(B)(N) Extreme Economics – The Pensionnaires

The No Risk, No Max Plan

Drama. The Canada Pension Plan Investment Board (CPPIB) is an arms-length fiduciary manager of the funds provided to it by Canadian taxpayers to ensure their long-term pension, disability and survivor benefits under the Canada Pension Plan (CPP) which was started in 1966 and came under CPPIB management in 1999.

Additional benefits are also paid to pensioners under the Old Age Security (OAS) and Guaranteed Income Supplement (GIS) legislation and these are funded from the general tax revenues of the Government on a pay-as-you-go basis and generally exceed the amounts that are paid to pensioners from the CPP (please see below for the Income Security programs of the Government).

Hence, we have the odd situation of a well-funded CPP with managed investment returns supplemented by unfunded cash payments from the Government in order that pensioners might have no less than a minimum guaranteed income.

We could do worse, and we have done worse and much worse prior to 1999, but can we do better with less risk and more income?

Figure 1: Yes, we can.

And the answer is that yes, we can, with no risk and an income that is limited only by what the rest of the world of investors has to “give” us in their $80 trillion market place and in their unrelenting and unforgiving hunt for an income from their money; please see Figure 1 on the right for more details (and click on it and again to make it larger as required).

The CPPIB is also in that market and its unrelenting efforts to “maximize investment returns without undue risk of loss” have cost us $37.8 billion so far this year (to the end of July) and $100 billion since 2012.

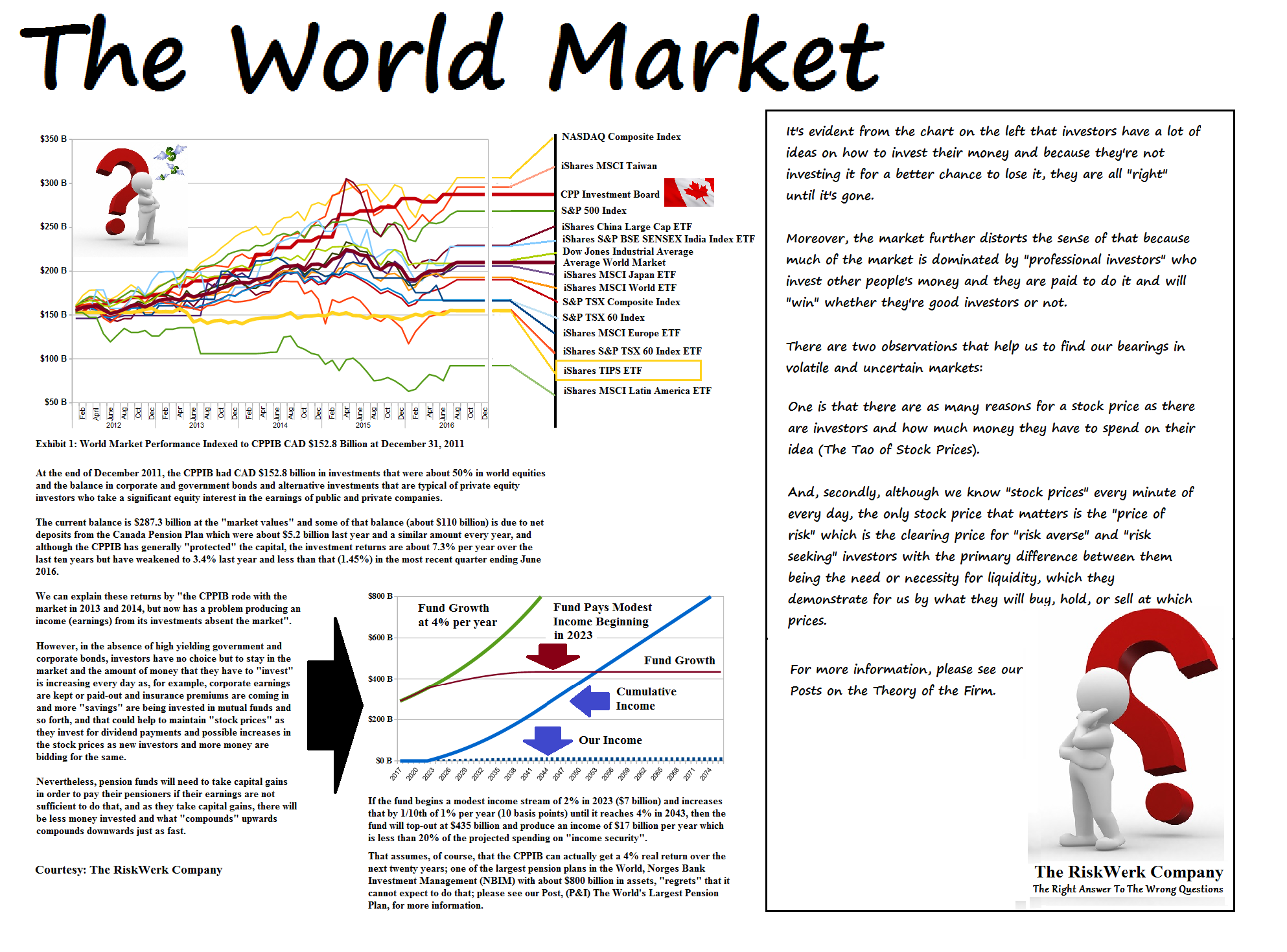

The reason that we use the word “cost” is that the provably “no risk, no max” portfolio that we call the (B)-class portfolio is currently worth $362.4 billion – $100 billion more than the CPPIB portfolio – and it earned those returns in one of the worst of all the markets, the S&P TSX 60 companies (please see Figure 1 above), and we started it with the same money as the CPPIB in 2012, $152.8 billion, but with no annual top-ups and, actually, no top-ups at all.

And our portfolio is currently producing $724 million per month in dividends with no risk at all to the capital; that’s a handsome 2.4% yield on the current portfolio ($362 billion) and effectively, an interest rate on what looks like a government bond but isn’t, and 5.7% per year on the money ($152.8 billion) that we originally put into the “plan” in 2012.

And it cannot be worth less than that ($362 billion) no matter what the market does for the rest of this year or next; in other words, our cost is zero (ZERO) but the CPPIB has already foreclosed on $100 billion and 2/3rds of its capital in 2012, and we have no idea how they’ll do for the rest of the year.

To put this another way, Canadians are currently “paying” the CPPIB $7 million per hour (that’s right, per hour 24/7) this year and they have paid an average of $2.7 million per hour since 2012 to “maximize investment returns without undue risk of loss” because they’re not getting the returns that they could be getting with a policy and plan for no risk and no max at all.

Please see the illustration below for an overview of how that is done and what it means for capital market investing; we’ll explain this outcome in more detail below.

How do you argue with no risk?

Figure 2: Oops? Was that just a wardrobe failure?

If can be done and the recent clean bill of health that was given to the CPPIB for its World Class investment process shows that; please see Figure 2 on the right.

All that we can say, and all that the actuaries and auditors can say, is that the CPPIB is “operating to spec” but the specs don’t include anything about obtaining an income from our money or give us any idea of what that income might be net of an expected 4% per year real return in capital gains and dividends (which they keep) and those returns were 3.4% last year (ending in March) but started-off negative (-0.10% or minus 10 basis points) in June 2015 and their most recent returns are 1.45% in the last three months since March but were negative again (-2.7%) in the first three months of the year.

Even our horse gets 4% real returns.

However, even our horse gets 4% per year real returns in almost every race, and certainly over time.

And that’s the point; the various stocks, bonds, and properties that we might invest in don’t get their price because they’re “pretty” or “foreign” or have good balance sheets; they get their price because other investors need to obtain an income from their money with more or less urgency depending on their needs for liquidity to pay their bills or their pensioners.

But the CPPIB doesn’t have any bills to pay and last year they picked-up another $5.2 billion from the companies and their employees ($38.406 billion received from the CPP less $33.219 billion returned to the CPP for pension payments) and the Government will spend another $46 billion (estimate) on the supplemental OAS and GIS payments and other income security programs in excess of the CPP.

Exhibit 1: Withdrawal Symptoms – Show me the money

Exhibit 2: OK – Here it is, here is the MONEY

For more examples of the (B)-class portfolio in difficult markets, please see our recent Posts on”The “W” Syndrome“, Steel, Green Energy and The Coal War; and the Canadian Mines have also taken-off – please see our recent Post “(B)(N) Extreme Economics – The (New) Canadian Mines” for a heads-up on that.

And for more information and examples of the Free Market Yield and the terms that we have used above, please see our Posts “(P&I) The Dismal Equation (Ecclesiastes 9:1)” and “(B)(N) S&P 100 Volatility Risk and The Full Moon” and “(B)(N) NASDAQ 100 Volatility and The Stone Bunnies“ and for an introduction to The Barometer “(B)(N) What’s A Girl To Do” or “(P&I) The Swiss Franc Debacle“.

And for more information on real “risk management” in modern times and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary and “(P&I) Dividend Risk and Dividend Yield“, and our recent Posts “(P&I) The Profit Box” and “(P&I) The Process – In The Beginning“; and we’ve also profiled hundreds of companies in these Posts and the Search Box (upper right) might help you to find what you’re looking for, such as “(B)(N) TLM Talisman Energy Incorporated” or “(B)(N) ATHN AthenaHealth Incorporated” or “(B)(N) PETM PetSmart Incorporated“, to name just a few.

And for more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice. And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

And for more on what risk averse investing has done for us this year, please see our recent Posts on “(P&I) The Easy (EC) Theory of the Capital Markets” or “(B)(N) The Easy (EC) Theory of the S&P 500“, and the past, The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”). The Canada Pension Bond®™, The Medina Bond®™, The Barometer®™, the Free Market Yield®™ and Extreme Economics®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.