(B)(N) Defence Is Not An Option

And where do you prefer to shop?

On Food, Water (Air) or Land?

Drama. Defence is not an option and it is required for good governance as much as food, water and land by every people that would be sovereign (Foreign Affairs, February 2014, The Unruled World – The Case for Good Enough Global Governance).

However, defence is not an especially profitable business and has a profit margin like a grocery store that could replace it someday because at the end of day, after a million or so years of conflict and for all that we have to show for it, that’s what it’s about – food, water and land.

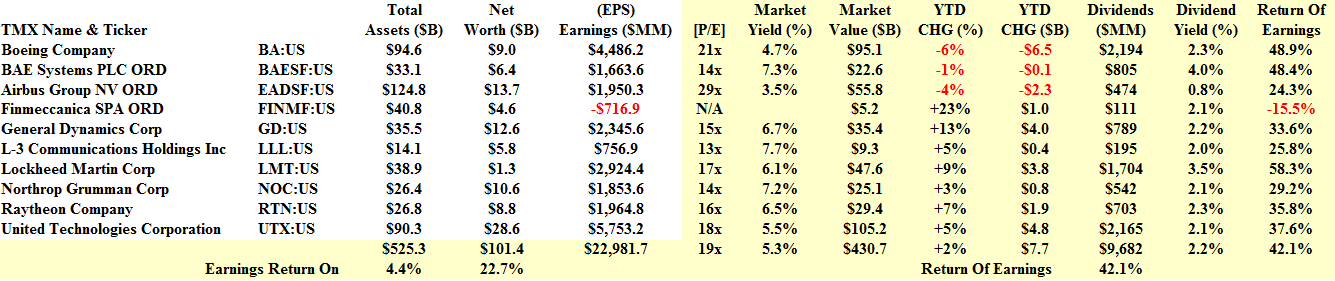

Notwithstanding megalomania and megalomaniacs who can be effectively defused with a closer look on HDTV, the ten largest primary defence contractors (that we know of) sold $400 billion of product last year and earned $20 billion which is less than a good day in the stock market or a good year at Wal-Mart.

And although we would prefer to throw carrots, peppers and beans rather than bombs, we’re unlikely to win that war at the present time (ibid, Foreign Affairs). And the stock market is just as bracing and has only one rule too – make money or die – and there are a lot of casualties to fuzzy thinking and bravado (Reuters, February 2, 2014, Hedge funds seek 1.8 billion damages from members of Porsche’s owning family).

So, as investors, we have no place to hide and we are always on the defensive – we want our money to be safe – 100% capital safety – and to obtain a hopeful but not necessarily guaranteed return above the rate of inflation which is a radically different approach than the purveyors of volatility and co-volatility and alleged market-beating gadgets of all sorts. But we’re not running for cover either. Please see Exhibit 1 below for the fundamentals that matter.

Exhibit 1: Defence Is Not An Option – Fundamentals – February 2014

Defence Is Not An Option – Fundamentals – February 2014

(B)(N) The “Undervalued” Defence Is Not An Option – February 2014

The defence contractors earned $23 billion last year and returned 42% of it or $9.6 billion to the shareholders for an aggregate dividend yield of 2.2%.

They also earned a remarkable 22% on the shareholders equity and their debt is leveraged 4:1 ($525 billion less $101 billion) so their credit rating is more than good.

After a fallow 2012, the market value increased by 55% and $150 billion last year and is followed by a further +2% and $7.7 billion so far this year. All ten of them are currently in the Perpetual Bond™ and that portfolio earned a staggering 67% last year, plus dividends. Please see Exhibit 2 and 3 below.

However, that’s the past and there is no safety in these numbers. The current portfolio has an estimated downside of minus (10%) in the next three months due to the demonstrated volatility absent surprise. But we would have made that same observation six months ago and $100 billion less than the market has since bid up these same stocks, all of which were trading above the price of risk then and are still trading above the price of risk now.

Resource and Non-Resource Canadian “Hot” Money Stocks

“Illiquid” versus “Liquid” Stocks

If, for example, bond yields were to increase in a low inflation environment, which is what we have, we can expect that investors will sell their equities – which they provably don’t understand anyway – and buy bonds which they also don’t understand but which look “safer” and have a practically guaranteed return and cash flow absent an increase in inflation.

But if the market swoons, the most affected stocks will be the roughly 20% of the stocks in the New York market and the roughly 50% of the Canadian market (S&P TSX) that are trading below the price of risk because those stocks are “overvalued” (even at low prices) because they are “illiquid” – an asking price to sell a large block will likely, and reasonably, be negotiated downwards and a bid price for a large block that is at or below the market price will likely find a grateful seller.

In contrast, the major defence contractors are “undervalued” (even at “high” prices) and demonstrate a benighted “liquidity” that is the goal of all investments and which they share with food and cigarettes and other essential industries such as the transports and utilities but not resources or commodities at the present time.

Exhibit 2: (B)(N) Defence Is Not An Option – Prices & Portfolio – February 2014

(B)(N) Defence Is Not An Option – Prices & Portfolio – February 2014

Exhibit 3: (B)(N) Defence Is Not An Option – Portfolio & Cash Flow Summary – February 2014

(B)(N) Defence Is Not An Option – Portfolio & Cash Flow Summary – February 2014

(Please Click on the Chart to make it larger and again if required.)

For more information on the chart elements and additional references to the theory, please see our Post, The RiskWerk Company Glossary.

For those of you with no pressing need for an F-35 or Cruise Missile, please see our Post The Gunsmiths.

And for more on what risk averse investing has done for us this year, please see our recent Posts on The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.