(B)(N) CTC.A Canadian Tire Corporation Limited

Deal Book. The Canadian Tire stores are our everything stores. If we need anything at all, excepting what we might buy at Loblaws or the Shoppers Drug Mart, we can get it there and some of our happiest purchases in living, playing and fixing (as they say) have been made at the Canadian Tire stores. Like Bombardier (please see our Post, Do Stock Prices Mean Anything?, November 2012) there is a controlling block of common shares (ticker CTC of about 3.4 million shares with a market value of $220 million) that have the only vote and final say, and the other much more common common shares (CTC.A of about 78 million shares with a market value of about $5 billion or twenty times as much) that don’t but all of the shares currently receive a dividend of $1.40 per year per share or $110 million in aggregate for a current yield of about 2% that is comparable to inflation.

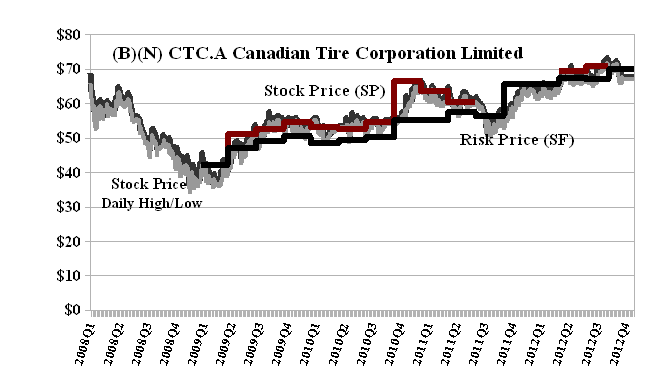

Exhibit 1: (B)(N) CTC.A Canadian Tire Corporation Limited – Risk Chart

Canadian Tire Corporation is comprised of two main business operations that offer a range of retail goods and services including general merchandise, clothing, sporting goods, petroleum and financial services.

(Please Click on the Chart to make it larger if required.)

Last year (in August 2011), Canadian Tire acquired The Forzani Group (now called FGL Sports and a subsidiary) in a deal worth about C$770 million in cash (please see, Reuters, May 6, 2011, Canadian Tire to buy Forzani Group for $798.5 million) which paid a 50% premium on the stock price (and, as it turns out, on the Risk Price (SF) which was about $18 at the time) to the Forzani Group shareholders. This year, Canadian Tire is buying Pro Hockey Life Sporting Goods Incorporated for C$85 million (again in cash, albeit, petty cash) to expand its stand-alone sporting goods businesses (Reuters, November 28, 2012, Canadian Tire to buy hockey gear retailer).

In principle, there are 100 million Class A Non-Voting Shares in the company’s charter and the company could float those shares above the 78 million shares already issued into the market for ready cash gains of $1 billion or more but the company has generally maintained an anti-dilutive policy with respect to those shares. There is a war chest, so to speak, but $1 billion isn’t what it used to be even though the company is somewhat leveraged with $8 billion in total debt and $4.6 billion in net worth or shareholders equity which is about the same as the current market value ($5 billion). However, debt, usefully applied, is not so much a liability as it is an asset.

The Risk Chart (please see Exhibit 1 above) shows that the Risk Price (SF) (Black Line and a step-function) and the stock price or Stock Price (SP) (Red Line and also a step-function) tend to maintain a Nash Equilibrium (please our Post, The Nash Equilibrium & Its Stock Price, October 2012) which demonstrates that the investors tend to just “like” the stock and are willing to hold it as readily as cash, and more so for the possibility of gains in price and dividends that have some chance to exceed the rate of inflation which, of course, cash doesn’t have. Please see our Post, The Price of Risk, August 2012, for more information on “likeability”.

At the present time, the stock is trading at $67 and below the price of risk $70 (Risk Price(SF)) and we can’t buy it for the Perpetual Bond™ because of the rules (please see, for example, The Wall Street Put, August 2012) and, of course, we never make forecasts of what the future might be for a company or its stock price (no matter how many hockey sticks are found wanting). That would be speculation and a gamble. Please see our Post, The Active Investor (DOA), November 2012.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories ust attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.