(B)(N) The Canada Deal Book

He Shoots! He Scores!

Deal Book. Last year, about a dozen Canadian companies made some “bet the farm” moves in acquisitions and divestitures, looking to re-structure and set the table for a better future for themselves, their employees, the shareholders and other stakeholders, such as their customers.

For example, Brookfield Asset Management is now the biggest landlord in the Los Angeles financial district after acquiring MPG Office Trust for US$2 billion and unloaded the lumber in its U.S. Pacific Northwest to Kapstone Paper and Packaging for $1 billion and transferred 260,000 hectares of timberland in Oregon and Washington State to Weyerhaeuser for US$2.65 billion.

HBC bought Saks for $2.9 billion in September and ExxonMobil of Houston, Texas, bought Calgary’s Celtic Exploration and conventional oil & gas production and reserves for $3.1 billion; BCE Bell Canada closed the deal on Astral Media for C$3.4 billion and KingSett Capital LLC and H&R REIT carved up Primaris REIT for $1.9 billion and $3.1 billion, respectively. And Rogers outbid the CBC to land the broadcast and digital rights to the NHL for the next 12 years for $5.2 billion. And First Quantum bought Inmet and its interest in the Cobre Panama copper mine, the largest in the world, for C$5.1 billion. And Sobeys landed Safeway for $5.8 billion and Loblaws picked up Shoppers Drug Mart for $12.4 billion in cash and stock and Valeant Pharmaceuticals bought Bausch & Lomb for $8.7 billion and is now re-purchasing its own stock for $1.3 billion.

Yes, that was exactly how it is?

But as investors peer into the past, their volatility and co-volatility models haven’t changed yet and their earnings forecasts are all askew and unreliable, what are they to do? They sell and punish themselves with their own uncertainty.

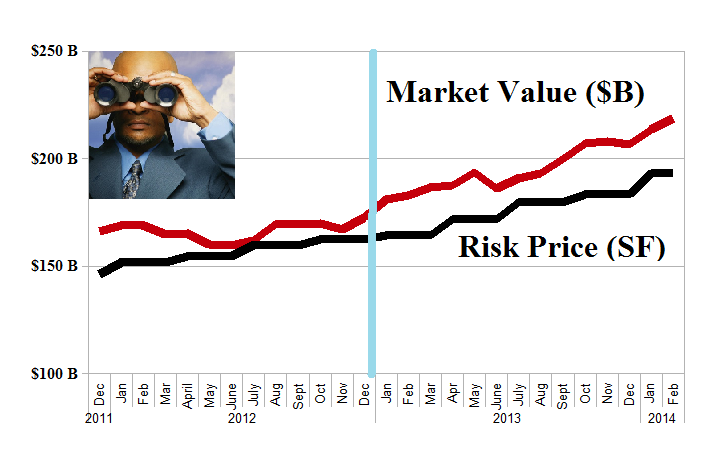

Nevertheless, these twelve companies gained +20% and $34 billion in market value last year and added another +6% and $12 billion since December.

They also earned $7.1 billion (net of losses of $3.3 billion) and paid $4.5 billion to the shareholders for a return of earnings of 64% and an aggregate dividend yield of 2.1%; and they made 7.4% on the shareholders equity and are carrying a debt of twice that ($334 billion less $97 billion).

And one might think that they are “overvalued” at 15× to 20× earnings, and possibly even at 30× counting in the losers, but that is not that case. Please see Exhibit 1 below for our map of the fundamentals.

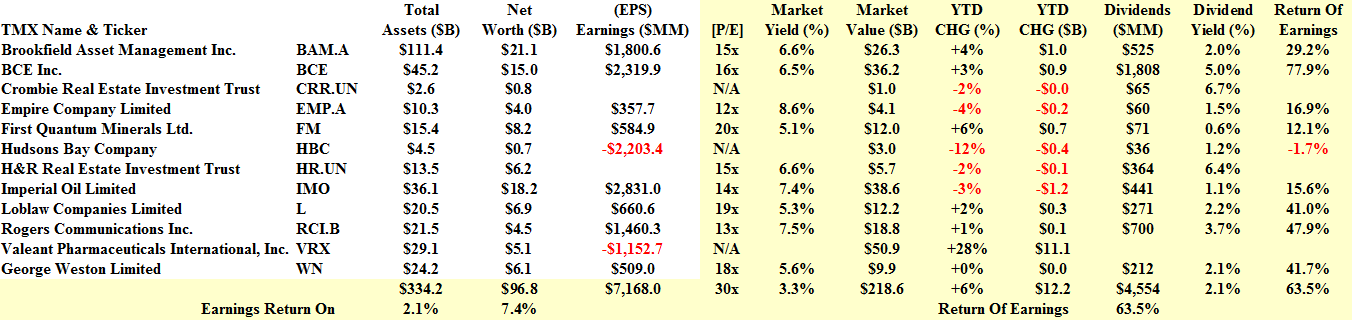

Exhibit 1: The Canada Deal Book – Fundamentals – February 2014

The Canada Deal Book – Funamentals – February 2014

The “Undervalued” Canada Deal Book – February 2014

Nine of the companies (excluding the two REITS, Crombie and H&R, and the retailer, Hudson’s Bay Company which distinguished itself with a $2 billion loss on sales of about $4 billion) are in Perpetual Bond™ and all but First Quantum Minerals have been so for all of last year.

The reason that they are “undervalued” is that they demonstrate an excess of demand over supply at these prices, however elevated, and the real-time “test” for that is “liquidity“.

An offer to sell a large block of these stocks at the current prices will likely be taken up with glee and thank you and put no downward pressure on the price; whereas as offer to buy a large block at these prices will likely be met with resistance and the buyer might have to bid them up in order to get them.

Those are the facts and we can see from the fundamentals, as an example, that that has not much to do with [P/E]s and volatility. Please see Exhibit 2 and 3 below for the details.

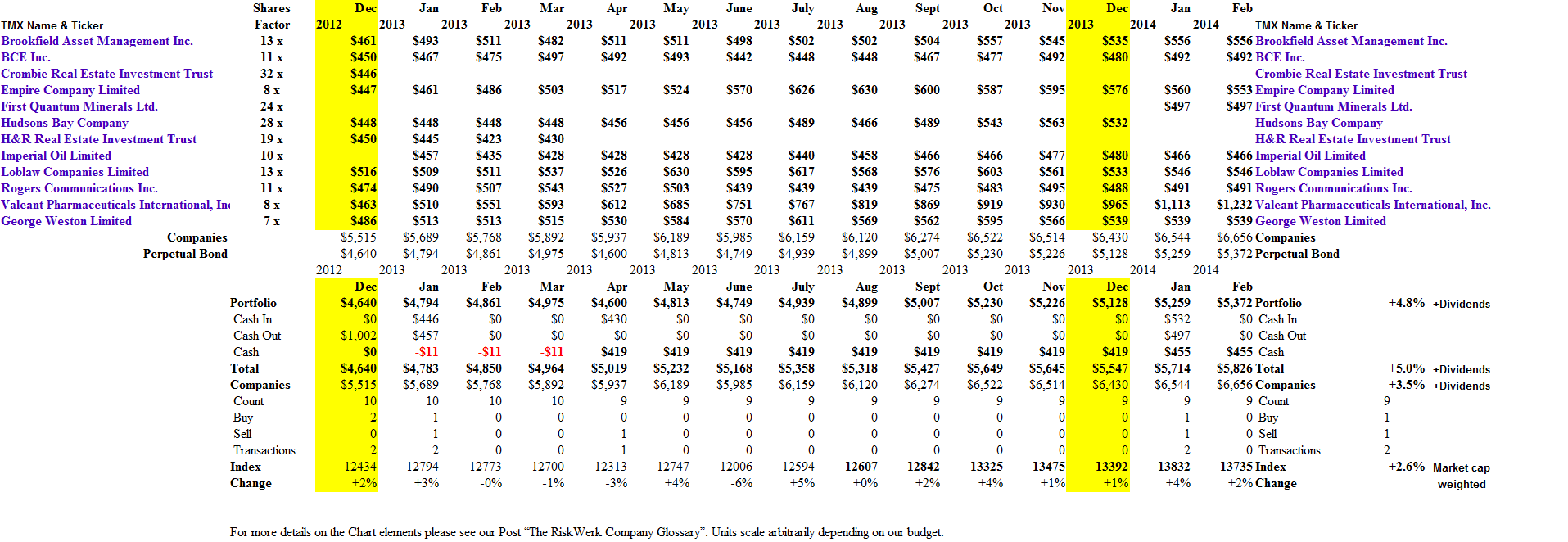

Exhibit 2: (B)(N) The “Undervalued” Canada Deal Book – Prices & Portfolio – February 2014

(B)(N) The Undervalued Canada Deal Book – Prices & Portfolio – February 2014

Exhibit 3: (B)(N) The “Undervalued” Canada Deal Book – Portfolio & Cash Flow Summary – February 2014

(B)(N) The Undervalued Canada Deal Book – Portfolio & Cash Flow Summary – February 2014

(Please Click on the Charts to make them larger and again if required.)

For more information on the chart elements and additional references to the theory, please see our Post, The RiskWerk Company Glossary.

And for more on what risk averse investing has done for us this year, please see our recent Posts on The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.