(B)(N) VRX Valeant Pharmaceuticals International Incorporated

Will Lip Gloss Be Enough?

Deal Book. Valeant Pharmaceuticals is a pharma-marketing firm that has grown inorganically by buying other pharma firms and there’s no reason for us to buy the stock other than to make some money from other investors who are willing to bid-up the price even though the company doesn’t pay a dividend and doesn’t make any money if we factor-in the losses of the last several years (Reuters, March 9 2015, Ackman’s Pershing Square makes $3.3 billion bet on Canada’s Valeant).

Perhaps the future is brighter but it does arrive and we tend to think of the company as an aging roué in need of ever more makeup, money, and lip-gloss; but such is the world and as investors, we need to be in it; please see Exhibit 1 below.

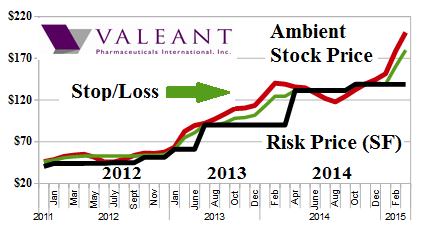

Exhibit 1: (B)(N) VRX (US) Valeant Pharmaceuticals International Incorporated – Risk Price Chart

Figure 1.1: VRX Valeant Pharmaceuticals International Incorporated

Day-to-day stock prices are not important to us because they could be anything on any day (the Tao of Stock Prices).

For us, the only important elements are the relationships between the ambient stock price (red line), the stop/loss (green line), and the price of risk (black line).

Our last outing with Valeant was in 2013 between $64 in January 2013 and $131 in June 2014, more than a year later, when the company breached our stop/loss at $131 and then dropped below the price of risk which was also $131 at that time and its “image” fell into disarray with the Allergan fiasco in 2014 after the Actavis fiasco in 2013; who knows what they will do this year, the year is still young.

We bought it again at US$140 in December 2014 and are currently holding it at $201 with our stop/loss at $180; long-dated options for next year are expensive but we bought the July put at $190 for $13 per share in the event that the bloom really does come off the rose in the next few months and we can also sell the options; as a result, we’re $50 to the good today and can book a +30% profit already that nobody can take away from us no matter what the stock price; if the stock price increases, we’ll raise our stop/loss and possibly traffic our put forward and upwards.

We only buy and hold stocks that appear to be trading at or above their price of risk which resolves a Nash Equilibrium between “risk seeking” and “risk averse” investors with the primary difference between them being the need for liquidity, and that’s certainly a factor in this case because the stock is substantially owned by only a few investment and hedge fund firms.

For any investor, the “price of risk” is always the purchase price but if it can’t be effectively defended with a cheap stop/loss or long-dated put, then they’ve bought a stock that is trading in the (N)-class of investor uncertainty and volatility and the price of risk is higher – which could be an expensive discovery, and as we’ve noted above, we have had no reason to raise the risk price, only the stop/loss.

For any investor, the “price of risk” is always the purchase price but if it can’t be effectively defended with a cheap stop/loss or long-dated put, then they’ve bought a stock that is trading in the (N)-class of investor uncertainty and volatility and the price of risk is higher – which could be an expensive discovery, and as we’ve noted above, we have had no reason to raise the risk price, only the stop/loss.

For more information on “big market” investing, please see our Posts “(P&I) The Dismal Equation (Ecclesiastes 9:1)” and “(B)(N) S&P 100 Volatility Risk and The Full Moon” and “(B)(N) NASDAQ 100 Volatility and The Stone Bunnies“.

And for more information on real “risk management” in modern times and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary and “(P&I) Dividend Risk and Dividend Yield“, and our recent Posts “(P&I) The Profit Box” and “(P&I) The Process – In The Beginning“; and we’ve also profiled hundreds of companies in these Posts and the Search Box (upper right) might help you to find what you’re looking for, such as “(B)(N) TLM Talisman Energy Incorporated” or “(B)(N) ATHN AthenaHealth Incorporated” or “(B)(N) PETM PetSmart Incorporated“, to name just a few.

And for more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice. And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

And for more on what risk averse investing has done for us this year, please see our recent Posts on “(P&I) The Easy (EC) Theory of the Capital Markets” or “(B)(N) The Easy (EC) Theory of the S&P 500“, and the past, The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.