(B)(N) Extreme Economics – How Not To Be Wrong

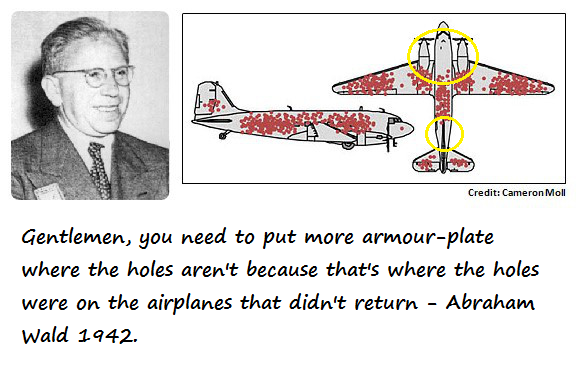

Abraham Wald (1902-1950)

Drama. In 1942, Abraham Wald advised the British Bomber Fleet on how to best protect their bombers with the least additional weight of armour and he said that rather than add more armour-plate to where the holes were on the returning bombers, which was what the British were doing at the time, you had to add more armour-plate to where the holes weren’t because those were the holes in the bombers that didn’t come back.

And that’s an example of “maximizing returns without an undue risk of loss” and it’s correctly called “survivorship bias” in this case and “100% capital safety” in ours.

However, almost all of our pension plans claim to be doing exactly that – they are bravely “maximizing returns without an undue risk of loss” for us stay-at-homes – and like the British Bomber Fleet, they’re trying to do it in the most obvious way by “fixing the holes” and buying only the stocks of “good companies” (they say) and possibly taking a “position” in them and, secondly, by buying diversified global portfolios of stocks and bonds in buoyant economies, at least when they bought them.

And as a consequence, like the British bombers, only an average of about 7% of our money ever returns to us every year and in some years it’s a bit more, maybe 15% once in a while because the market was “good”, and in other years such as 1998 or 2008, we have to pay them money in order to get back what they lost and they attribute all of this “uncertainty” to “risk” which they have failed to manage.

Figure 1: 20 & 30 Year Total Returns S&P 500 Companies

But what they have failed to do, and actively refuse to do, is to manage our money for 100% capital safety no matter what and in the long run, we can expect no better returns from them than from those of the legions of managers before them who have been doing exactly the same things that they are and, so, are challenging “risk” to defeat them – and that’s easy and it happens all the time; please see Figure 1 on the right for the reason that your retirement benefits will not be what they should be (Bloomberg, October 26, 2016, How the Next President Could Save Social Security).

Are you worried? You should be worried because you’re flying heavy with your new silver plates in all the wrong places.

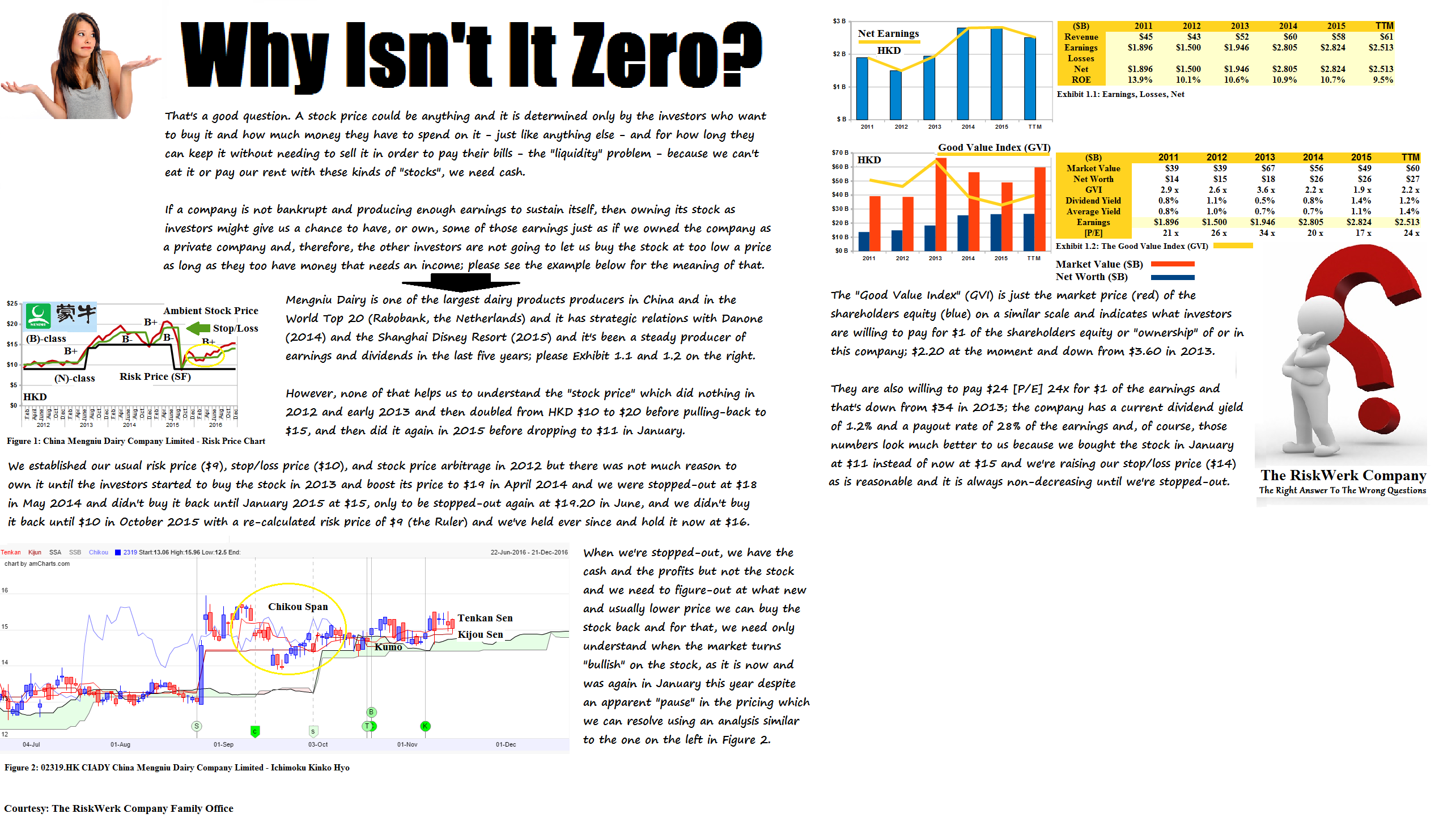

Moreover, there are well-known reasons that these methods don’t work and your portfolio manager should know them and it’s not excusable for a stock market investor to get less than the typical return on the shareholders equity which is about 8% per year in the major markets and the owners of real companies are wasting their time and money if they’re not getting at least that; please see below.

How Not To Be Wrong – The Float

There is a solution to this “investment problem” of pitiful returns and it’s not unlike Mr. Wald’s solution to the problem of cant knowledge and perception in the British Bomber Fleet and we implement it routinely with just “a stock chart, a ruler, and a good eye” and there are many examples in our Posts; the practical method is just a “heuristic” but the Theory of Firm explains why it works.

For example, 740 companies of the 1,600 companies in our World Trade Portfolio traded at more than 50% above their average 2012 prices at some time in the last five years – they must have been “good companies” – but forty of those have failed to keep those values and at some time this year they traded at less than 20% above their average 2012 values – maybe they weren’t such good companies after all?

On the other hand, 700 of those companies traded above their 2012 average price and have continued to trade at above that level, but for how much longer?

And we don’t know anything about these companies except that at various times they were trading above their price of risk for reasons that we also don’t know anything about (please see The Tao of Stock Prices) but we could use the arbitrage principle and our rule for 100% capital safety – we will not buy or hold anything for which we cannot guarantee 100% capital safety – allowed us to triple our money in five years with no risk at all.

But even if we don’t know anything about the companies, we know a lot about this “market” which consists exactly of these companies, their investors, and how much money they have and for how long they can invest in them before making a decision or preference for “liquidity” to pay their bills or their pensioners – we call it “The Float”.

The Free Market Yield in this market of forty “good companies” is 1.61% and, therefore, this is a mildly inflationary or “growth” economy; and the current dividend yield is 2.6% in aggregate and the normalized annual volatility is 10.9%.

The Free Market Yield in this market of forty “good companies” is 1.61% and, therefore, this is a mildly inflationary or “growth” economy; and the current dividend yield is 2.6% in aggregate and the normalized annual volatility is 10.9%.

And so we expect (provably) to earn about 24% per year in capital gains and dividends (the dividend yield plus twice the expected and normalized annual volatility) in this market in the next year and to earn it in exactly in the same way that we earned it in the previous five years – an average of 24.7% per year with no risk because we don’t invest in the companies per se nor in how good they are, or not, but rather we “invest in the investors” and the float that they create in their vain pursuit of an income on their money; please see Exhibit 1 below for more details (and click on it and again to make it larger as required).

Exhibit 1: How Not To Be Wrong – A Random Walk in Stocks and The Float

For more examples of the (B)-class portfolio in difficult markets, please see our recent Posts on”The “W” Syndrome“, Steel, Green Energy and The Coal War which is heating-up again now; and the Canadian Mines have also taken-off – please see our recent Post “(B)(N) Extreme Economics – The (New) Canadian Mines” for a heads-up on that.

And for more information and examples of the Free Market Yield and the terms that we have used above, please see our Posts “(P&I) The Dismal Equation (Ecclesiastes 9:1)” and “(B)(N) S&P 100 Volatility Risk and The Full Moon” and “(B)(N) NASDAQ 100 Volatility and The Stone Bunnies“ and for an introduction to The Barometer “(B)(N) What’s A Girl To Do” or “(P&I) The Swiss Franc Debacle“.

And for more information on real “risk management” in modern times and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary and “(P&I) Dividend Risk and Dividend Yield“, and our recent Posts “(P&I) The Profit Box” and “(P&I) The Process – In The Beginning“; and we’ve also profiled hundreds of companies in these Posts and the Search Box (upper right) might help you to find what you’re looking for, such as “(B)(N) TLM Talisman Energy Incorporated” or “(B)(N) ATHN AthenaHealth Incorporated” or “(B)(N) PETM PetSmart Incorporated“, to name just a few.

And for more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice. And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

And for more on what risk averse investing has done for us this year, please see our recent Posts on “(P&I) The Easy (EC) Theory of the Capital Markets” or “(B)(N) The Easy (EC) Theory of the S&P 500“, and the past, The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”). The Canada Pension Bond®™, The Medina Bond®™, The Barometer®™, the Free Market Yield®™ and Extreme Economics®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.

Trackbacks