(B)(N) BlackRock’s Broken Bond Market

Not Fit For Purpose

Courtesy: BlackRock Incorporated

Drama. BlackRock has advised us that the market for corporate (not government) bonds is “broken” because the “gate-keepers”, which are largely the banks who are the broker/dealers, are extracting an “unearned toll”, and won’t let go – even though they will eventually have to let go in order to maintain their regulatory capital (Bloomberg, September 22, 2014, BlackRock Urges Changes in ‘Broken’ Corporate Bond Market).

BlackRock’s proposal – which we paraphrase – is that the bond market needs to be “securitized” so that bonds can trade like equities, either individually or in packages, with standardized coupon dates and more typical amounts in tranches of not less than $750 million.

The purpose of trading these bonds in a securities market is that all-to-all trading (as in equities) is likely to uncover liquidity which is currently blocked by the broker/dealers and their one-on-one trading model that earns not only fees and commissions but profits on their inventory which has become smaller and is likely to become still smaller if they cannot finance the inventory pending its sale, and maintain their regulatory capital requirements; please see our Post “(P&I) The Banker’s Modality” for more information on how “inventory” affects bank profits.

The market in mortgage-backed securities (MBS) that developed in the 80’s demonstrates the liquidity-creating possibilities of all-to-all trading, whereas the market in municipal bonds (which currently has over one million issues and an aggregate amount of only $3.7 trillion) demonstrates an illiquid market with prices created by the broker/dealer network and the”local weather”, so to speak, and often contained in so-called “alternative investments” sold to insurance companies and pension plans.

It’s possible that BlackRock can create this market by itself, and it’s a new market, and all that it really needs is the ability to lend about $11 trillion (over time) and replace the current diaspora of roughly 40,000 corporate bonds of impossibly complicated amounts, and terms, and feckless grades, with about 11,000 new ones with face amounts of not less than $750 million, and with definite semi-annual coupon dates (of which there are only four, the 15th of March, June, September and December) and rational terms ab initio.

And it will shake the industry to its core (The Economist, September 27, 2014, The future of banking: You’re boring. Get used to it and our recent Post “(B)(N) Money on the Run“).

Investment Grade

If all the bonds are “investment grade”, then they can be held to maturity without risk of default – although companies might change, but even in bankruptcy, the bondholders are almost always made good (absent the Panama Canal (1892) or something like that that has no provable earnings) – and their current (secondary market) price will be rationally determined by their coupon rate and any adjustments for inflation and the current rates of interest, subject to liquidity considerations – such as who will buy them, who has the money to lend if not the banks, and why will they buy them, et cetera – which can also be moderated, or encouraged, by increasing or decreasing their price subject to “price discovery” in a well-posted securities market (which we have today).

In our well-known but widely disputed view, there is only one “investment grade” – safe, liquid, and hopeful – that is 100% capital safety, 100% liquidity, and a hopeful but not necessarily guaranteed return above the rate of inflation – and we know how to enforce that rule in the equities market.

It is said that the Barber of Seville cuts everyone’s hair but not his own …

However, the facts of the market demonstrate that most investors, whether professional or retail or academic, think that all other investors are fools, or possibly just misinformed, and that they are not among them and, as a result, there is a decidedly Darwinian aspect to the market that defines its very being, and the gradual erosion of consumer wealth and savings into deeper pockets which are not necessarily any smarter.

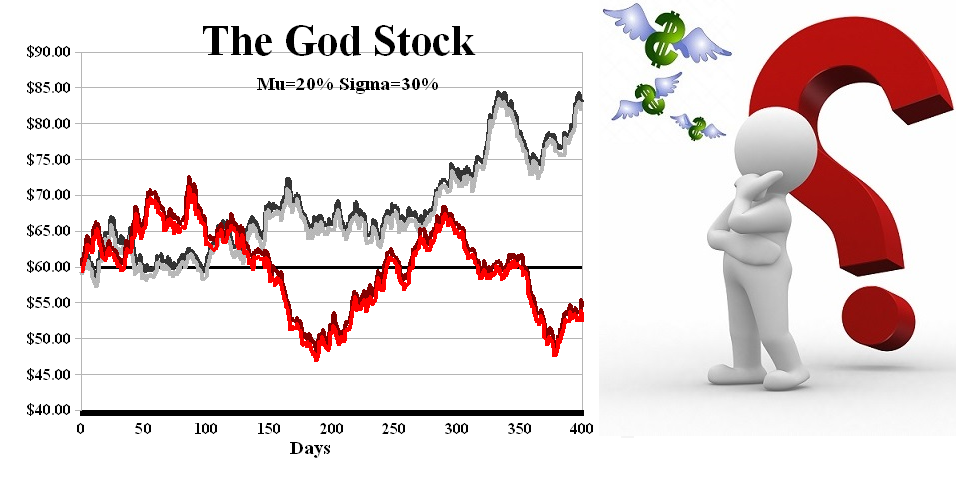

But there is no reason for any stock price other than that’s the price for which it can be sold, or bought, and the reasons for these transactions are always different for the buyer and the seller; the chart below (Exhibit 1) shows how far out-of-whack the market prices are with respect to the mere goal of a hopeful non-negative real return, as opposed to the merely desired, but unfounded, outcome of “making a killing”.

Figure 2: The God Stock Does Not Reward Risk and Investing Is Not A Trial

The reason for this “whackiness” is the widespread and regimental use of the Capital Assets Pricing Model (CAPM) and Modern Portfolio Theory (MPT) which promote the “risk/reward equation” but explain nothing and render that result which could have been attained by just buying and holding the same stocks; please see our recent Post “(B)(N) American Small Caps” for more information.

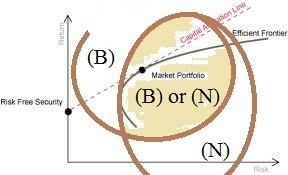

However, in contradistinction to this alleged market model, we have shown that any market separates into the (B)-portfolio of stocks for which prices can be defended above the price of risk, and the (N)-portfolio of stocks for which the prices are subject to investor uncertainty and for which the price of zero competes with any other such price, and that this “partition” is determined by demand and supply and, effectively, liquidity concerns, but “volatility” is irrelevant; please see Figure 3 below.

Figure 3: Efficient Frontier (B)(N) Boundary Open

We also note that the price of risk is a phantom stock price and that it can be computed as the solution of a Nash Equilibrium between risk-seeking and risk-averse (less risk-seeking) investors but, in practice, the “price of risk” for any investment is the purchase price, and whether or not it is “the” price of risk depends on whether that price can be defended in the market; for example, a stock that is trading in the (N)-zone of investor uncertainty is as likely to render any stop/loss price, or bought put, without “value” as it is with “value”.

The above model also shows that the “high frequency trader” (ibid the BlackRock proposal) is just another dealer operating on nano-cycles rather than seconds, or days, or weeks, or months, or possibly, an eternity if the price, or the product, is not right.

Priced On Hope, Not Volatility

The pricing of the bonds in the secondary market – given that they are all of investment grade and we can expect the coupon rate and the return of capital – depends only on inflation and the anticipation of inflation, for which volatility is meaningless and “past performance” has most definitely nothing to do with “future performance”, and it also depends on the need, or desire, for liquidity or investment (in the alternative).

Equities, on the other hand, don’t have those benefits; that is, there is no assurance in a stock price, and no compensation for a business failure other than a well-crafted short position, and nothing that is known that will drive a stock price other than demand over supply, for which there are as many reasons as there are investors and their money.

Once again, assuming that the bonds are all “investment grade” (and we don’t rely on the rating companies for that, although other investors might), we can examine a portfolio of them for arbitrage opportunities by correlating the Enterprise Risk, which is based on the “factors of production” (N*) supporting the shareholders equity (N), and therefore the earnings, with the modality, α=R/P, where R is “what is owed to the firm” and net of what it owns, with the total liabilities (P) which we usually describe as “what the firm owes”, which is everything above the shareholders equity, including the long term debt, preferred shares, and minority interest (if any).

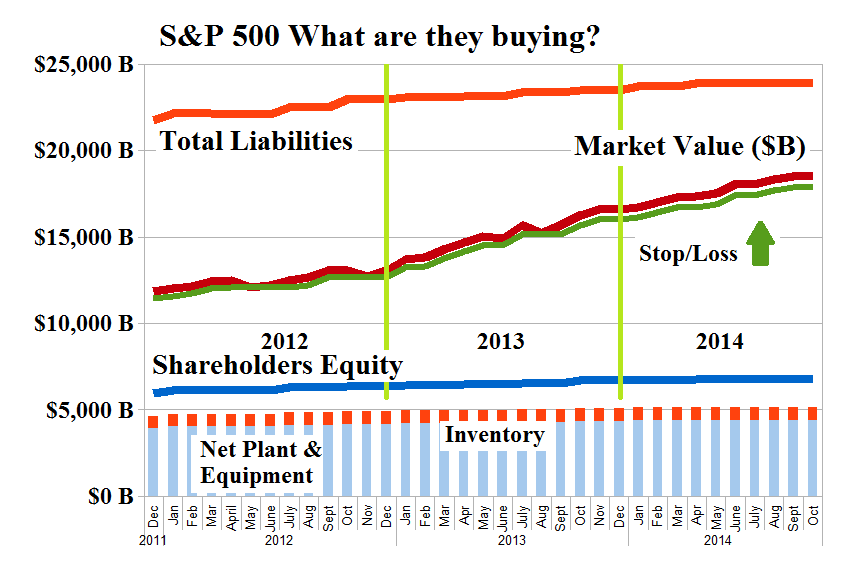

Exhibit 1: S&P 500 What are they buying?

Figure 1.1: S&P 500 What are they buying

But the first thrilling question that we might dwell on is, What are they buying?

The chart on the left shows the aggregate market value ($18.5 trillion, up +50% from $12 trillion in 2012) of the S&P 500 companies since 2012, and also “what they are” – their total liabilities ($23.8 trillion up from $22 trillion); the shareholders equity ($6.8 trillion up from $6.1 trillion); their fixed assets ($4.4 trillion up from $4.0 trillion); and their inventory ($760 billion up from $696 billion in 2012).

Interesting! this planet you have!

And the chart also shows “what they will be”, no matter what the stock price in the next year, and probably for the next several years absent some miracle of growth.

If we were an alien, from another planet, and not used to gambling, we might conclude that the “investors” here have a lot money, but not much sense.

The New World of Money

Fire! The market is going down, ha ha.

There are also a lot of “bears” around who are saying that the market “has” to go down. But to what? And why? And when?

The chart (Figure 1.1 above) shows that our money, as “money”, isn’t worth very much, and has depreciated by nearly 50% against the things that we’re trying to buy with it.

Investors who sell now and “take profits”, or are poised to sell now (such as at the stop/loss shown in Figure 1.1), need to yell Fire! on the way down and out, because their real fear is not that the market will go down, but that it will go up and they’ll be left holding nothing but their money, and the price of equities – and income – is rising.

What they want is that the market should go down so that they can eventually use their cash to buy more equities at lower prices, which explains the “gradual erosion of consumer wealth and savings into deeper pockets” which we described above, and of which the most recent 2008 and 2009 fiasco is a good example.

From the SEC Chair, Mary Jo White: “The U.S. securities markets are the largest and most robust in the world, and they are fundamental to the global economy. They transform the savings of investors into capital for thousands of companies, add to nest eggs, send our children to college, turn American ingenuity into innovation, finance critical public infrastructure, and help transfer unwanted financial risks.”

Not for us, they say.

Which is true, of course, but it’s not the education for their children, or their nest eggs, that they’re buying with their savings.

Our defense, of course, is not to sell until the market sells us out and the issue for us is not capital gains – which we already have and know how to keep – but what can we do to enhance our returns of income above the rate of inflation?

But that’s (nearly) the same as the dividend yield – which companies try to maintain – and capital gains on equities, which are subject to changing circumstances that might affect the company or its industry, and are largely calibrated to the company’s earnings and, therefore, to its ability to maintain the dividend yield by maintaining the payout rate on higher earnings, which we call the “Dividend Risk”.

Risk, Risk, Risk & More Yield

In order to get to the “yield”, we need to wade through a lot of “risk” and the new bond market will compete with our equity dollar because it too is an “all-to-all” transaction and not just the “all-to-one” transaction of the current bespoke market for corporate bonds.

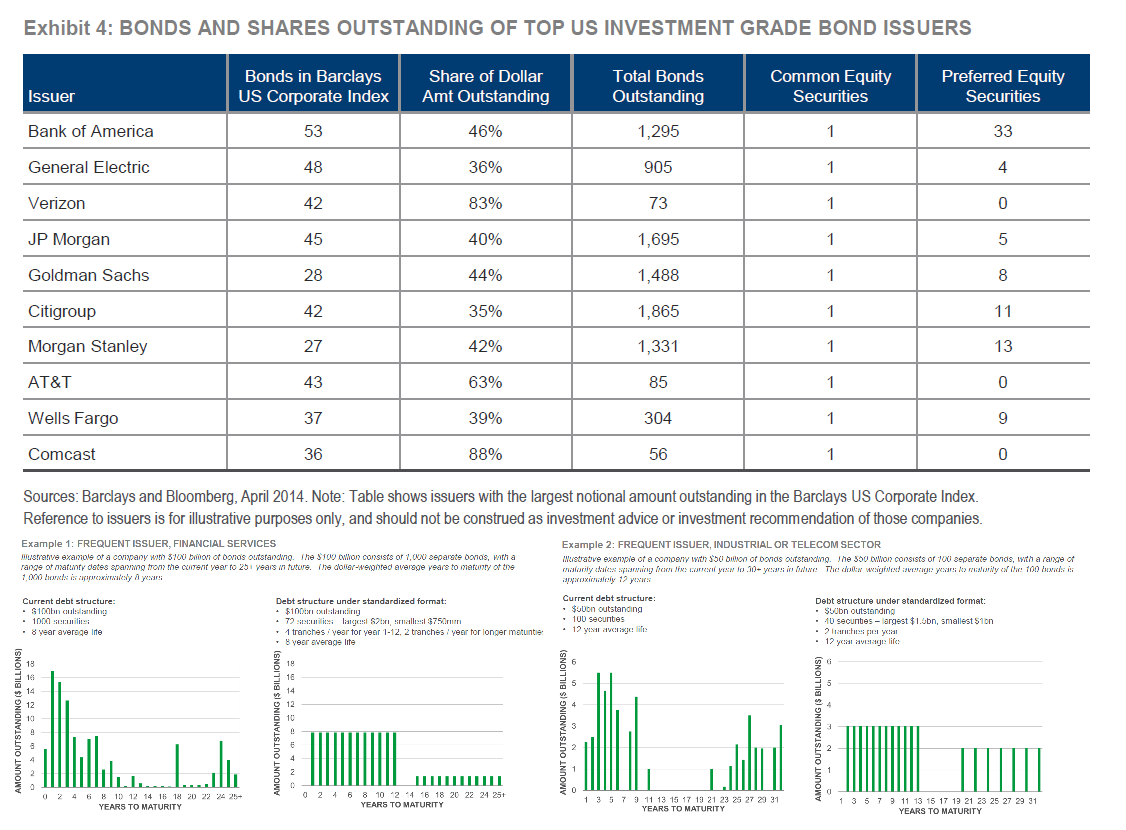

Figure 4 Courtesy: BlackRock Bonds & Issuer

For example, is it better to buy an interest in the company’s stock, or an interest in its debt which is also trading in a similar market of bid and ask prices, and possibly through an ETF that indexes a basket of them?

Moreover, the goals are the same because each of them offers opportunities for both capital gains and dividend (or coupon) returns and yields; please see Figure 4 on the right.

And is there a reason that there might be a difference? Because if there is, we can reasonably expect arbitrage opportunities for which the returns are certain (with probability one).

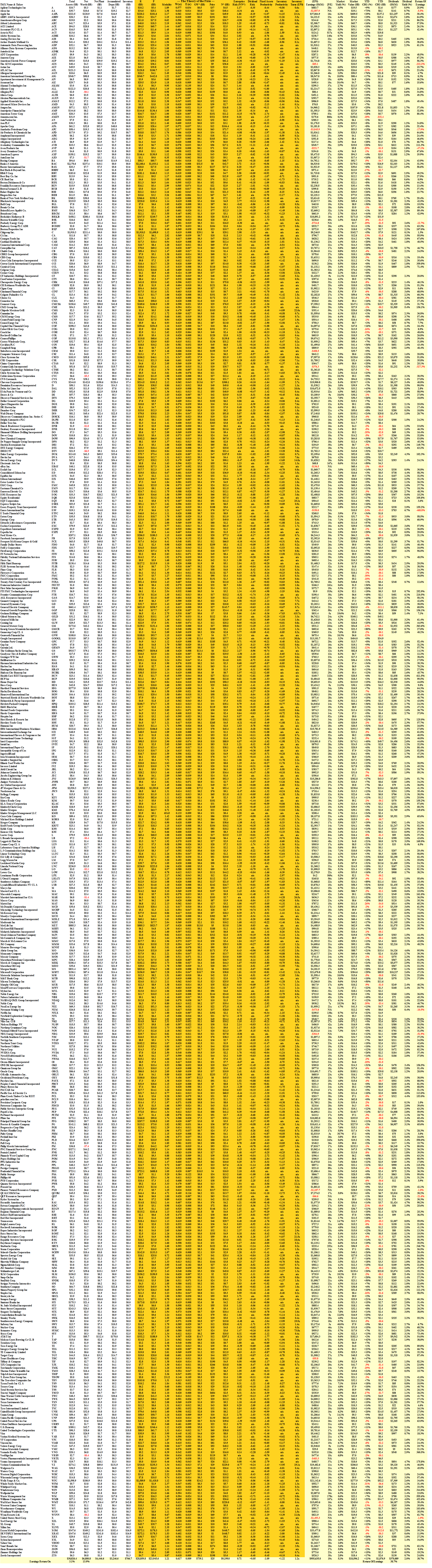

As we noted above, the “Enterprise Risk” measures the ability of the “factors of production” (N*) to support the shareholders equity (N); the “Debt Risk”, however, for “Investment Grade” companies, is the inverse of the modality because companies that do not use the debt market to fund growth, are using their own money, the shareholders money, to do it; please see Exhibit 2.1 below and for further details, please click on the link (and again to make it larger) “S&P 500 Fundamentals“.

Exhibit 2: S&P 500 Enterprise Risk and Debt Risk

Figure 2.1: S&P 500 Enterprise Risk & Debt Risk

The chart (Figure 2.1 on the left) shows the “virtuous circle”, Enterprise Risk=Debt Risk=1, which is the benchmark for “Investment Grade” affecting bonds, and raises questions for companies that are off-line, so to speak, and opportunities for arbitrage for near neighbors with respect to one measure but not the other.

It solves the “bond problem” of what’s good and what’s not so good, and maybe even what should be avoided if the right answers are not forthcoming and intelligible.

But it doesn’t solve the “yield problem” on whether it might be better to buy the bonds and clip the coupons, or buy the equities and cash the dividends, and capital gains on either, if any.

The market price of the Coase Dividend relates “virtue” to “price”, but it is only meaningful in the context of companies with similar challenges affecting their “trading connections”, and although investors and the market can “feel it”, they can’t see it, and it is best-used in the IPO situation for a new company in an established industry which contains its competitors; please see, for example, our recent Posts on “(B)(N) BABA Alibaba Group Holdings Limited” or “(B)(N) Fannie Mae & Freddie Mac“.

Moreover, “good companies” don’t necessarily get “good prices” (and sometimes “bad companies” do) and we have explored that fact in several recent Posts on the retail and food (groceries) industries; for example “(B)(N) Good Food For Thought” and “(B)(N) Tesco PLC et al“, or “(B)(N) BONT Bon-Ton Stores Incorporated“.

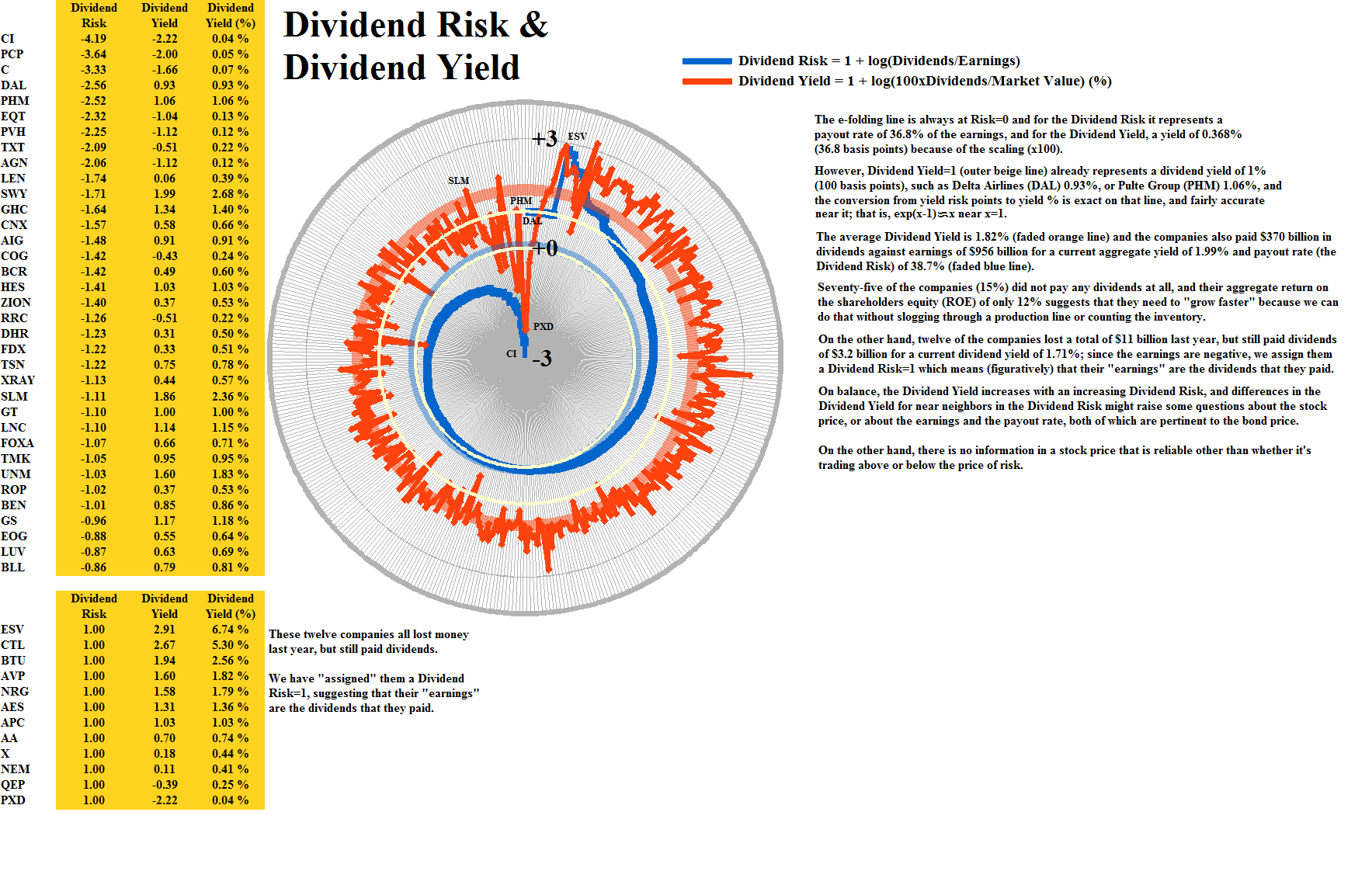

But we can bridge the gap between bond yields and dividend yields by looking at the relationship between the Enterprise Risk and the Dividend Risk, which is the payout rate on earnings, and the Dividend Risk against the Dividend Yield, which tells us how the market is pricing the payout rate and the earnings; please see Figure 2.2 and 2.3 below.

Figure 2.2: S&P 500 Enterprise Risk & Dividend Risk |

Figure 2.3: S&P 500 Dividend Risk & Dividend Yield |

For more information on the “Five Equations of State”, and an introduction to the terms that we have used here, please see our Post “(B)(N) Through the Looking-Glass“, and for the really hard rocks, the Theory of the Firm which is based on The Process.

And for more information on real “risk management” in modern times and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary and “(P&I) Dividend Risk and Dividend Yield“, and our recent Posts “(P&I) The Profit Box” and “(P&I) The Process – In The Beginning“; and we’ve also profiled hundreds of companies in these Posts and the Search Box (upper right) might help you to find what you’re looking for, such as “(B)(N) TLM Talisman Energy Incorporated” or “(B)(N) ATHN AthenaHealth Incorporated” or “(B)(N) PETM PetSmart Incorporated“, to name just a few.

And for more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice. And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

And for more on what risk averse investing has done for us this year, please see our recent Posts on “(P&I) The Easy (EC) Theory of the Capital Markets” or “(B)(N) The Easy (EC) Theory of the S&P 500“, and the past, The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.

{kind=link}