(B)(N) RIM Research in Motion Limited

Drama. Research in Motion has NOT been in our investment portfolio, the Perpetual Bond™, for years. Not when it was $140 in 2008 or $90 the year after or $60 last year or $10 or less this year but it keeps getting press attention that can’t be bought at any price. And certainly not by a technically $10 “penny stock” that has never paid a dividend. (The Globe and Mail, November 30, 2012, RIM’s roller coaster ride.)

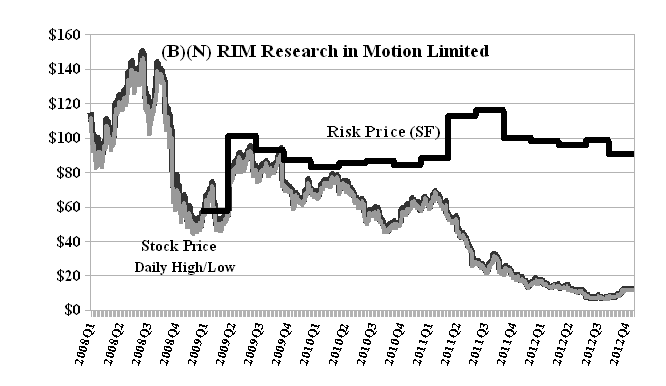

Possibly the company just needs more time to figure out what it’s doing – and to do it – but the stock market has nothing to do with that. (Please see our recent Post, Do Stock Prices Mean Anything?, November 2012.) Blowing life or death into it on a daily basis creates opportunities for day-traders and penny stock market “players” between $8 to $10 to $12 to $10 to $8 (again) but we have no idea of what it might be “worth” absent some new operational and business results even though we know frequently what somebody has paid for it. They “paid” $60 billion for it in 2008, $30 billion in 2011 and $6 billion this year and there are some who think that it might be “bought” and a bargain for $9 billion next year. We don’t have any idea or opinion about that at all. The stock price will be whatever somebody is willing to pay for it. The Risk Price (SF), however, is the risk-adjusted price and remains firmly above $80 and is currently $90 (please see Exhibit 1 below, Black Line, a step-function) and one might wonder what that means given that we will not own a stock in the Perpetual Bond™ unless the ambient stock price Stock Price (SP) is apparently and plausibly above the Risk Price (SF).

In round numbers, the company has total assets of $12 billion, debt or total liabilities of $3 billion, shareholders equity of $9 billion and a current market value of less than that, $5 billion to $6 billion (which could be compared with some well-heeled competitors such as Samsung $160 billion or Apple $600 billion). The Risk Price (SF), however, is our estimate of “the least stock price at which the company is likeable” (Goetze 2009) and the essential standard of “likeability” is that portfolios of likeable stocks will tend not to lose in value and the contra, that the portfolio of stocks that are deemed “not likeable” in the same market will tend not to gain in value. (Please see our Post, The Price of Risk, August 2012, for more information.)

The Risk Price (SF) is also an estimate of a “fair value” acquisition price but it’s hard to imagine – though not impossible circa a few years ago – that anyone would pay $40 billion ($80 for 500 million shares) to acquire all of RIM at the present time. Still, a large or controlling interest could be had for a lot less but to pay less, the risk remains firmly attached. It just has new owners. (Please see, for example, our recent Post, (B)(N) IMN Inmet Mining Corporation, November 2012.)

Exhibit 1: (B)(N) RIM Research in Motion Limited – Risk Price

Research in Motion Limited designs, manufactures, and markets wireless solutions for the mobile communications market worldwide. It provides platforms and solutions for access to information, including email, voice, and instant messaging.

(Please Click on the Chart to make it larger if required.)

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.