(B)(N) FCX Freeport-McMoRan and The Big Shorts

Figure 1: The Big Shorts

Drama. Investing is a hard-scrabble business and the market is rife with the “Play Boys” on Wall Street who are “managing” a lot of our money and trade on fear – they have a good story but no theory and can’t wait for, or don’t want, or don’t expect the earnings to come in (24/7 Wall Street, March 10, 2016, The 5 Most Shorted NYSE Stocks: Chesapeake Energy Leads the Trend) and so create their own at our expense; please see Figure 1 on the right for the low down on shorts.

But there are many who have been long when they should have been short (VRX Valeant Pharmaceuticals) and others who were short when they should been long (HLF Herbalife Limited) and most of the “excitement” now is in the energy and resources stocks with investors who are trying to get in early and at the bottom of a long bull market that ended in 2014 and has left them with a sense of awe not rivaled since God created the Grand Canyon. And they missed that too.

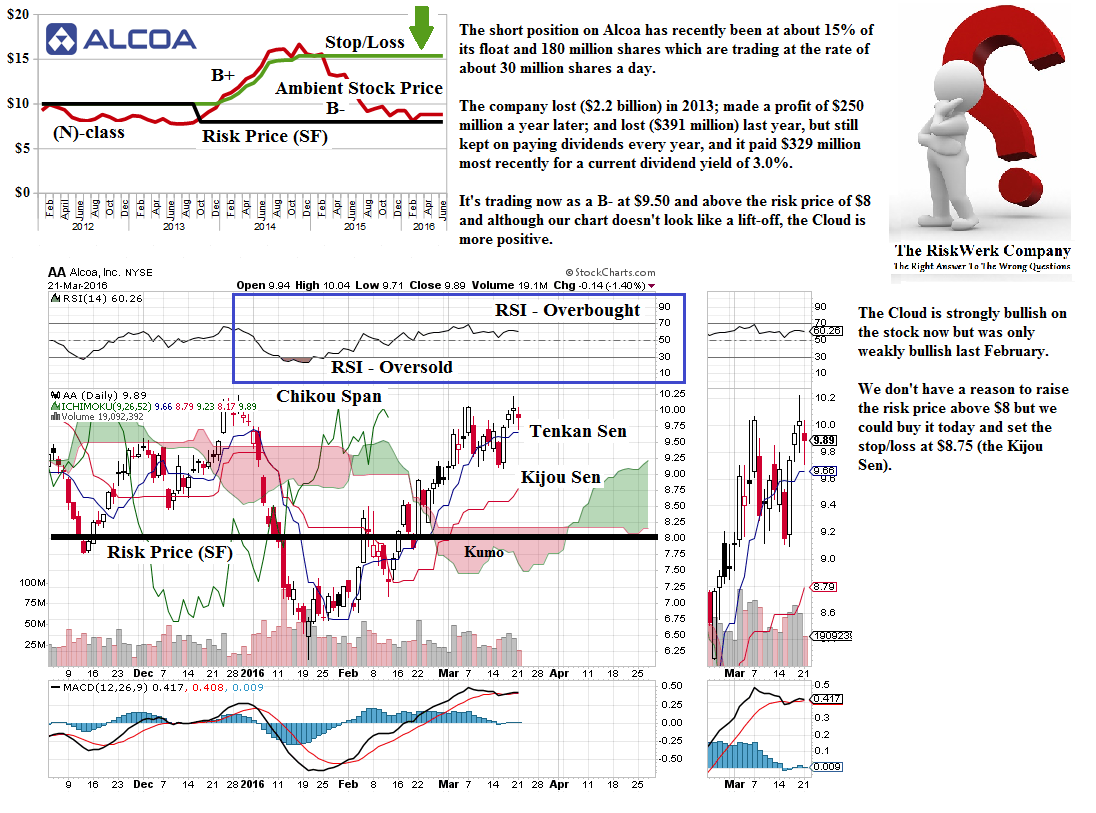

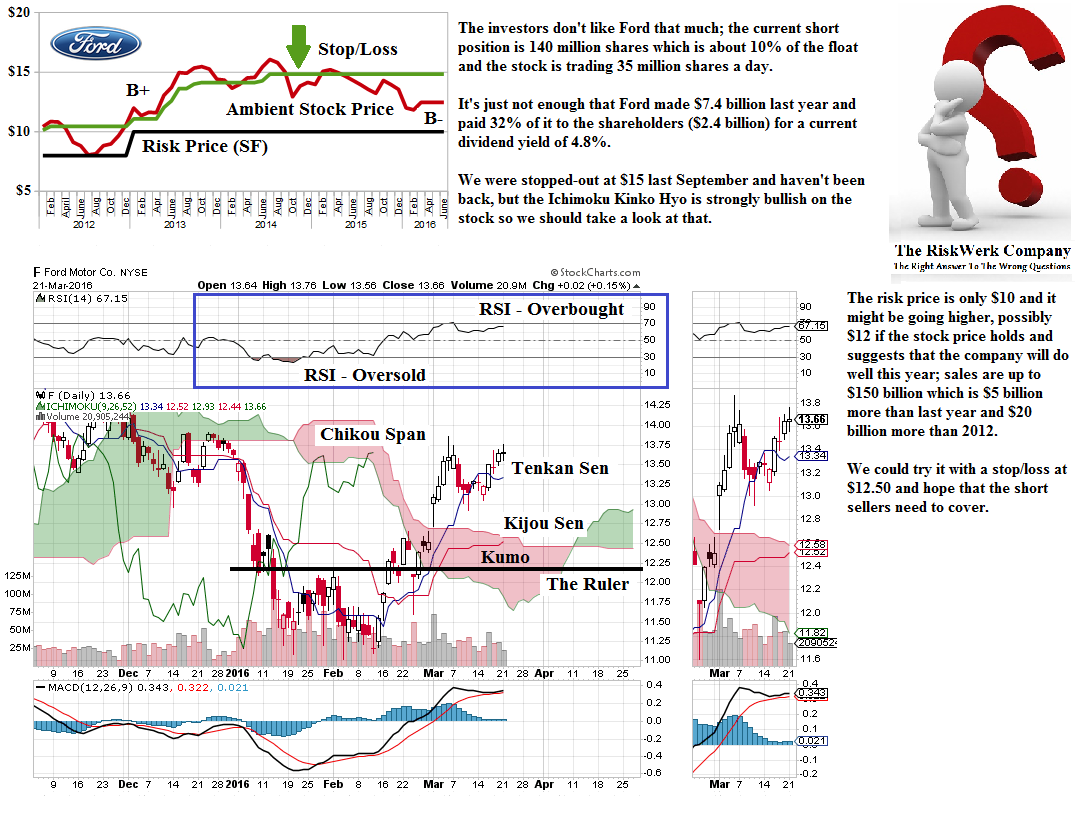

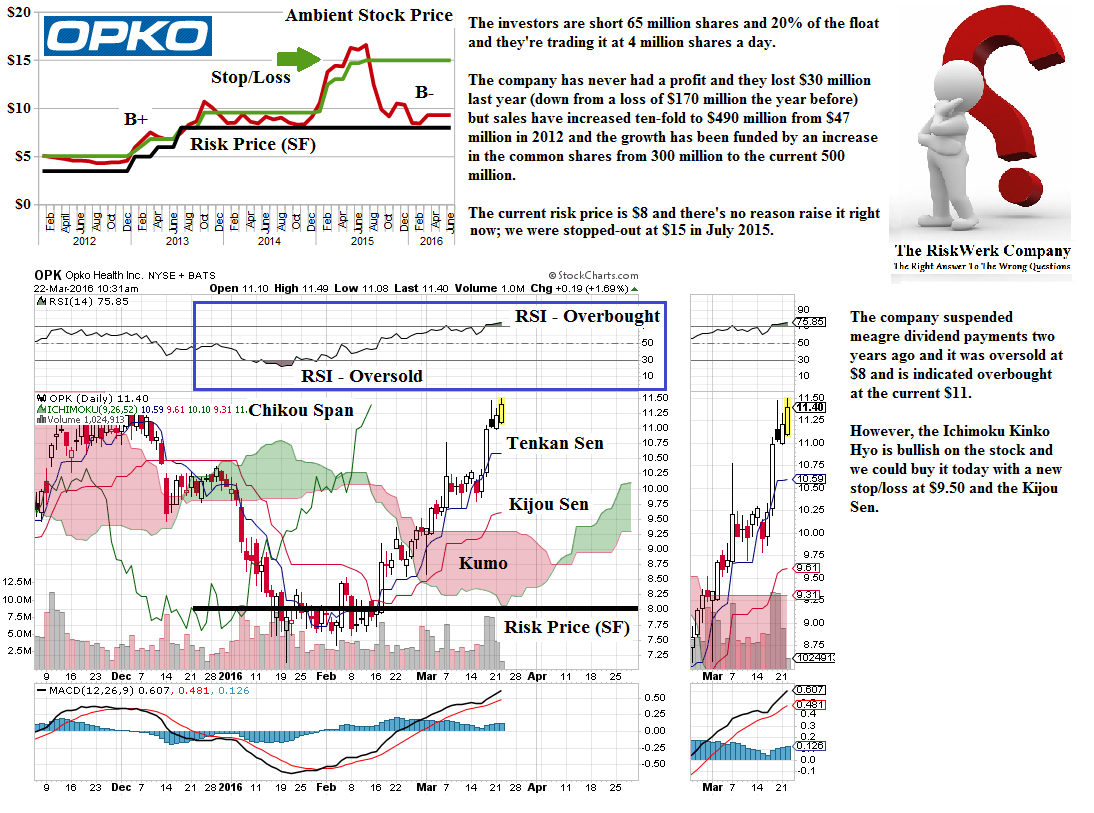

And these short positions are not small and vary between 20% and 40% of the float and even more in some cases (WSJ Short Interest) and the daily activity suggests that they’re playing against us and waiting for us to sell out of companies like Alcoa, Ford, General Electric, Pfizer, Sprint Nextel, and many more (please see below) and make their dreams come true.

But what about our dreams? Are we ready to go long while they scramble for cover?

The Big Shorts

The short positions in the twenty-seven companies of The Big Shorts vary between a significant portion (or percentage) of their total shares outstanding, or they number in the hundreds of millions of shares in some of the bigger companies such as Alcoa, Ford, or Sprint; these shares are owned by somebody but have been borrowed, rented, and sold, by the short sellers who hope to buy them back at a lower price before the owners want them back. Oh well.

Figure 2: Earnings

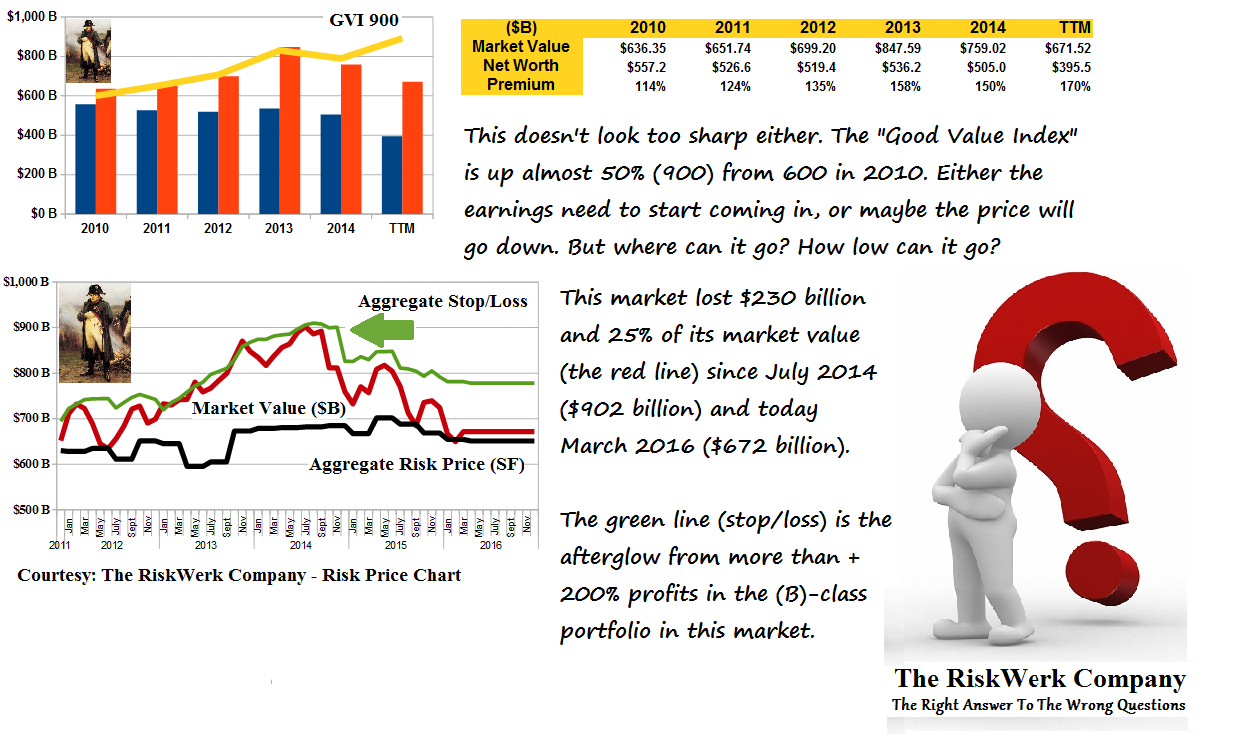

In aggregate, these companies lost almost four times as much ($61 billion) as they earned ($16 billion) last year, but will they do that again this year? Please see Figure 2 on the right (and click on it and again to make it larger as required).

We don’t know but most investors are focused on the companies that are in the market. Are they good companies? Is the management good? Is their product good? Do they have customers?

Which makes sense but that’s not really where the action is; the “action” is in the market itself – like a grocery store with stocks on the shelf – which currently values these companies at $672 billion which is almost 70% more than their net worth ($396 billion) and the real question is how “good” are they – that is, how “good” are the investors? And the answer is “they’re not very good”.

Figure 3: The Good Value Index

For example, would you pay $1.70 for $1 if you didn’t think that was a good “investment” – that you would get your money back and maybe even more? But that price is also 20% more now than they paid for it in 2014 and 50% more than they paid in 2011 despite the short sellers; please see Figure 3 on the right.

The reason that investors are still holding these assets at “high prices” (however low they might appear) is that this economy of these companies and their investors is a “deflationary economy” with a current Free Market Yield of only 0.122% (12 basis points) and, therefore, the price of an income in this market is “high” (very high) and if the investors could find cheaper prices for an income in a more inflationary economy, they would buy those.

And there are lots of them in our World Trade Portfolio but how much money do we really want to make?

We ran these companies as a (B)-class portfolio since 2012 and the total investment return over four years (52 months since January 2012) was +213% in dividends and capital gains and so we tripled our money at the rate of about 30% per year and we can’t do any worse than that at the stop/loss prices; our problem now is what to do with all that cash because there are only three survivors at the present time (CalMaine Foods, General Electric, and (behold) the JC Penney Company).

Please see Exhibit 1 below for the Cash Flow Summary of this portfolio and more detail on the highlights above; because of the “extreme delicacy” of this “situation”, we’ve looked at some of our current buy/hold or not decisions in Exhibit 2 using our usual “stock price charts, a ruler, and a good eye” and please see Exhibit 1 below for more detail on the theory and practice of today’s “special case” of FCX Freeport-McMoRan Incorporated which we last looked at in 2012.

Exhibit 1: The Big Shorts – Fundamentals & Cash Flow Summary

Exhibit 2: The Big Shorts – A Stock Price Chart, a Ruler, and a Good Eye

Figure 2.1: CALM CalMaine Foods Incorporated (B+) |

Figure 2.2: GE General Electric Company (B+) |

Figure 2.3: JCP JC Penney Company Incorporated (B+) |

Figure 2.4: AA Alcoa Incorporated (B-) |

Figure 2.5: ATHN Athenahealth Incorporated (B-) |

Figure 2.6: F Ford Motor Company (B-) |

Figure 2.7: GPRO GoPro Incorporated (B-) |

Figure 2.8: OPK Opko Health Incorporated (B-) |

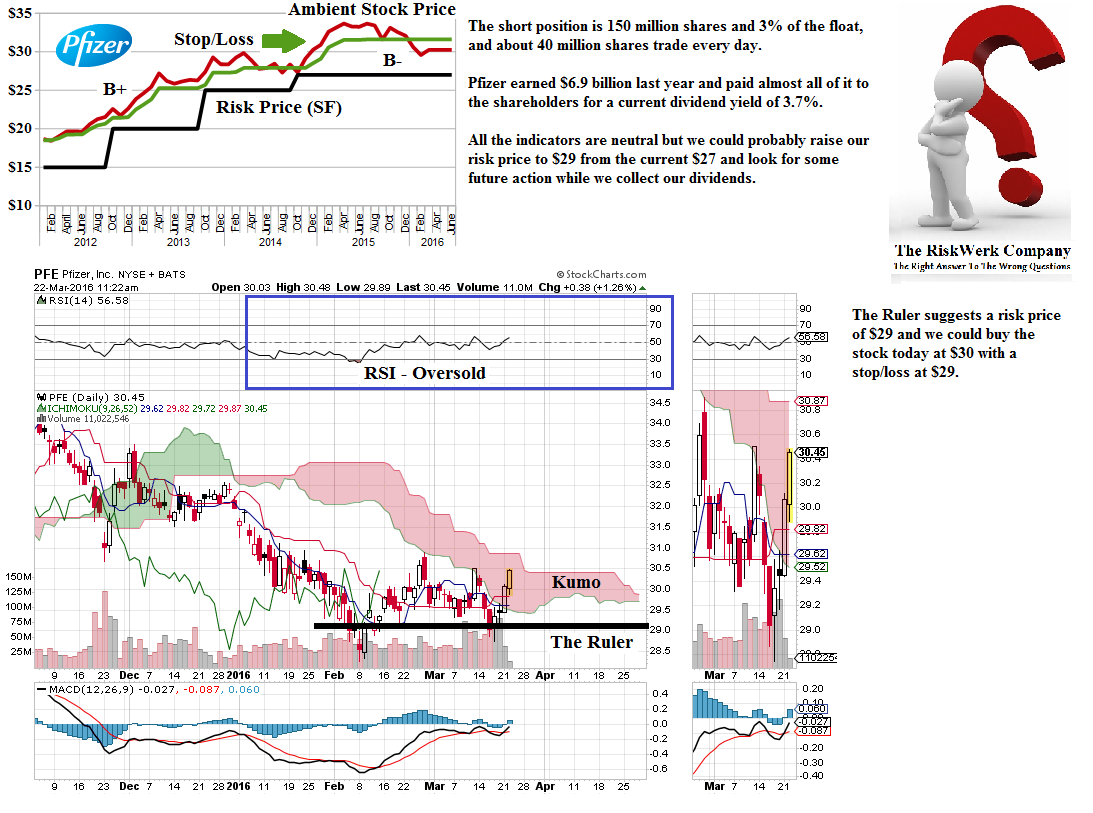

Figure 2.9: PFE Pfizer Incorporated (B-) |

Figure 2.10: TCK Teck Resources Limited (B-) |

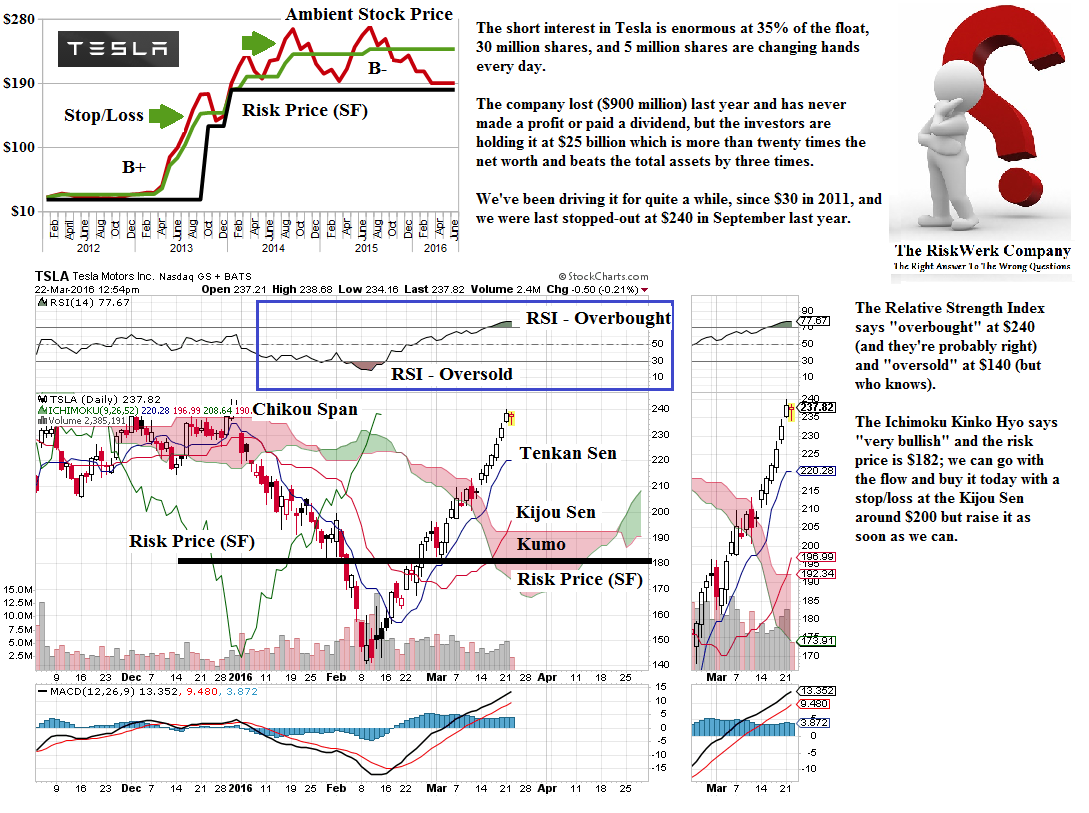

Figure 2.11: TSLA Tesla Motors Incorporated (B-) |

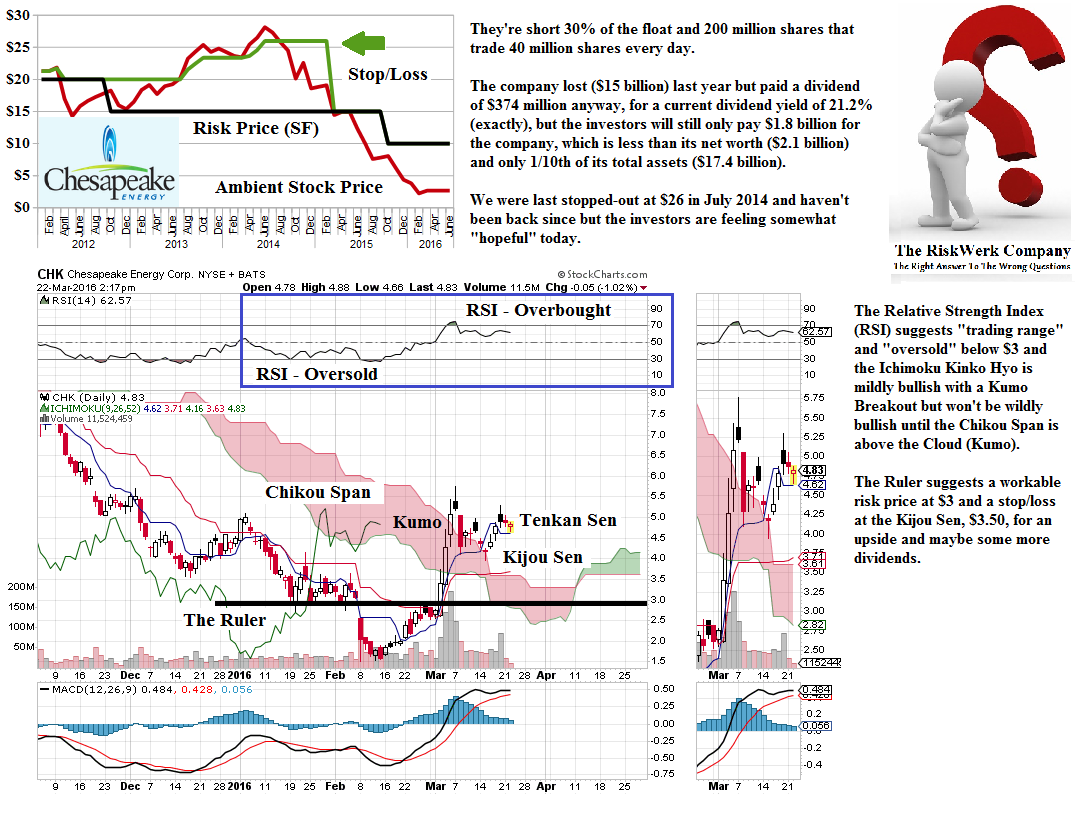

Figure 2.12: CHK Chesapeake Energy Corporation (N) |

Figure 2.13: CNX Consol Energy Incorporated (N) |

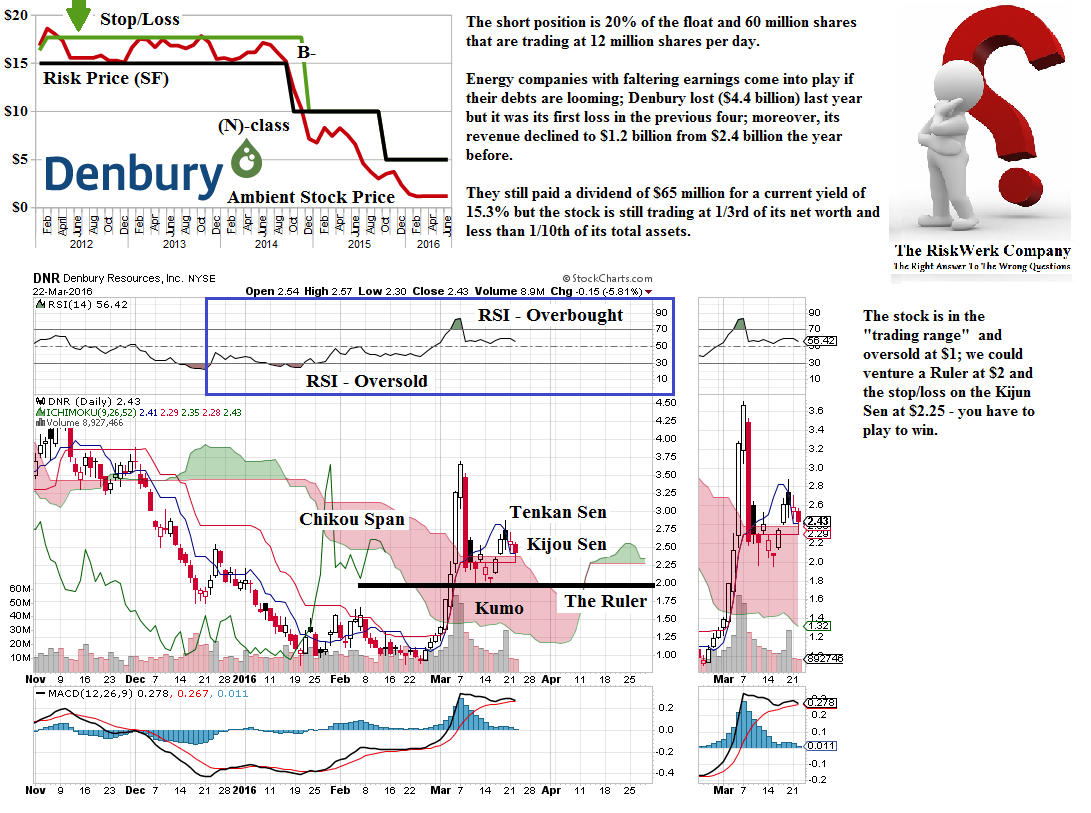

Figure 2.14: DNR Denbury Resources Incorporated (N) |

Figure 2.15: FCX Freeport-McMoRan Incorporated (N) |

Figure 2.16: GME GameStop Corporation Class A (N) |

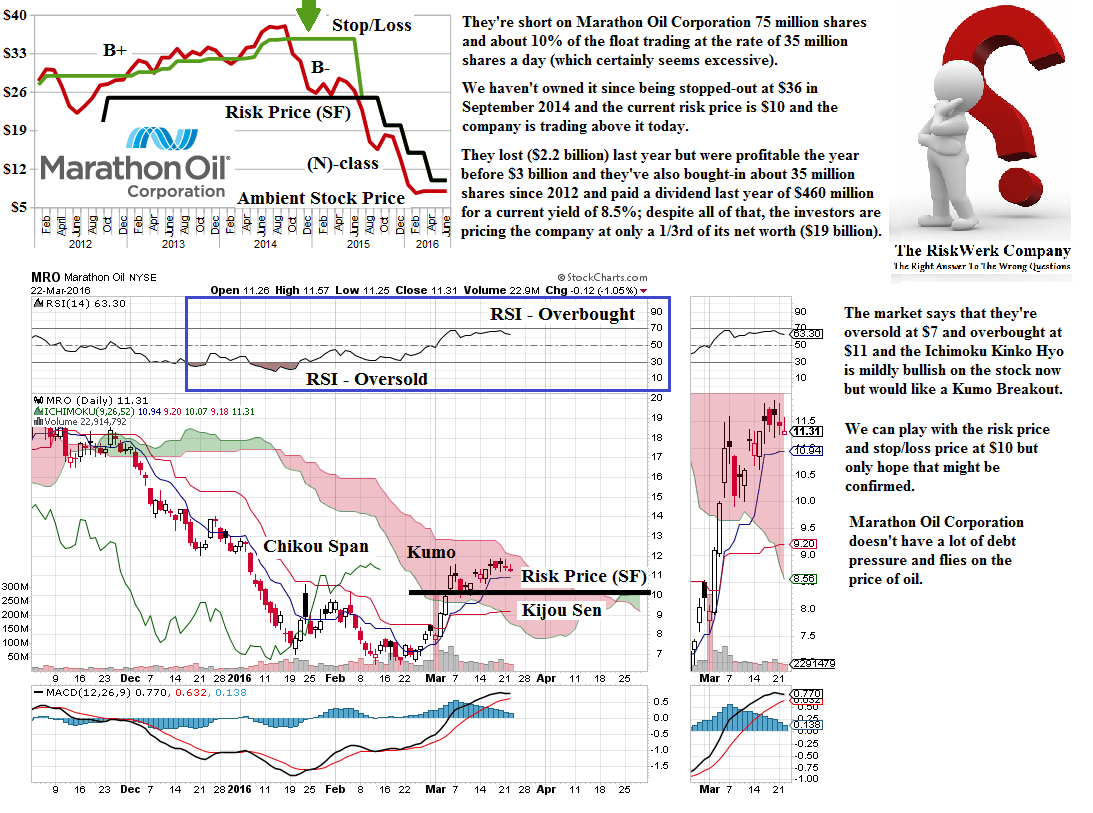

Figure 2.17 MRO Marathon Oil Corporation (N) |

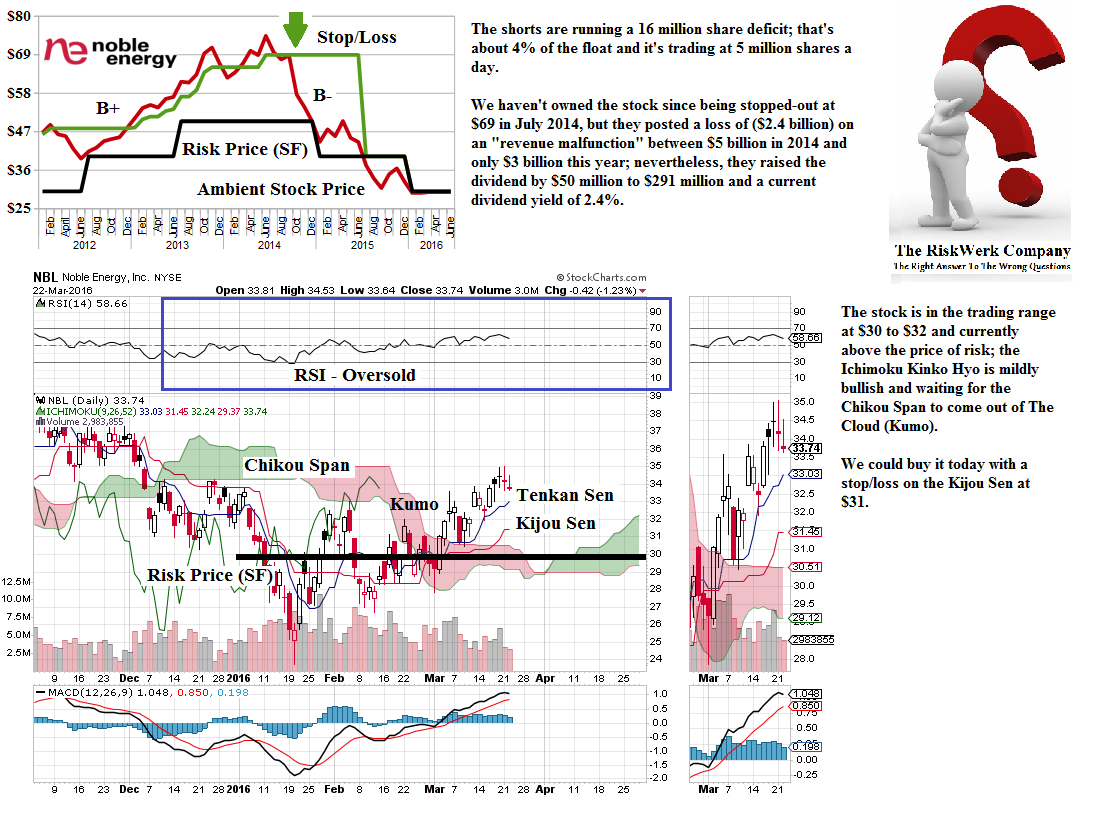

Figure 2.18: NBL Noble Energy Incorporated (N) |

Figure 2.19: PBR Petroleo Brasiliero SA Petrobas ADR (N) |

Figure 2.20: RH Restoration Hardware Holdings Incorporated (N) |

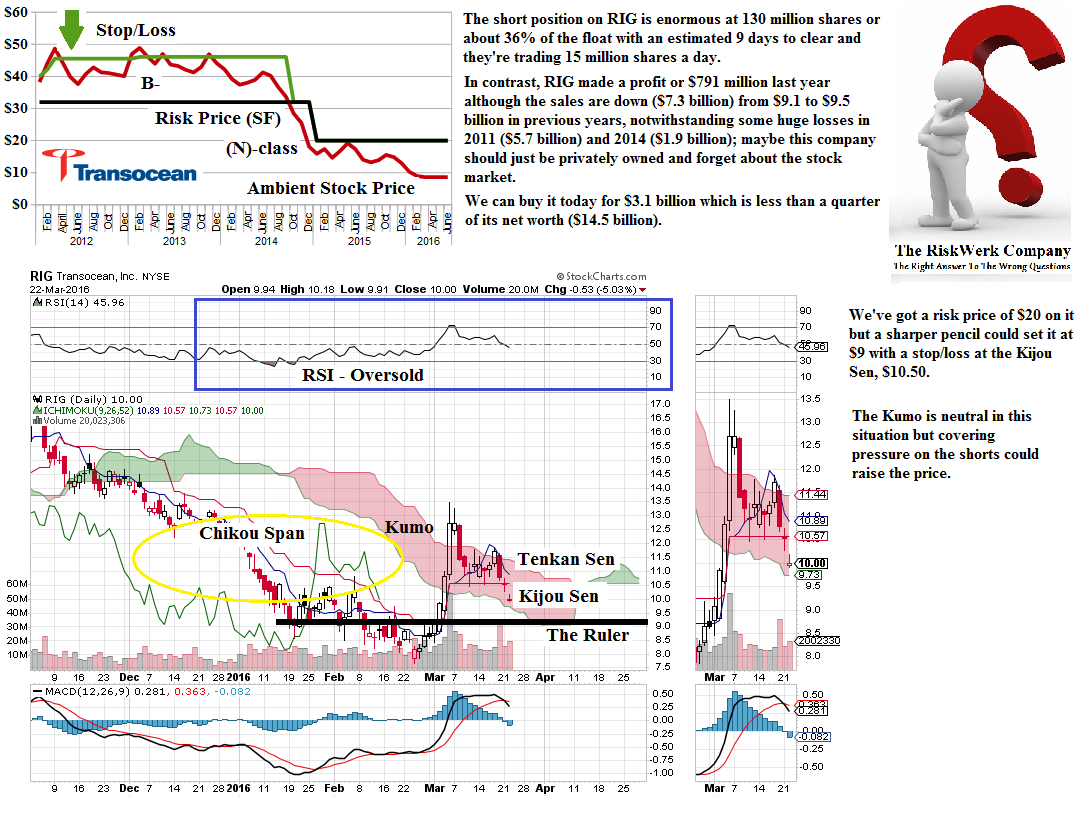

Figure 2.21: RIG Transocean Incorporated (N) |

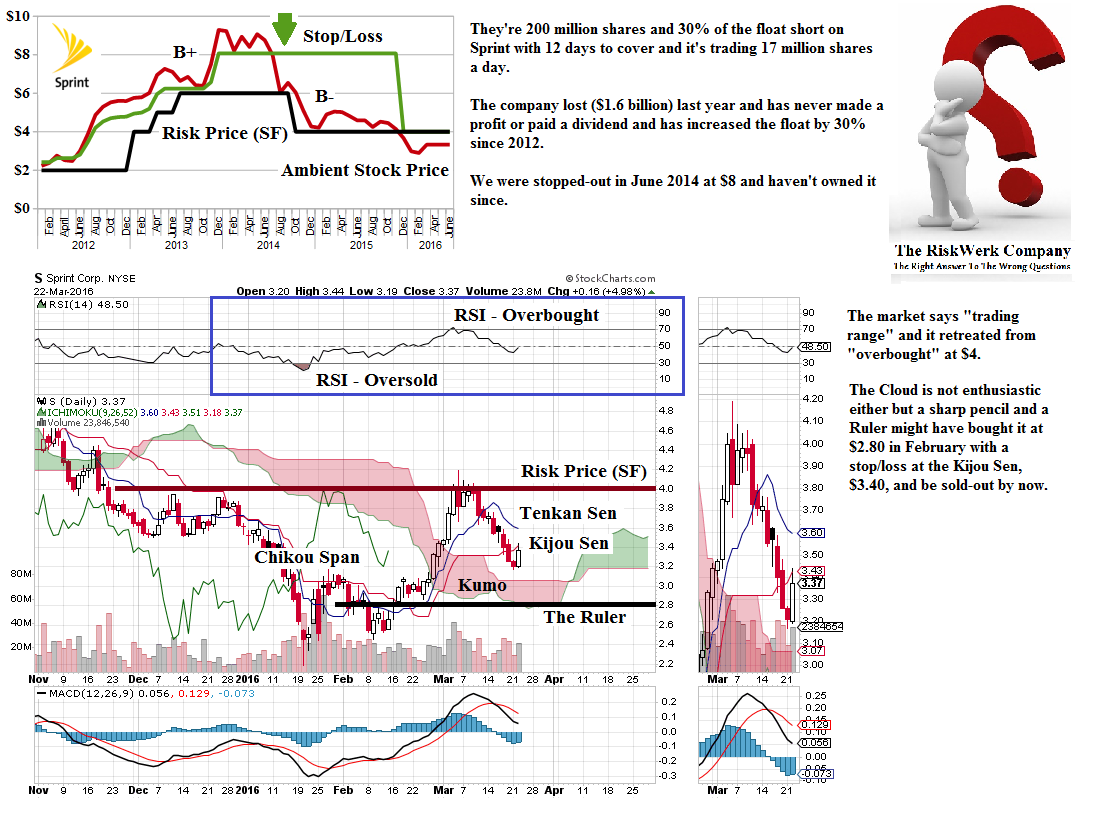

Figure 2.22: S Sprint Nextel (N) |

Figure 2.23: SCTY SolarCity Corporation (N) |

Figure 2.24: SDRL Seadrill Limited (N) |

Figure 2.25: SUNE SunEdison Incorporated (N) |

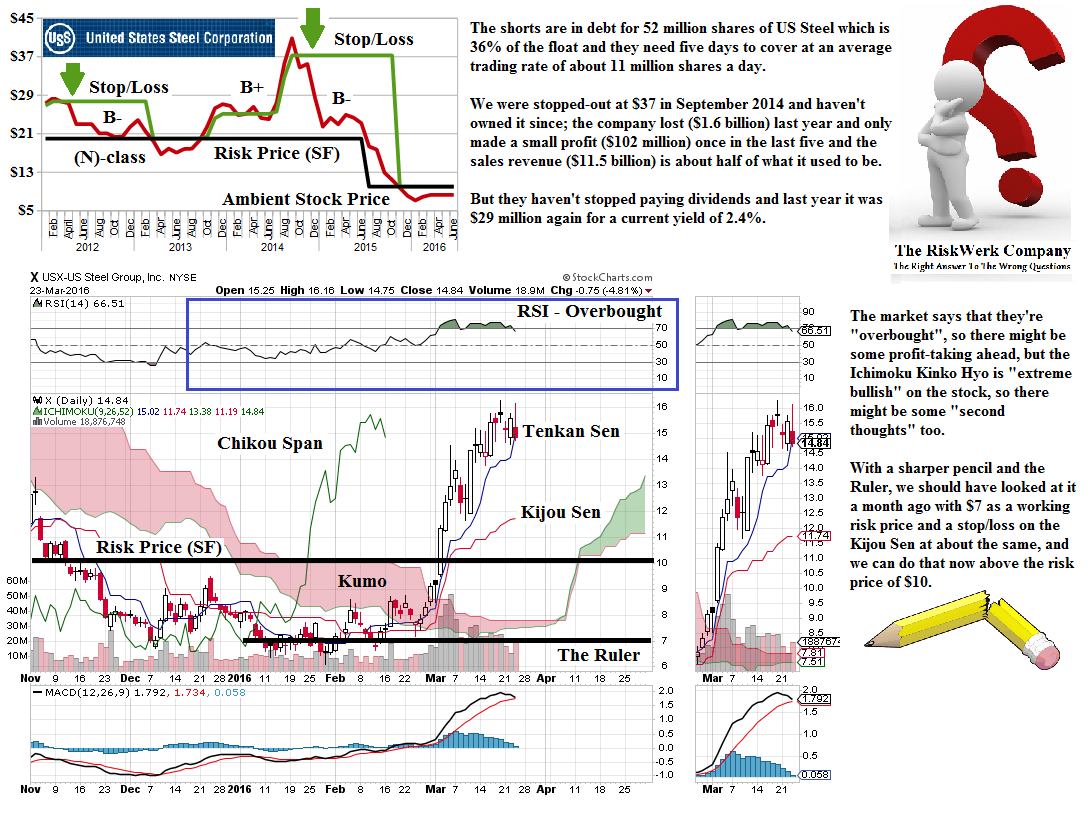

Figure 2.26: X US Steel Group Incorporated (N) |

Figure 2.27: ZG Zillow Group Incorporated Class A (N) |

For more information and examples of the Free Market Yield and the terms that we have used above, please see our Posts “(P&I) The Dismal Equation (Ecclesiastes 9:1)” and “(B)(N) S&P 100 Volatility Risk and The Full Moon” and “(B)(N) NASDAQ 100 Volatility and The Stone Bunnies“ and for an introduction to The Barometer “(B)(N) What’s A Girl To Do” or “(P&I) The Swiss Franc Debacle“.

And for more information on real “risk management” in modern times and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary and “(P&I) Dividend Risk and Dividend Yield“, and our recent Posts “(P&I) The Profit Box” and “(P&I) The Process – In The Beginning“; and we’ve also profiled hundreds of companies in these Posts and the Search Box (upper right) might help you to find what you’re looking for, such as “(B)(N) TLM Talisman Energy Incorporated” or “(B)(N) ATHN AthenaHealth Incorporated” or “(B)(N) PETM PetSmart Incorporated“, to name just a few.

And for more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice. And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

And for more on what risk averse investing has done for us this year, please see our recent Posts on “(P&I) The Easy (EC) Theory of the Capital Markets” or “(B)(N) The Easy (EC) Theory of the S&P 500“, and the past, The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”). The Canada Pension Bond®™, The Medina Bond®™, The Barometer®™, the Free Market Yield®™ and Extreme Economics®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.