(B)(N) MSAB Melker Schorling AB

The Fundamentals

Drama. Melker Schorling is the founding partner of Melker Schorling AB which runs a number of very selective investments for an elite clientele and despite his modesty, he is often called the man with the Midas Touch (Reuters, July 24, 2016, Melker Schorling, Sweden’s quiet tycoon with the Midas touch).

Fair Market Value in Sweden

The (B)-class portfolio in these six “golden” companies (Hexagon, AAK, Hexpol, Assa Abloy, Securitas, and Loomis) doesn’t have very much work to do because of the substantial positions in both stocks and capital that is managed and owned by Mr. Schorling through the stock company MASB Melker Schorling AB which is a publicly traded holding company and not a limited partnership.

As a consequence, these companies are trading in aggregate at very close to their “Fair Market Value” which is their “price of risk” and the “clearing price” for rational investors constrained primarily by their needs for liquidity, and the stock prices (again in aggregate) have a very low volatility (about 4% per year) that is almost unheard of in New York.

But it gets better. Just buying and holding these stocks on an equal-weighted by value basis has produced an average annual return of 20% per year in dividends and capital gains for the last five years and there appears to be no reason that the portfolio can’t do it again in the next five years.

Moreover, this market is inflationary with respect to the US dollar; in other words, this market is “cheap” in US dollars and an “emerging economy” in growth terms with a Free Market Yield of 1.652% and a Coase Dividend of $58 per $1 of investment which is twice that of the Dow Jones Industrial Companies ($29); please see Exhibit 1 below for more information.

The Hunt For An Income

Of course, we don’t have a “problem” getting 20% or 30% returns on our investments in almost any market in the US, Canada, Europe, or China and the Far East, and many of our Posts demonstrate how we do that and how easy it is to do with just a “stock chart, a ruler, and a good eye”.

“Volatility” doesn’t work but thank you for trying.

But we have a “theory” that works, the Theory of the Firm for which a “stock chart, a ruler, and a good eye” is just a heuristic in the same way that we might ride our bicycle – push off, peddle, and look straight ahead – without knowing the theories of the conservation of energy, momentum, and gravity which explain why it works in more detail and how it might fail.

Which brings us to today’s problem: investors are generally willing to pay 10x earnings, 20x earnings, 30x earnings, and so forth for a stock that might not even pay dividends or have earnings, and we don’t know why.

Why would we pay $1 today for the possibility of 10 cents, 5 cents, 3 cents, and so forth, of earnings a year from now to which we’re not even entitled even if they happen?

The answer is, for example, that [P/E] 20x earnings, looks like the 5% yield on a government or corporate bond if our capital in the stock holds its value, or increases, although most companies don’t payout all of their earnings to the shareholders; it’s typically 40% of their earnings but it could be nothing for a “growth company” or a lot and even more than they earn for a company that’s trying to support the price of its stock.

And secondly, if we don’t pay that price as it’s being demanded, then somebody else will be able to buy the earnings, perhaps all of them in a takeover bid, at a lower price depending only on the owner’s need for liquidity – money to spend to pay their bills (or pensioners or insurance obligations, for example) or for some other investment idea.

Because of that equation, Mr. Schorling needs to keep a close eye on the revenues, earnings, dividend policy, and stock prices for these companies; if the stock prices are “too low” then other investors (or even the companies themselves) will begin to buy them and might even take a “position” in these companies that rivals his own; whereas if the stock prices are “too high” then the companies can benefit by selling treasury stock into that market and Mr. Schorling might need to buy those stocks at high prices in order to maintain his controlling interests.

Please see Exhibit 1 below for an explanation of what it means to buy or sell [P/E] 183x earnings today (and click on it and again to make it larger as required).

The aggregate market value of these companies is about SEK $700 billion (or USD $90 billion) and Melker Schorling AB owns about 9% of it but that’s 100% of his net worth and the stock (MELK.ST) hasn’t been as good to him as its holdings have been to us because he can’t sell it (or treasury stock) and maintain his position and the stock, MELK.ST, has a very low dividend yield of less than 5 basis points (0.05%).

Our preference, therefore, is to look at the companies in the market and currency in which they trade which in this case is Stockholm in the Swedish Krona (SEK) but, of course, they also trade in New York, London, and Frankfurt, for example, and the charts in Exhibit 2 below will help us to catch-up and buy into an “economy” at “low prices” that is an inflationary economy relative to our own; please see Exhibit 2 below for more details.

Exhibit 1: [P/E] 183x Earnings Today MELK.ST Melker Schorling AB

Exhibit 2: Fair Market Value in Sweden

Figure 2.1: HXGBY Hexagon AB ADR (B+) |

Figure 2.2: ARHUF AAK AB ADR (B+) |

Figure 2.3: HXPLF Hexpol AB Class B ADR (B-) |

Figure 2.4: ASAZY Assa Abloy AB Class B ADR (B+) |

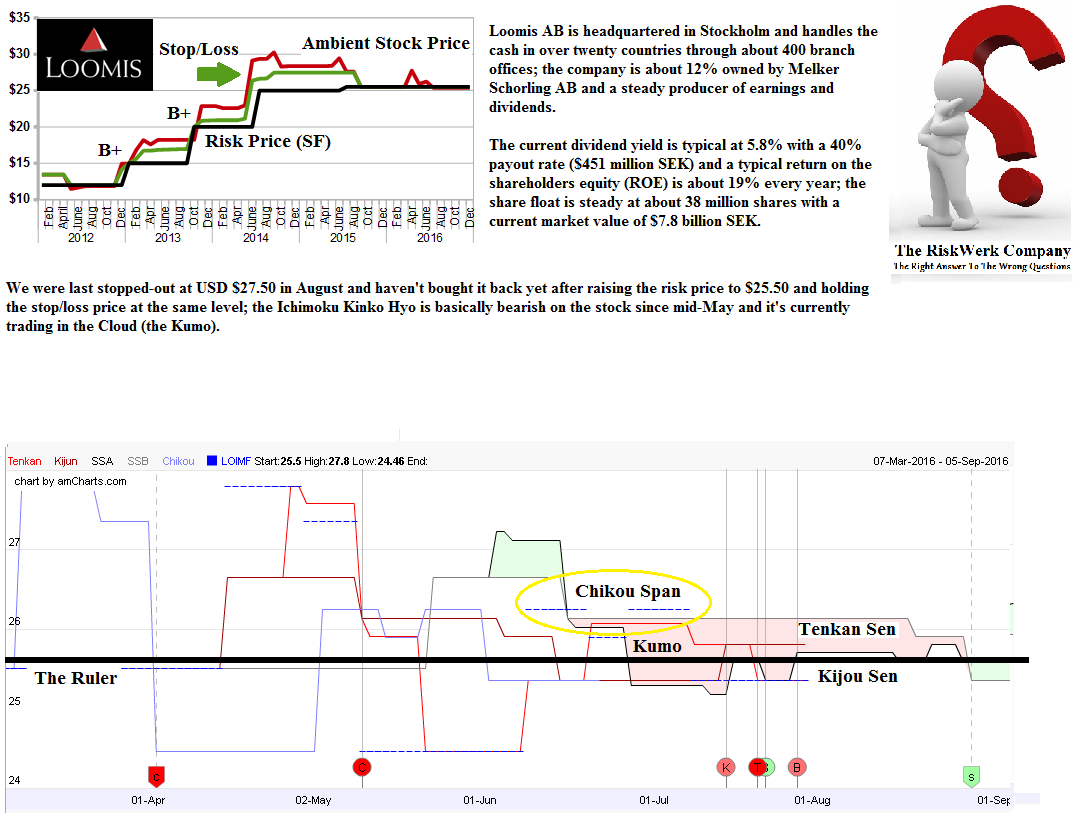

Figure 2.5: LOMF Loomis AB Class B ADR (N) |

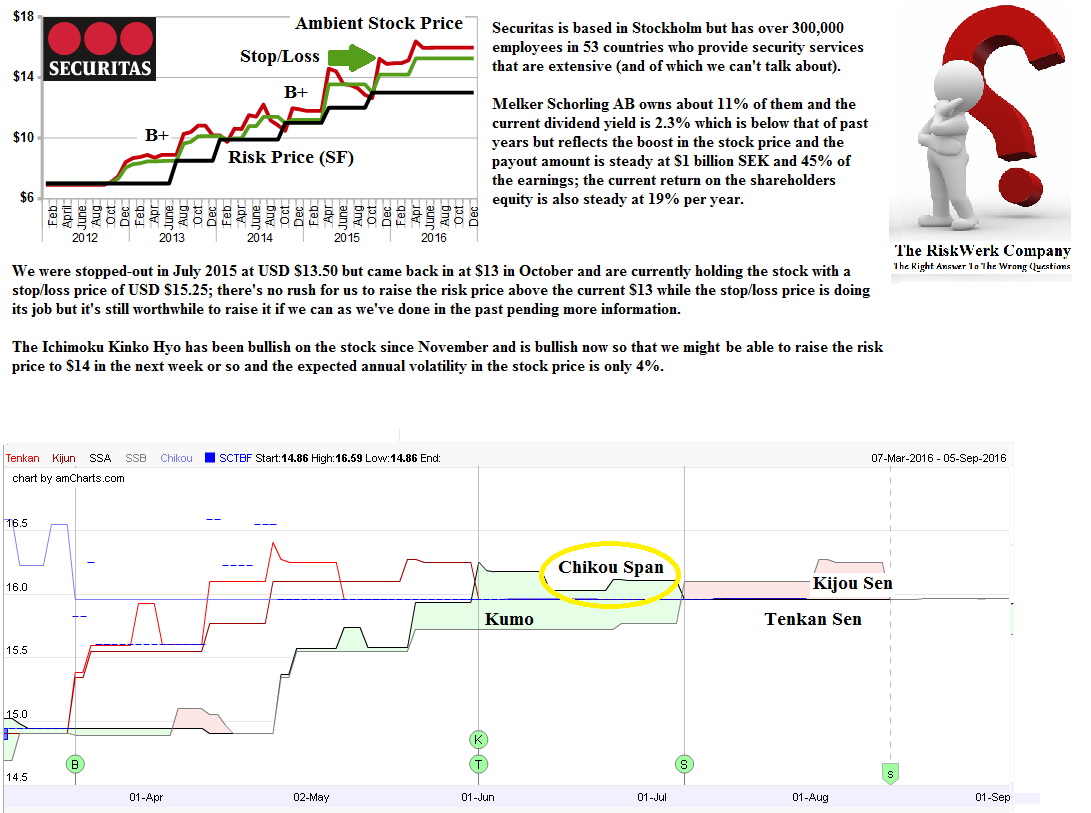

Figure 2.6: SCTBF Securitas AB Class B ADR (B+) |

There are two well-known and popular books which explain why volatility is not an investment risk and why their authors don’t know anything about investing: please see J.J. Siegel, Stocks for the Long Run, 1994, and Burton G. Malkiel, A Random Walk Down Wall Street, 1973.

For more examples of the (B)-class portfolio in difficult markets, please see our recent Posts on”The “W” Syndrome“, Steel, Green Energy and The Coal War; and the Canadian Mines have also taken-off – please see our recent Post “(B)(N) Extreme Economics – The (New) Canadian Mines” for a heads-up on that.

And for more information and examples of the Free Market Yield and the terms that we have used above, please see our Posts “(P&I) The Dismal Equation (Ecclesiastes 9:1)” and “(B)(N) S&P 100 Volatility Risk and The Full Moon” and “(B)(N) NASDAQ 100 Volatility and The Stone Bunnies“ and for an introduction to The Barometer “(B)(N) What’s A Girl To Do” or “(P&I) The Swiss Franc Debacle“.

And for more information on real “risk management” in modern times and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary and “(P&I) Dividend Risk and Dividend Yield“, and our recent Posts “(P&I) The Profit Box” and “(P&I) The Process – In The Beginning“; and we’ve also profiled hundreds of companies in these Posts and the Search Box (upper right) might help you to find what you’re looking for, such as “(B)(N) TLM Talisman Energy Incorporated” or “(B)(N) ATHN AthenaHealth Incorporated” or “(B)(N) PETM PetSmart Incorporated“, to name just a few.

And for more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice. And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

And for more on what risk averse investing has done for us this year, please see our recent Posts on “(P&I) The Easy (EC) Theory of the Capital Markets” or “(B)(N) The Easy (EC) Theory of the S&P 500“, and the past, The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”). The Canada Pension Bond®™, The Medina Bond®™, The Barometer®™, the Free Market Yield®™ and Extreme Economics®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.