadian Mines” for a heads-up on that.

And for more information and examples of the Free Market Yield and the terms that we have used above, please see our Posts “(P&I) The Dismal Equation (Ecclesiastes 9:1)” and “(B)(N) S&P 100 Volatility Risk and The Full Moon” and “(B)(N) NASDAQ 100 Volatility and The Stone Bunnies“ and for an introduction to The Barometer “(B)(N) What’s A Girl To Do” or “(P&I) The Swiss Franc Debacle“.

And for more information on real “risk management” in modern times and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary and “(P&I) Dividend Risk and Dividend Yield“, and our recent Posts “(P&I) The Profit Box” and “(P&I) The Process – In The Beginning“; and we’ve also profiled hundreds of companies in these Posts and the Search Box (upper right) might help you to find what you’re looking for, such as “(B)(N) TLM Talisman Energy Incorporated” or “(B)(N) ATHN AthenaHealth Incorporated” or “(B)(N) PETM PetSmart Incorporated“, to name just a few.

And for more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice. And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

And for more on what risk averse investing has done for us this year, please see our recent Posts on “(P&I) The Easy (EC) Theory of the Capital Markets” or “(B)(N) The Easy (EC) Theory of the S&P 500“, and the past, The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”). The Canada Pension Bond®™, The Medina Bond®™, The Barometer®™, the Free Market Yield®™ and Extreme Economics®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.