(B)(N) The Great Rotation & Twenty Hot Canadians

Figure 1: Big Deals in 2015

Drama. The Great Rotation has acquired a new twist in 2015 that weighs large in corporate ballrooms all over the World; it’s usually thought of as a movement of investor funds from “risky” equities at high prices into “safe” government and corporate bonds with higher yields (the old 60/40 and 40/60 “prudence” game for the old folks), but there aren’t enough of the those bonds and certainly nothing like the high single digit or double digit interest rates (and inflation) of the 80’s absent Brazil, Argentina, Venezuela, or the Congo anyone?

And so last year was a record year for deals and even as the global stock markets faltered and returned net nothing for all their trouble, bespoke investors (banks, insurance companies, pension funds, sovereign wealth, and Berkshire Hathaway and a few others) pumped $5.1 trillion into funding the mostly all cash deals for Pfizer and Allergan, AB InBev and SABMiller, Royal Dutch Shell and BG Group, Dell and EMC, Dow Chemical and DuPont, Heinz and Kraft Foods, Anthem and Cigna, Aetna and Humana, EBay and PayPal, and Teva and Allergan Generics (to name just a few) – and all of those companies borrowed our money at low rates (very low rates) and bought their competition in their slow-growth markets (The Wall Street Journal, December 21, 2015, Year in Review: Mergers Set a Record as Firms Bulk Up); please see the illustration on the above right.

But those deals are only the headline deals and account for only $700 billion of the total $5.1 trillion that’s now earning interest at about 3% for the next twenty years or so (current US government bonds are 3% for 30 years and only 1.25% real return) and in order for the principle investors to earn an income, they will need to re-package (securitize) and re-sell that debt at retail many times over just to keep up with inflation and global growth over which they have no control; moreover, those deals seem to have stressed their budgets and their attention span because more modest and accessible IPOs and new entries in the equity markets are down 16% last year from 2014 and even more from 2013 (The Wall Street Journal, October 14, 2015, Weak Pricing, Pulled Deals: IPOs in 2015).

Figure 2: The Great Rotation

And after all, $5.1 trillion is also the current market value of the thirty Dow Jones Industrial Companies and they earned $264 billion last year and paid-out 54% of it to the shareholders for a current dividend yield of 2.8% and will probably do it again this year and M&A has a lot to do with how they got into the Dow but these companies also employ millions of people and $5.1 trillion exceeds the budget of the US government ($3.8 trillion) and imagine what would happen if they had no money to spend because it was all tied-up in Brazilian bonds or something.

And as a result, investors are buying into 3% corporate bonds and the prices of older bonds at less than 3% in the secondary markets will plunge to make up the difference as liquidity requirements kick-in and they need to be sold to raise cash to pay the bills and their pensioners.

And as a result, the equity markets are “floating” and they will continue to float in 2016 and maybe 2017 and maybe beyond until there’s a real need for our money to finance investment and growth; please see Figure 2 above.

And as a result U.S. retirement assets which totaled $23.5 trillion for the quarter ended September 30, are down 4.3% from the end of the previous quarter, said the Investment Company Institute’s recent quarterly report; how long are they going to do that if 2016 and 2017 looks a lot like 2011 and 2012 and nothing like 2013 is in sight?

The Perpetual Bond

The Great Rotation is also the Great Game and most of us are not a part of it; for example, there is no pension plan in the World that can raise $5.1 trillion in one year but it’s likely that hundreds of them chipped-in a few billion to help with these deals and that in the long term, thousands of investors and pension plans will own a piece of these bonds.

Figure 3: What risk?

But our game is quite different because for us there is no risk in the equity markets but there is always lots of risk in the bond markets because inflation is a government initiative and beyond our control (as are corporations that can’t pay their bills) whereas we can buy and sell equities on the World markets with 100% capital safety and 100% liquidity guaranteed and a hopeful but not necessarily guaranteed return above the rate of inflation (because it’s a government initiative) and we are hopeful as long as companies have earnings and pay dividends and other investors want to buy them or work the market for capital gains creating volatility; please see Figure 3 on the right for how the World is structured according to the demonstrated societal norms of risk aversion and bargaining practice and the reason that volatility is our friend and not an investment risk.

For example, the top three big-cap US stocks gained more than +100% last year and we bought them at much lower prices in 2012 and 2013 because they were trading in the (B)-class and for no other reason and there are currently about 900 companies that are trading in the (B)-class in our World Trade Portfolio but that number is down from about 1200 a year ago and we expect that if the market wanes that more of those will be trading as a B- (below the stop/loss price) and possibly as an (N)-class stock (below the price of risk) and although we’ll have cash earned at high prices, what are we going to buy?

And that’s our problem for today; please see Exhibit 1 below to get started and Exhibit 2 and 3 below for just one of many, many, solutions.

Exhibit 1: The Top Three US Big-cap Stocks

AMZN Amazon Incorporated |

NFLX Netflix Incorporated |

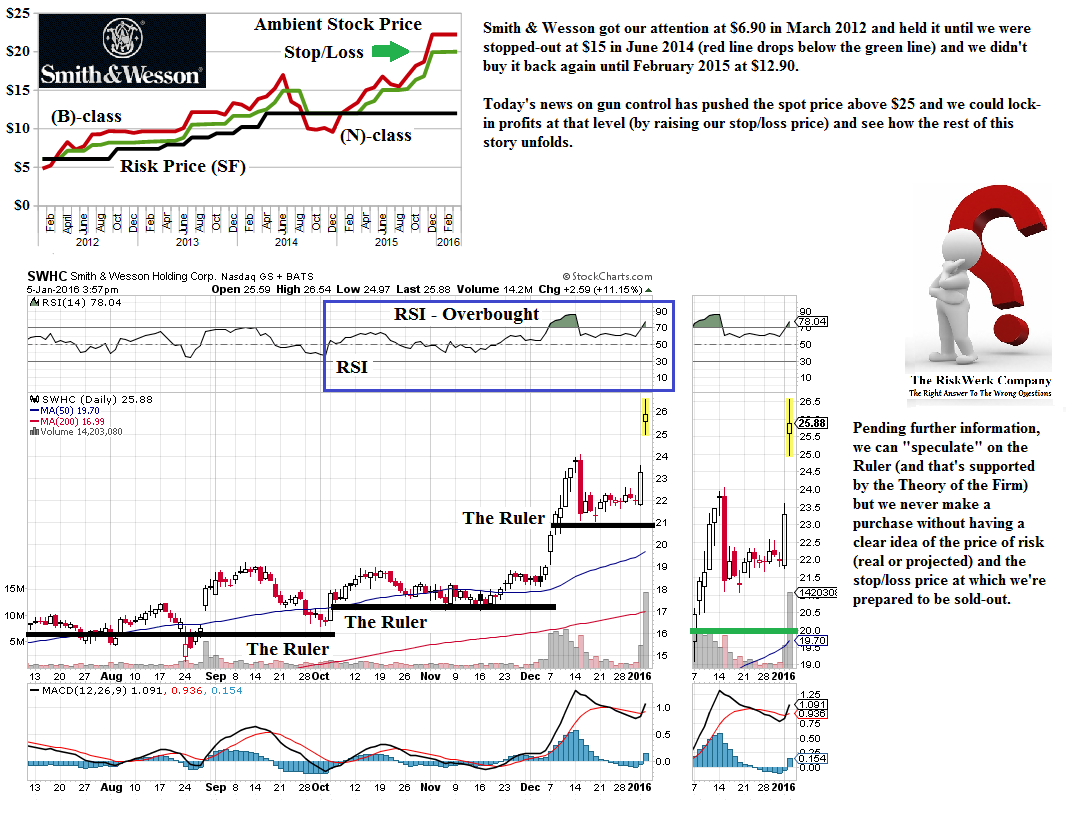

SWHC Smith & Wesson Holding Corporation |

Of course, that’s not all – there are another fifty US companies that gained more than 40% last year and they’re all trading as a B+ or B- and there are still more at +30%; moreover, with patient money, or our profits on the price of risk, we can buy more of the “high priced” companies in the B+ or take a position in the sectors such as the resources that are trading in the (N)-class and collect our dividends until something happens.

A Stock Chart, a Ruler, and a Good Eye

Canadian dollar stocks are cheap in US dollars, Euros, and Yuan and certainly one move for patient money is to take positions in the Canadian resource industries – the mines, woods, and oil & gas – which are mostly trading in the (N)-class and have been for the last several years and that move is equivalent to buying bonds at a steep discount because these companies are paying dividends (even if they have to borrow the money) at high yields pending a possible bankruptcy or reorganization or takeover. Or possibly prosperity.

Risk? What risk?

But to get some patient money not our own, we can work the active market in the (B)-class and re-invest our profits as we can afford them.

And all that we really need is a stock chart, a ruler, and a good eye, and some money to invest; please see Exhibit 2 below for some current examples of the Canadian Hot Stocks in 2015 and we note that these stocks are up +18% since December – one month ago – and our issue now is in keeping our profits, and even more profits, but it’s not in getting them – that’s the easy part; please see Exhibit 3 below for the summary of the (B)-class portfolio in these stocks and how we got here and Exhibit 2 below for how we’re going to stay here this year.

Exhibit 2: Twenty Hot Canadians For The Cold, Cold Market

ADN Acadian Timber Corporation |

AEM Agnico-Eagle Mines Limited

|

ARE Aecon Group Incorporated |

ATD-B Alimentation Couche-Tard Incorporated |

BAA Banro Corporation

|

BAM-A Brookfield Asset Management Incorporated |

BCB Cott Corporation |

CCL-B CCL Industries |

CLS Celestica Incorporated |

CSU Constellation Software Incorporated |

DGC Detour Gold Corporation |

DOL Dollarama Incorporated |

EXE Extendicare Incorporated |

FSV FirstService Corporation |

GIB-A CGI Group |

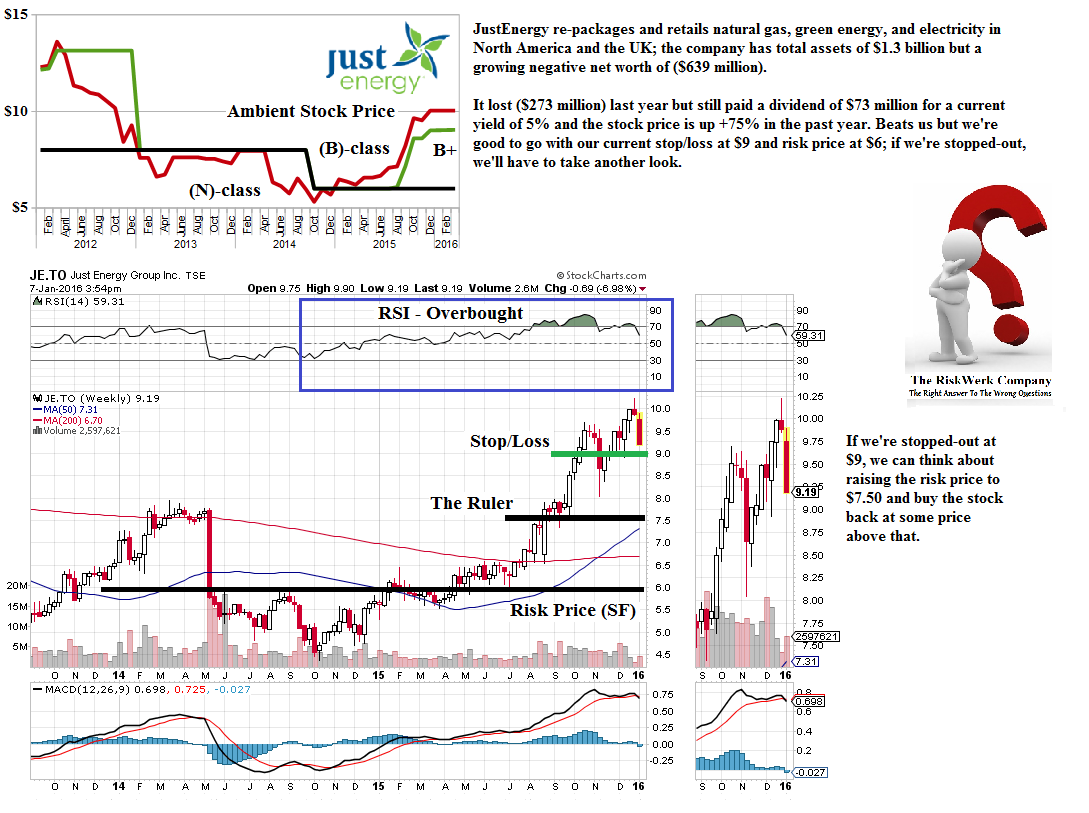

JE JustEnergy Group Incorporated |

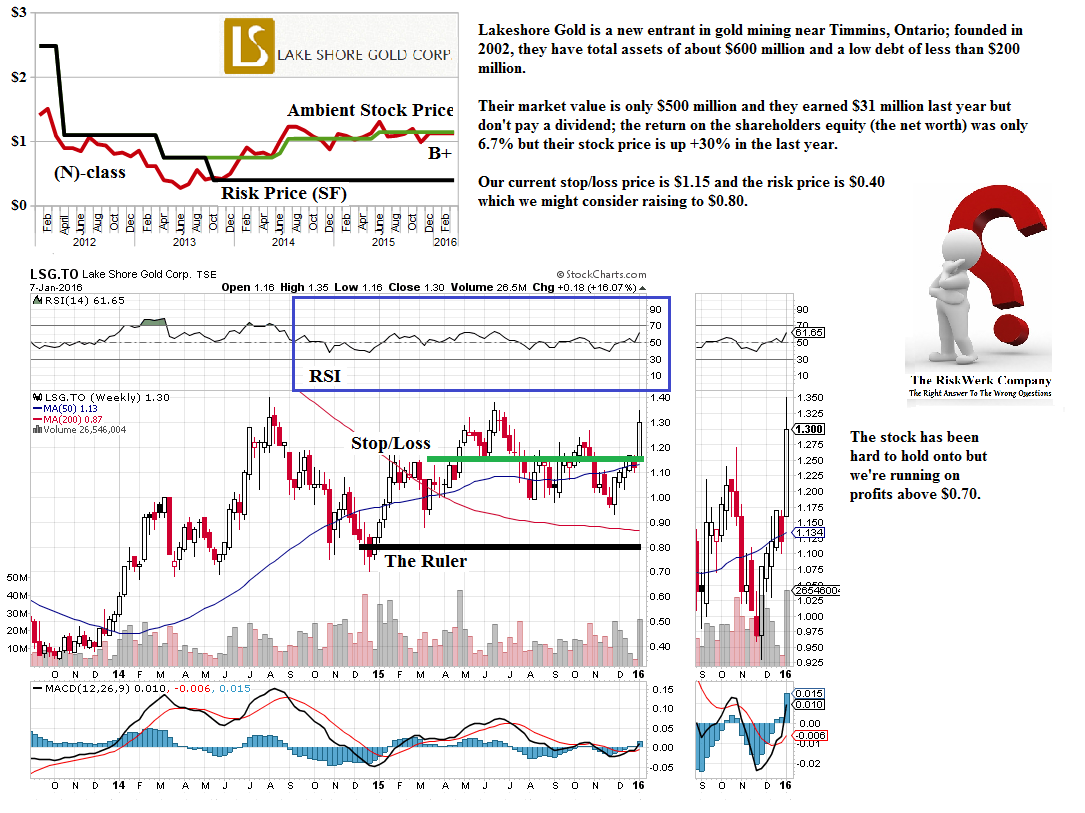

LSG Lake Shore Gold Corporation |

MFI Maple Leaf Foods Incorporated |

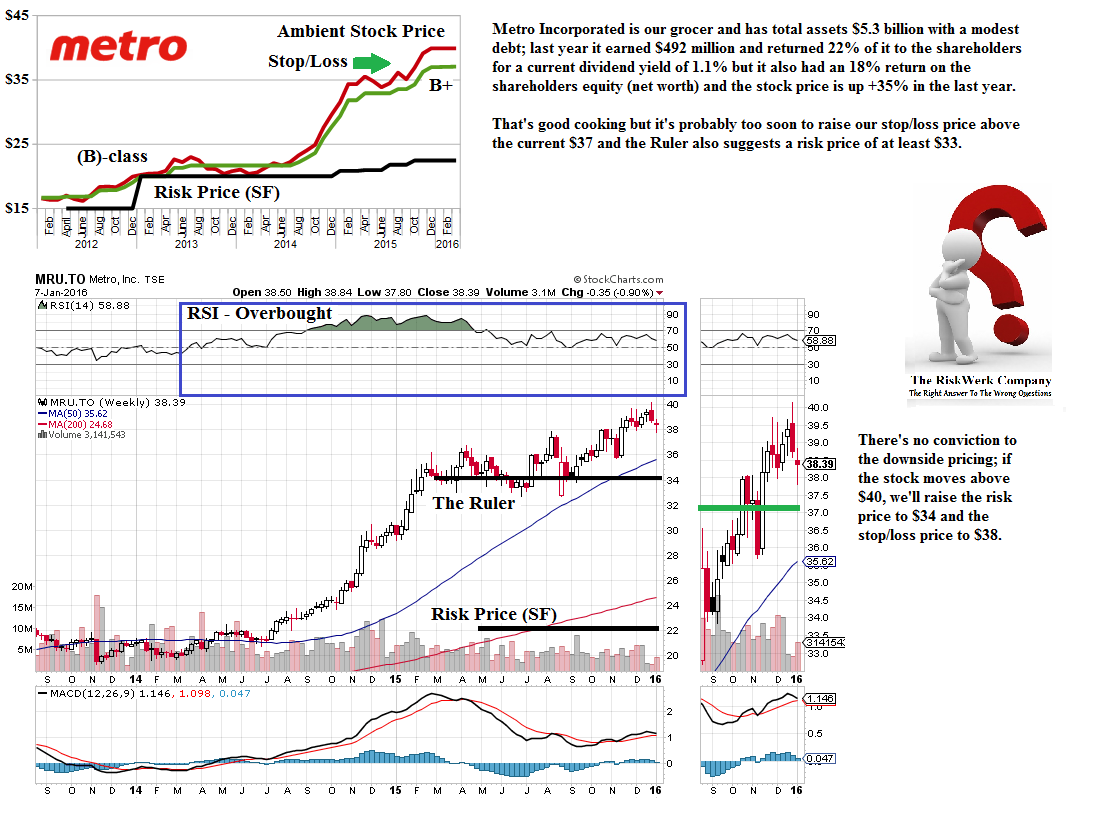

MRU Metro Incorporated |

NG NovaGold Resources Incorporated |

OCX ONEX Corporation |

Exhibit 3: Twenty Hot Canadians – Fundamentals and Cash Flow Summary

Exhibit 1.1: (B)(N) Twenty Hot Canadians – Fundamentals & Cash Flow Summary

For more information on the current Canadian market, please see our Posts “(B)(N) Extreme Economics – A Stock Chart, a Ruler, and a Good Eye” and “(B)(N) Extreme Economics – Plan Zero (Buy Canadian)“.

And for more information and examples of the Free Market Yield and the terms that we have used above, please see our Posts “(P&I) The Dismal Equation (Ecclesiastes 9:1)” and “(B)(N) S&P 100 Volatility Risk and The Full Moon” and “(B)(N) NASDAQ 100 Volatility and The Stone Bunnies“ and for an introduction to The Barometer “(B)(N) What’s A Girl To Do” or “(P&I) The Swiss Franc Debacle“.

And for more information on real “risk management” in modern times and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary and “(P&I) Dividend Risk and Dividend Yield“, and our recent Posts “(P&I) The Profit Box” and “(P&I) The Process – In The Beginning“; and we’ve also profiled hundreds of companies in these Posts and the Search Box (upper right) might help you to find what you’re looking for, such as “(B)(N) TLM Talisman Energy Incorporated” or “(B)(N) ATHN AthenaHealth Incorporated” or “(B)(N) PETM PetSmart Incorporated“, to name just a few.

And for more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice. And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

And for more on what risk averse investing has done for us this year, please see our recent Posts on “(P&I) The Easy (EC) Theory of the Capital Markets” or “(B)(N) The Easy (EC) Theory of the S&P 500“, and the past, The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”). The Canada Pension Bond®™, The Medina Bond®™, The Barometer®™, the Free Market Yield®™ and Extreme Economics®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.