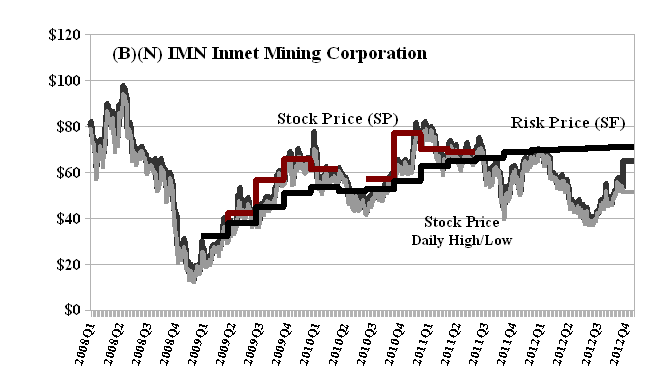

(B)(N) IMN Inmet Mining Corporation

Deal Book. Inmet Mining Corporation has turned down a $70 per share friendly but unsolicited takeover offer from FM First Quantum Minerals Limited (Reuters, November 28, 2012, Inmet turns down First Quantum bid, adopts rights plan). If the offer were in cash (C$4.86 billion) then the shareholders of Inmet would be fairly compensated on a risk-adjusted basis because the Risk Price (SF) is currently also $70 to $71 (please see Exhibit 1 below) and has been steadily rising since $60 to $70 last year (2011) although one might think that the risk price is more likely to go up in the future months as more of its projects and operations are completed or developed absent the ever present possibility of disasters such as mine explosions or flooding, labour unrest or government force majeur.

However, the offer is not in cash but consists of C$2.461 billion in cash and up to 112.679 million shares (113 million) of common stock in First Quantum issued from treasury and valued at the current market or trading price of about $21.50 and, therefore, $2.4 billion. But the current Risk Price (SF) for First Quantum is $29 (and has also been rising, please see Exhibit 2 below) so how is the risk-adjusted shortfall of $8 per share to be recovered or compensated? To put it another way, there’s $900 million ($8×113 million shares) on the table that is likely to go in and then go out of the pockets of ex-Inmet shareholders in the future – possibly the near future – if the deal is accepted as proposed. (Please see our recent Post, (B)(N) PRY Pinecrest Energy Incorporated, November 2012, for an example of a no cash, all stock deal which further explains the meaning of the Risk Price (SF) in this context.)

That would certainly be the case if the stock price of First Quantum due to dilution (which is about 25%) and operational and business concerns were to drop by $8 in the next year and that has certainly happened several times before (please see Exhibit 2 in 2010, 2011 and even this year 2012). The protection that could be offered to the Inmet shareholders is (for example) warrants at $8 per new share exercisable before July 2013 (say) and there will be a market for those that is similar to that of put options. For example, the July 2013 put at $21 is currently asked at $3.35 per share but there are no contracts at the present time.

In the deal-making scuttlebutt and posturing (please see the news), there’s more hand waving than the Jetta warriors, but it’s really quite simple, isn’t it. We are, indeed, buying risk but – all bounty aside – we also demand the guarantee of capital safety and a hopeful return above the rate of inflation. Please see our Post, The Price of Risk, August 2012, for information.

Exhibit 1: (B)(N) IMN Inmet Mining Corporation – Risk Price

Inmet Mining Corporation is a Canadian-based global mining company that produces base metals with a focus on copper.

(Please Click on the Chart to make it larger if required.)

The Canadian base metal miner is building the massive Cobre Panama copper mine in Central America and has adopted a shareholder rights plan to give it more time to evaluate bids and potentially seek alternatives to a takeover. In addition to its 80 percent stake in Cobre Panama, Inmet owns operating mines in Turkey, Spain and Finland.

Exhibit 2: (B)(N) FM First Quantum Minerals Limited – Risk Price

First Quantum Minerals Limited is a mining and metals company engaged in mineral exploration, development and mining.

(Please Click on the Chart to make it larger if required.)

First Quantum of Vancouver, British Columbia, operates mines in Zambia, Mauritania and Australia and owns mining assets in Africa, Australia, South America and Europe.

The RiskWerk Company does not own any of the common stock of either of these two companies and has no financial or fiduciary interest in these transactions.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.