(P&I) Volatility Is Not An Investment Risk

The Hereafter Does Not Solve The Problem Of Our Mortality

Drama. Volatility is not an investment risk – it is just volatility and it has a simple explanation. Moreover, as actuaries, we ought to know that the economics of volatility management and diversification is nothing more than badly applied statistics and does not solve the problem of investment risk any more than the “life hereafter” solves the problem of our mortality.

But what is an investment risk is “illiquidity” – we can’t get our money whole when we need it – and the pension industry has a demonstrated penchant for taming volatility and seeking illiquidity (“constructive illiquidity”) with the net effect that they are proud to report their “paper profits” and hopefully rising “paper assets” but are not accountable for not producing a reliable income, now, and every year hereafter.

In our view, the minimum acceptable return on assets under management – which is the shareholders equity – is 10% per year, every year, in accessible cash and that’s the bottom of the barrel because it’s just the “bankers rate“. In other words, if a pension plan is managing $50 billion for its shareholders, the pensioners and pensioners-to-be, and it can’t distribute in principle $5 billion per year in real terms and do it every year, then it’s just gulling the shareholders and the sponsors and postponing the inevitable for another year.

The Rehearsal, Edgar Degas 1878

21st Century Pension Plan Management – A Rehearsal

The calculation is quite simple and quite mean. A typical pension plan with $50 billion in assets can be expected to have 250,000 members each of whom has a vested interest of $200,000 over thirty years. If the plan can’t spin-off $10,000 to $20,000 in income for each of them, every year, in real terms, now, it’s a failure and that’s the only bar that the plan sponsors need to be concerned with.

Everything else in the art and practice of pension plan management is just a rehearsal and anticipation of the life hereafter.

Volatility Management By Risk Management

Nor do we think that the bar is unreasonable; there are lots of examples, all routine and unremarkable, in these Posts of “ersatz money” – big portfolios of highly liquid stocks which spin-off 30% or so every year in every market and don’t need to change their investment strategy. Which is why we say that volatility is not an investment risk – it is our friend.

To be more precise, we threw together, at random, a portfolio of blue chip big-cap stocks in the S&P 500 with a high investment “beta” in excess of β>1.5 which is typical of consumer cyclicals and resource stocks and the playground of risk-seeking investors but we managed it for risk aversion – we want our money to safe – 100% capital safety – and to obtain a hopeful but not necessarily guaranteed return above the rate of inflation.

Exhibit 1: The Dreamscape Portfolio – Fundamentals – March 2014

The Dreamscape Portfolio – Fundamentals – March 2014

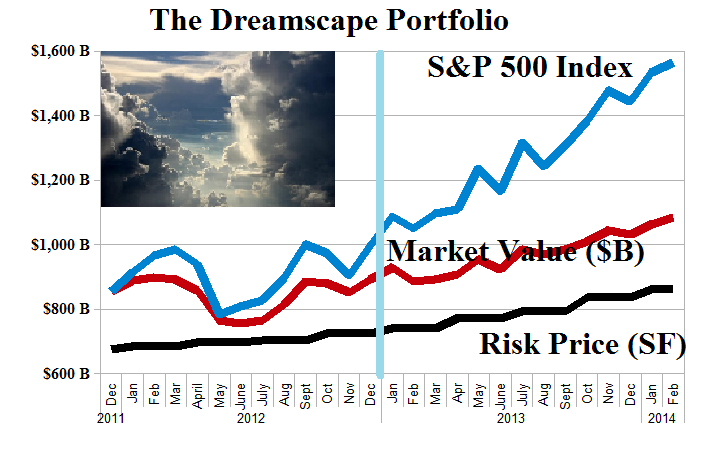

(B)(N) The Dreamscape Portfolio – Risk Price Chart – March 2014

The market capitalization-weighted average beta of this portfolio is β=1.8 but we can see from the Chart on the left that even that doesn’t work out as predicted.

On the other hand, these companies gained $140 billion in market value last year for a gain of +16% and they paid an aggregate $36.7 billion in dividends for an aggregate dividend yield of 3.4% and a 46% return of earnings to the shareholders.

In addition, their return on the shareholders equity was 8.8% and the aggregate [P/E] of 13× and market yield of 7.5% suggests that they are still “undervalued”.

However, they are “undervalued” for another reason and that is that they are, in aggregate, trading above the price of risk, estimated as the Risk Price (SF), and when managed as a Perpetual Bond™, they will always be trading above the price of risk. That portfolio returned +22% last year and is up +8.6% so far this year. Please see Exhibit 2 and 3 below for the details.

To say that a stock is “undervalued” in those terms means exactly that there is a demonstrated excess of demand over supply at these prices, however “high”, and that we can expect to sell large blocks of them without undue downwards pressure on the stock price; and if we propose to buy large blocks, then we will have to deal with the market price and should not expect any “bargains“.

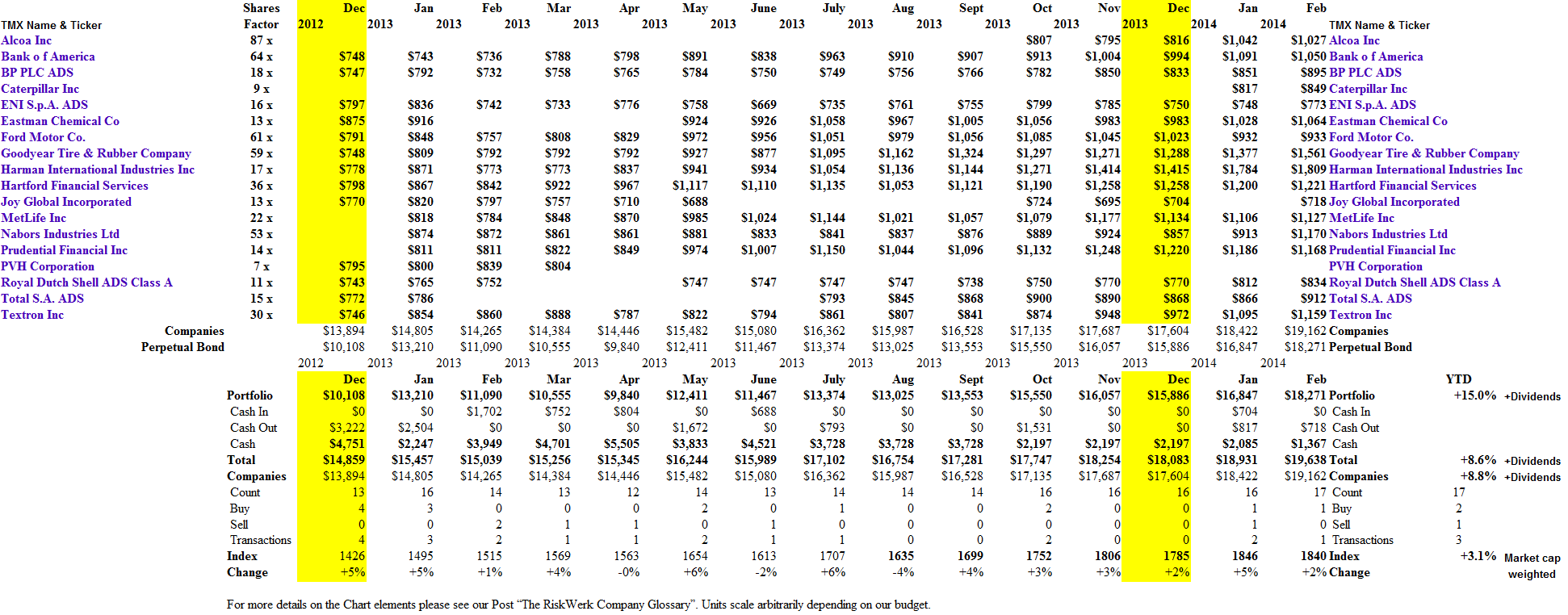

Exhibit 2: (B)(N) The Dreamscape Portfolio – Prices & Portfolio – March 2014

(B)(N) The Dreamscape Portfolio – Prices & Portfolio – March 2014

Exhibit 3: (B)(N) The Dreamscape Portfolio – Portfolio & Cash Flow Summary – March 2014

(B)(N) The Dreamscape Portfolio – Portfolio & Cash Flow Summary – March 2014

(Please Click on the Chart to make it larger and again if required.)

For more information on “risk management” and additional references to the theory, please see our recent Post, The RiskWerk Company Glossary.

And for more on what risk averse investing has done for us this year, please see our recent Posts on The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.