(B)(N) Diamonds In The Rough

Surely, it’s not that easy?

Drama. The industry pundits have given us a kaleidoscope of diamonds in the rough – they say that oil & gas, manufacturing, wineries, online retail, raw materials, and paper are out this year – but watch the marijuana, East coast high-tech, silicon, industrial 3D-printing, solar energy, defense, communications, pharma, and Wall Street (U.S.News & World Report, December 30, 2104, Fifteen Sectors to Watch in 2015).

If that’s true, then the overall market in 2015 will turn out to be like 2012, with nearly no growth for the first nine months, and then a flurry of activity at the end of it, “if” – and we think that it is a very big “if” – if the demand for the producer industries that are being shunned picks-up in 2015 or thereafter.

Nevertheless, this forecast “in the small” is not helpful and unlikely to be factor this year, but we can draw out of it a much bigger picture of the future which has been germinating for the last twenty years or so, in bits and pieces; please see below for “The Brave New World”.

That looks like a lemon?

But before we can do that, we can dispatch with certain aspects of the “little future”, notwithstanding that the forecasters might also be wrong about the industries that they shun and that our best friends are still in the much simpler and reliable industrial and transportation companies of “(B)(N) What’s A Girl To Do?“.

For example, Wall Street is expected to find new ways to exploit our savings and investment dollar, so we’ll pass on that and let the banks fight it out because they are banking for the old ways for which there’s no demand and small conscience (CNBC, December 29, 2014, ‘Shadow banking’ set for breakout year in 2015); pharma is expected to thrive on specialty drugs with names and causes that we can’t pronounce and hope not to need, but that’s an old story in the NASDAQ; and communications is expected to thrive on captive audiences for content providers, but they will need to re-open Pandora’s Box Office and the Roman Circus for an encore.

These industries might animate the investors from time-to-time, and create some “hot spots”, but we can’t predict them, and can deal with them in the usual way as a (B)-class portfolio that benefits from volatility and investor uncertainty.

And so, that leaves us with just six industries on which we might place our random bets – marijuana, East coast high-tech (about 82,500 companies worldwide), silicon, industrial 3D-printing, solar energy, and defense – but because East coast high-tech sees its future in the “cloud, mobility, data and security”, we’ll wait for the IPOs, and focus on just five industries and see what a portfolio of those might do for us.

But we got still more surprises – the only industry that the United States has a clear edge in well-capitalized big-cap companies, is defense, and we have ten of those, including our interests in BAE Systems, Airbus and Finmeccanica.

Made to measure on our 3D-printer

And there are dozens of solar energy and renewable energy companies worldwide, especially in Europe and China, but only about twelve that are listed in the US, and they lost $3 billion last year and have a market capitalization of only $17 billion of which the two largest are First Solar ($4.5 billion) and SunEdison ($5.3 billion), neither of which are (B)-class at the present time; and industrial 3D-printing, both hardware and software, can be had from the French, the Japanese, the Germans, China, and the US, and there are lots of software companies to drive the applications which are just emerging, slowly; and silicon is the keystone product for nearly all of our electronics technology and solar panels, but there is an excess of supply over demand and nearly all of it is produced by just three companies, only one of which is in the US, Applied Materials Incorporated; and marijuana services are from a software company, BioTrackTHC, which is owned by a private company, Bio-tech Medical Software Incorporated, but software is cheap because there are a lot of good programmers who can conjure up a new smoke screen on demand.

The Brave New World

A “large” economy, such as that of the US or China, or the World, always settles-in to the Company D modality, which is a subsistence economy in which we “owe” roughly three times what is “owed” to us in the local currency, which itself has no value but is a “promise” to pay, and the “worth” of it, and the prosperity of such an economy, is determined by the productivity of the people in it, and productivity is always engendered by trade (or conquest, and then trade) to acquire new ideas, skills, and materials.

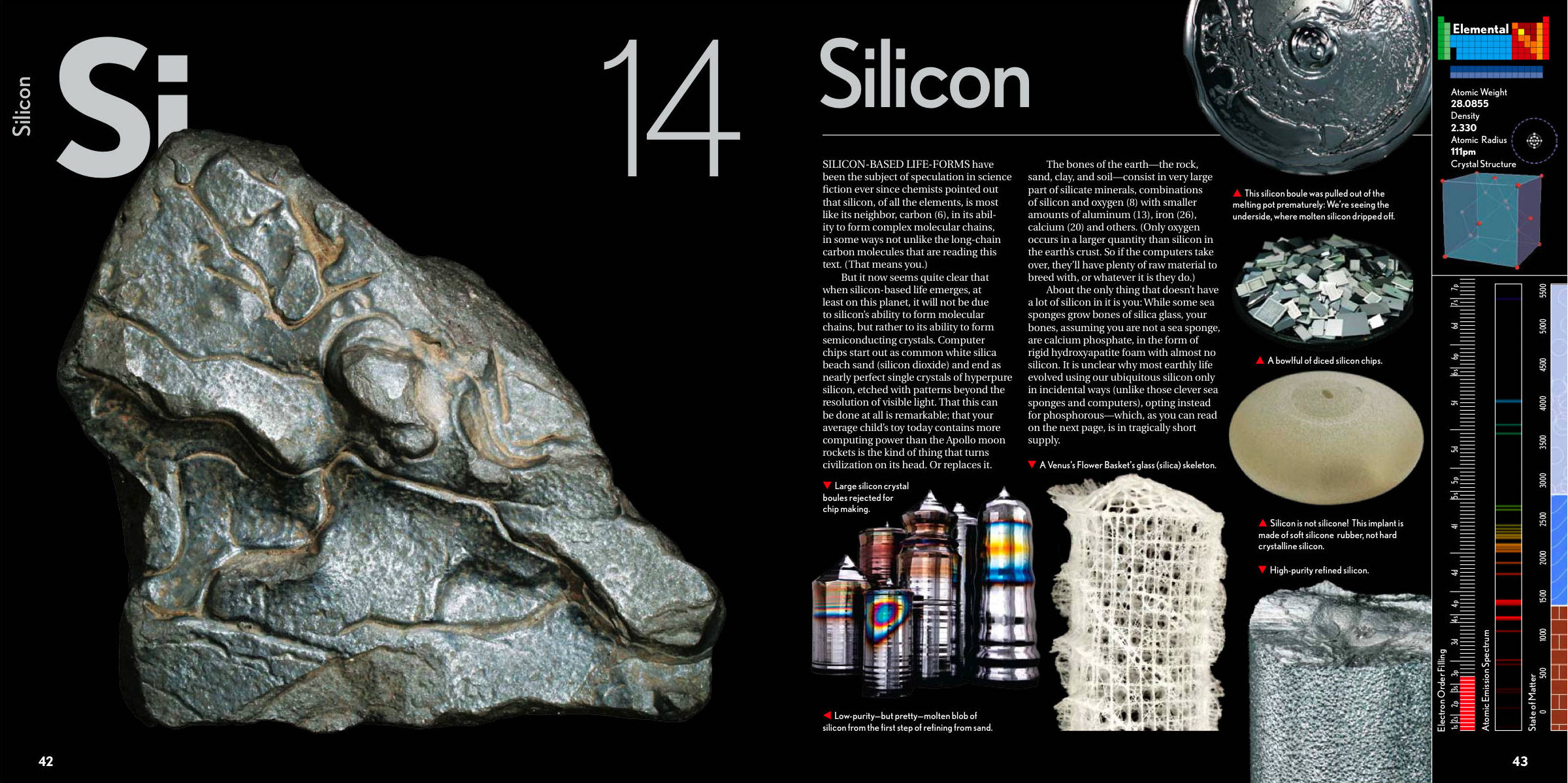

Moreover, we say what we mean – prosperity is determined by the productivity of the people in it – and even though some economies might have a “materials” advantage, it is bound to disappear; economics is about people, and their will to thrive, and not about materials; silicon, for example, is the 2nd most abundant material on Earth and the 8th most abundant material in the Universe, and it can be made into almost anything, including energy and, according to the fables, us.

Courtesy: The Elements, Theodore Gray, 2009

In fact, if we use our imagination, we could say that the World is about silicon and its applications in defense, energy, and materials that we can conjure out of almost anything by printing them (Business Insider, November 24, 2012, GE Is So Stoked About 3D Printing, They’re Using It To Make Parts For Jet Engines).

If, then, all that we have is defense, solar energy, silicon and 3D-printing, most of which we don’t even own – they are World resources – and all of which depend on silicon for which we have a glut, we’d best take a closer look at them.

They had a vision!

Of course, it doesn’t matter whether these groups of companies are growing faster than the others because their stock price won’t “grow” unless investors are willing to buy into them – they need a “vision” and that’s a fact that was discovered long before “diamonds were forever”.

But we can determine if they are having a “vision” by observing their behavior with respect to the price of risk; for example, if we’re not too discriminating, we can run all forty-four of the companies in the (B)-class, and that portfolio was dragged-down by defense and yielded only +308% in 2013, and another +71% in 2014; but solar was bigger – much bigger – in 2013 and yielded +689% in 2013 and another +124% in 2014, and the problem is that after last year’s “blow-out”, we’re down to just one company, Green Plains Incorporated, in the (B)-class, and we have a lot of cash to deal with.

Results like those are, of course, an “accident”, but it wasn’t our accident and we’re currently holding only twenty-one of the forty-four companies, down from forty last year, and we have a lot of new cash, waiting for more “accidents” in this market, or the next; please see Exhibit 1 below for more details.

Exhibit 1: The Brave New World – Risk Price Chart

Figure 1.1: (B)(N) Diamonds In The Rough – Risk Price Chart

For more information on real “risk management” in modern times and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary and “(P&I) Dividend Risk and Dividend Yield“, and our recent Posts “(P&I) The Profit Box” and “(P&I) The Process – In The Beginning“; and we’ve also profiled hundreds of companies in these Posts and the Search Box (upper right) might help you to find what you’re looking for, such as “(B)(N) TLM Talisman Energy Incorporated” or “(B)(N) ATHN AthenaHealth Incorporated” or “(B)(N) PETM PetSmart Incorporated“, to name just a few.

And for more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice. And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

And for more on what risk averse investing has done for us this year, please see our recent Posts on “(P&I) The Easy (EC) Theory of the Capital Markets” or “(B)(N) The Easy (EC) Theory of the S&P 500“, and the past, The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.