(B)(N) More Money, Please (REITS)

Maybe it’s REITs that are forever

Drama. Real Estate Investment Trusts (REITs) have become an attractive investment to income-seekers because of their high payout rates against earnings – guaranteed to be not less than 90% of the company’s pre-tax income and almost as good as owning the company but not the management of it – and hopefully, there will be earnings.

But – earnings or not – fluent access to both the debt and equity markets is important to these companies, and if the earnings falter in one quarter or so, most REITs will try to maintain the dividend yield, and possibly the shareholder’s income, even if they have to borrow money or sell assets or issue new stock, to do it – they have some options that we, as persons, or business owners, don’t usually have.

REIT World – Now and Hereafter

Globally, there are about 400 REIT-structured public companies with $1 trillion in shareholders equity (FTSE EPRA/NAREIT Global Real Estate Index Series) and the professional management of income producing properties (not all of which are real estate) should produce steadfast and workman-like profits, no matter what the weather on Wall Street, which goals are not the same as ours in any case, and we have cause to wonder if there are enough of these to go around; please see below.

The Eternal Life Annuity

It would appear that buying a REIT at rock-bottom prices – and possibly at any price, which we’ll look at below – is as good as buying an eternal life annuity at any age, regardless of health, or wealth, which would be doubly attractive to those of us who want our money, both capital and income, to outlive us, and not so much the other way around.

Figure 1: (B)(N) RYN Rayonier Incorporated REIT

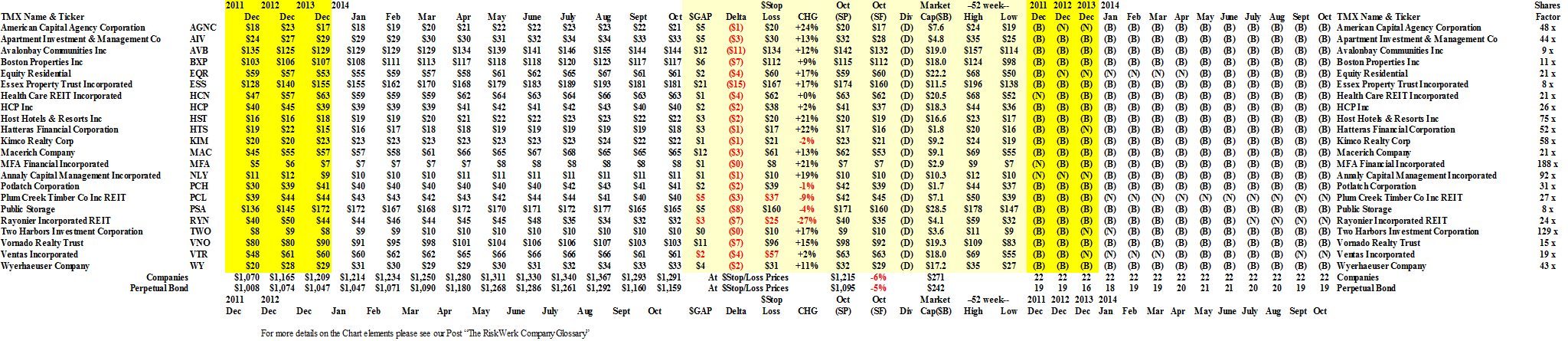

That hypothesis needs to be tested; for example, the US REITs are up in aggregate about 7% this year, but they’re only level with their 2012 prices, and there are some, such as Rayonier Incorporated (RYN) that are down minus (-27%) to produce a current yield of only 6.1%; please see Figure 1 on the right.

Moreover, their aggregate return on equity was only 13.5 % last year, and only 4.4% on the assets, but if we exclude the “financials” – those REITS without properties – the numbers are 15.1% and 7.1%, respectively, which are better returns than most investors and rental property-owners can get, year-after-year; please see Exhibit 1 below for the fundamentals.

The issue, then, is whether we should buy REITS at low prices – or even now at somewhat higher prices – and not worry if the price goes even lower, which it might do if the interest rates are increasing, but not make any difference to our income regardless of how it might affect their income, or send a made in Wall Street signal that there might be a problem with the earnings (The Street, September 29, 2014, Mortgage REITs Offer Great Yields, but Big Risks Remain).

Exhibit 1: (B)(N) S&P NYSE REIT World – Fundamentals

S&P NYSE REIT World – Fundamentals

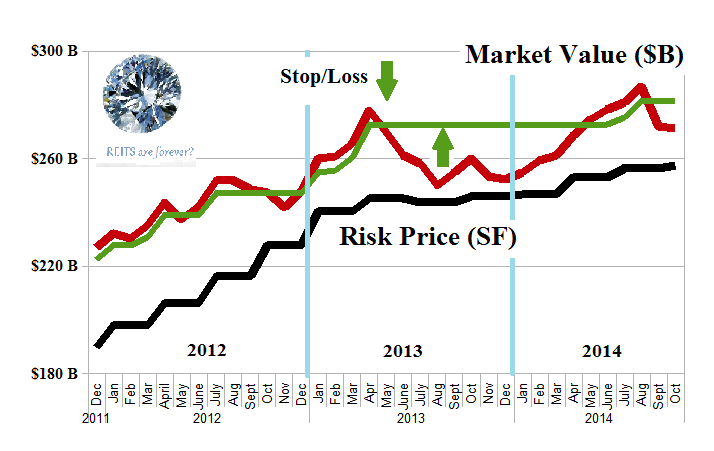

Figure 1.1: (B)(N) S&P NYSE REIT World – Risk Price Chart

There are plenty of “salespersons” on Wall Street, and elsewhere, who will tell us which REITs to buy and sell and when.

But we’re not interested in making a quick buck – we’re looking for the long term – and we can’t rely on an economic forecast to tell us much about the future, or even next week.

What we want to know is what can we do to protect our capital and our income, in all weathers, for an eternity or until it arrives.

And these REITs are for the long-term – they don’t depend on new products, or new ideas, every year – all they need is more people who need shelter, student housing, storage, mortgages, shopping centers, health care, and so forth.

(B)(N) BRK-B Berkshire Hathaway Incorporated Class B – Where’s the money?

And they don’t depend on the singular ability of one person, or even several persons, either.

The stop/loss (please see Figure 1.1 above) can always be used to protect our capital, but it’s difficult to apply if the companies are trading in the (N)-zone of investor uncertainty and stock price volatility.

But it’s easy to apply to the (B)-class companies that are trading at or above the price of risk, and so done, the managed portfolio of REITS returned +14% in 2012, +6% last year, and is up +9% so far this year, and we’re holding nineteen of the twenty-two companies, excluding only Plum Creek, Rayonier, and Ventas at the moment; please click on the links “(B)(N) S&P NYSE REIT World – Prices & Portfolio and Cash Flow Summary” for further details.

Lower Prices Than At The Wal-Mart, Today.

If the market sells us out at the stop/loss, we can expect to buy these companies back at lower prices if they’re still trading above the price of risk.

In aggregate, these companies paid $12 billion in dividends last year for a payout rate of 64.5% (which is below 90% because two of them, American Capital Agency and Hatteras Financial, lost $1.1 billion last year, but still paid dividends of $1.1 between them, and we have added the paid dividends back into the reported earnings per share (EPS)) and an aggregate dividend yield of 4.4% of which five were above 10% (and they also stand out for other reasons that we’ll discuss below in Exhibit 2) and four more were above 4.4%, and only three (Boston Properties 2.2%, Vornado Realty Trust 2.9%, and Essex Property Trust 2.9%) were between 2% and 3%; please see Exhibit 1 above for further details.

But what about the yield?

Yield Up, Income Down – Probably Not.

The “yield”, of course, is a two-edged sword because the yield will automatically increase if the stock price goes down – for which there are as many reasons as there are investors and their money – but if we’re buying at low prices, then our yield (and income) will always look good to us, unless the company’s earnings falter or it goes into bankruptcy, which is unlikely for all the companies.

But should we also expect that our income will go up or down as the stock price changes? That becomes an important question if, for example, we buy a portfolio of REITs for $10 million and expect an income – perhaps a real one, adjusted for inflation – of $1 million per year for an eternity if necessary.

On balance, excluding the possibility of gross or erratic management, the answer is no – we should not expect our income to fluctuate with the stock price of a REIT – because a well-managed REIT is always working both sides of the street, both the equities market and the debt market for the sources of its funding, or its income, and if it can’t make money on one side, it can expect to make money on the other.

For example, since the current short-term interest rates are low, the REIT can borrow money at low rates and use the money to buy assets which are typically real properties or mortgage-backed securities, and leverage the assets to borrow even more money short-term, and repeat the cycle as often as is feasible and reasonable with respect to the assets that it’s buying. And it can sell its own equity into the market to raise cash if that is reasonable, or necessary, or if its borrowing costs are too high to make a profit and it needs to live on the income that it’s acquired.

Moreover, if stock prices are systemically down, our yields will make them attractive purchases and tend to boost the stock price; and if the stock prices are generally high, as they are now, the REITS might increase their payout rates in order to differentiate themselves in the stock market, or sell more of their equity into that market.

And a good track record of paying consistent dividends to its shareholders will bolster our confidence in the management, but no management lives forever, so we also need to develop some “structural” indicators that will distinguish one REIT from another, regardless of the stock price and its purported yield.

And there might not be enough productive properties for REITs to manage and produce the higher yields that are expected of them because real properties are scarce resources.

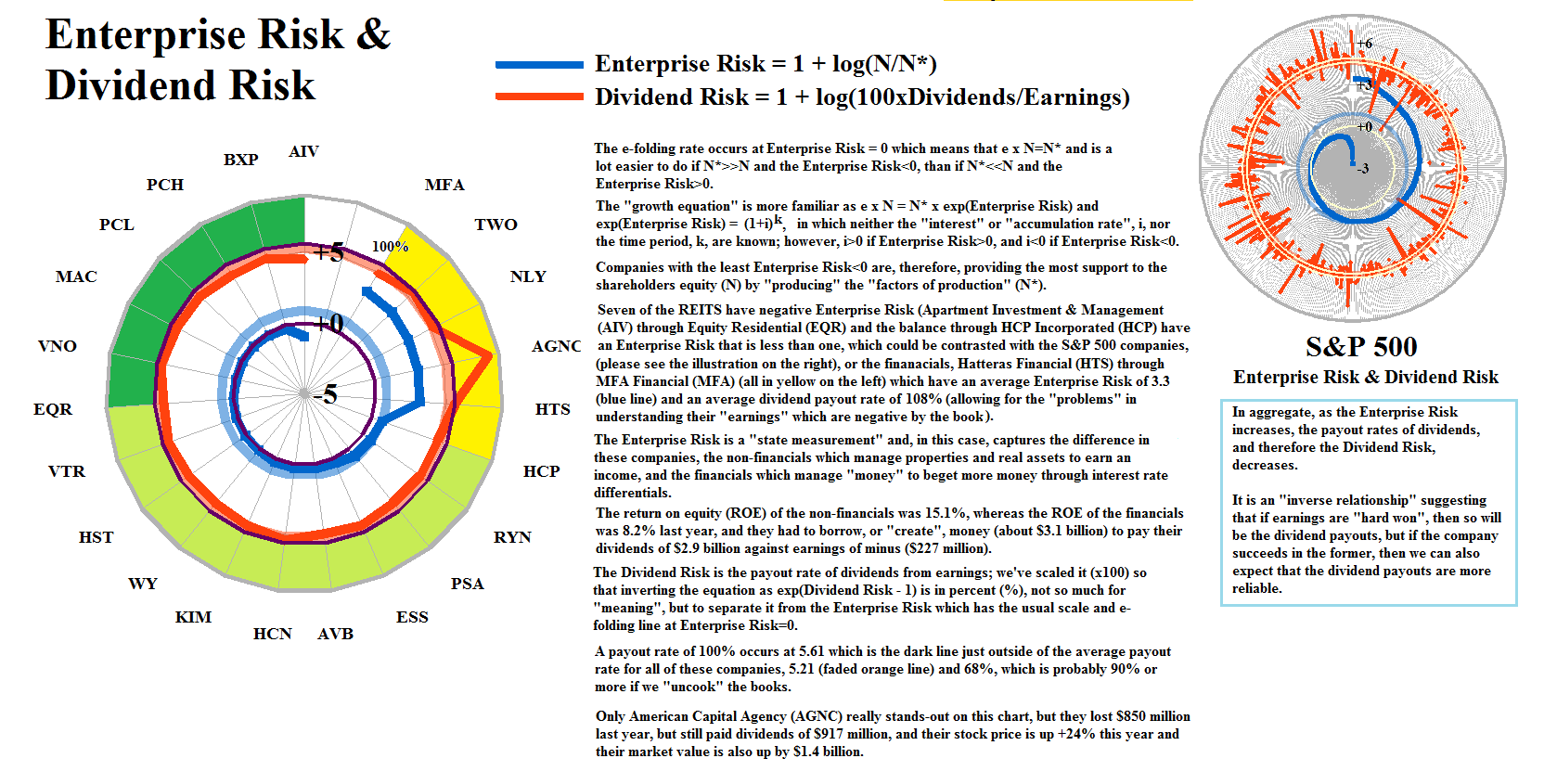

Enterprise Risk & Dividend Risk

The “Enterprise Risk” is the take-up rate for the “factors of production” (N*) to support the shareholders equity (N), and therefore, the earnings; and the “Dividend Risk” is the payout rate of earnings to dividends (90% for these companies), and we would think that a low Enterprise Risk would also provide us with a low Dividend Risk – and that is true, even remarkably true for these companies; please Exhibit 2 below.

Exhibit 2: S&P NYSE REITS Enterprise Risk & Dividend Risk

Figure 2.1: S&P NYSE REIT – Enterprise Risk & Dividend Risk

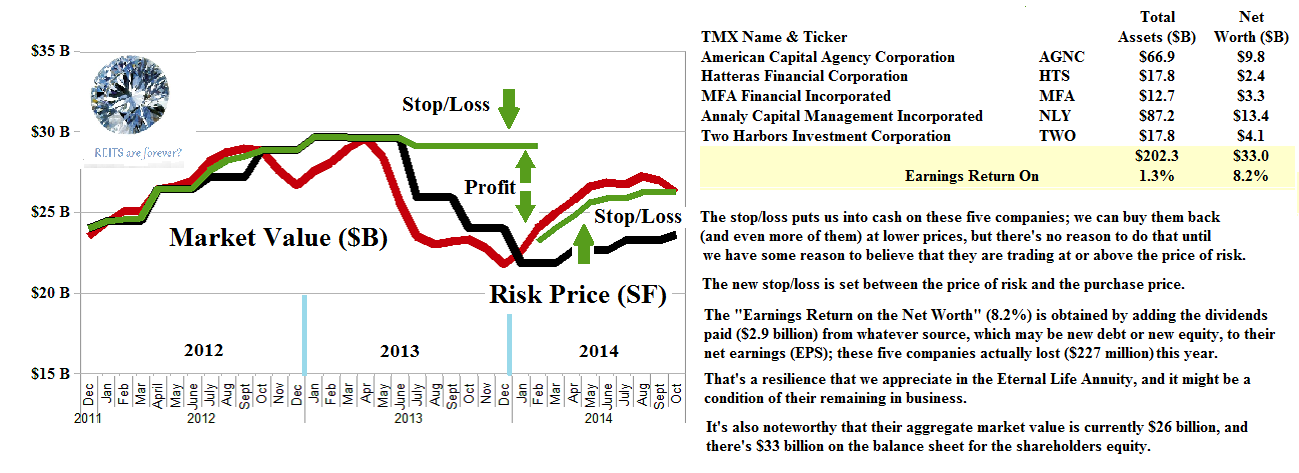

Five of the companies (American Capital Agency, Hatteras Financial, MFA Financial, Annaly Capital Management, and Two Harbors Investment Corporation) stand-out on this chart, and they all stand-out in the same way and to the same degree – they are all investment companies, and they all invest in mortgages, and unlike the other REITS, they don’t have tangible property, or inventory, to manage.

Exhibit 3: (B)(N) S&P NYSE Mortgage REITS – Fundamentals

(B)(N) S&P NYSE Mortgage REITS – Fundamentals

Figure 3.1: (B)(N) S&P NYSE Mortgage REITS – Risk Price Chart

And their dividend yields are currently all in the double-digits (10%-12%) even though their stock prices are up +21% this year; the market value is up by $4.5 billion and they paid $2.9 billion in dividends, even though they lost ($227 million) in aggregate and, possibly, “bought” their dividends in the stock market by issuing new shares; and their return on the shareholders equity is only a middling 8.2% in contrast to the S&P 500 companies (13.9%) and the non-financial REITS (15.1%); please see Figure 3.1, on the left, and Exhibit 3 above for more details.

But all five of them are currently in the (B)-class, and that portfolio is up +19% so far this year; please click on the links “(B)(N) S&P NYSE REIT World – Prices & Portfolio and Cash Flow Summary” for further details.

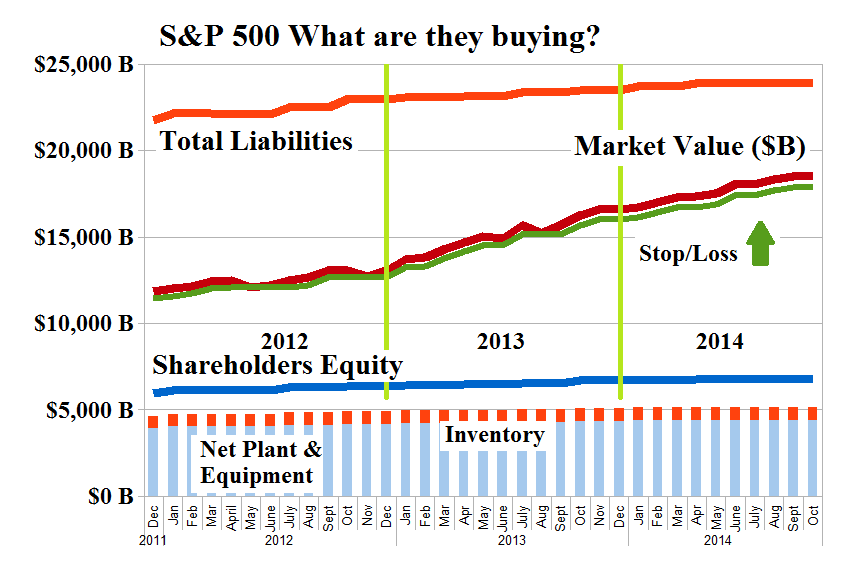

The Stock Market is Always Cheap

Figure 2: S&P 500 What are they buying?

Investors have bid up the S&P 500 companies by more than 50% since 2012, but what they’re buying hasn’t gone up by nearly that much in its “production value”; please see Figure 2 on the right.

And some investors – but not all – will “win” if they sell-out before the market crashes, whenever that is, and buy back even more of the same stocks with more money at lower prices; please see our Post “(B)(N) BlackRock’s Broken Bond Market” for more information on how to avoid the “Bear Embrace” that ritually brings the market down, and crushes the “unprepared”.

The Price of Risk

But that’s how it works and why the market is called a “Bear Market” (hungry) and a “Bull Market” (feisty), because the only “fair price” is the price of risk – 100% capital safety, 100% liquidity, and a hopeful but not necessarily guaranteed return above the rate of inflation – and if the investors can’t get it from the companies in the stock market, as a return of earnings and dividends, soon enough, fast enough, or big enough, they try to get it from each other, which is the only other place that it can come from if it doesn’t come from the companies.

As the market stands now, the most recent investors in the “Bull Market” automatically receive 50% less for their money, and it will be a real 50% less if they are unable to protect, or defend, the prices that they paid.

But if we are able to defend our prices, then the stock market is always cheap, and the only “stock price” that we might believe in, is zero, because at that price, or figuratively close to it, it becomes an ownership issue, and of all of the earnings, and of all of the future earnings.

But we can read the market fiction, and understand the story, if we look at “price” in the context of the Enterprise Risk by examining the Coase Dividend, and in the context of the market risk by understanding the relationship – if any – between the Enterprise Risk and the Dividend Yield, and the Dividend Risk and the Dividend Yield for these companies.

Figure 3: Return on Equity and Debt Courtesy: GMO LLC

Our object is not to discover, or justify, a stock price, but merely to identify possible arbitrage opportunities within the prices that are being established by the market, without regard to “history”, or a “judgmental value” because we don’t know of any for which there is a proof and dividends do seem to matter for which the obverse is argued; please see Figure 3 on the right and Exhibit 4 below.

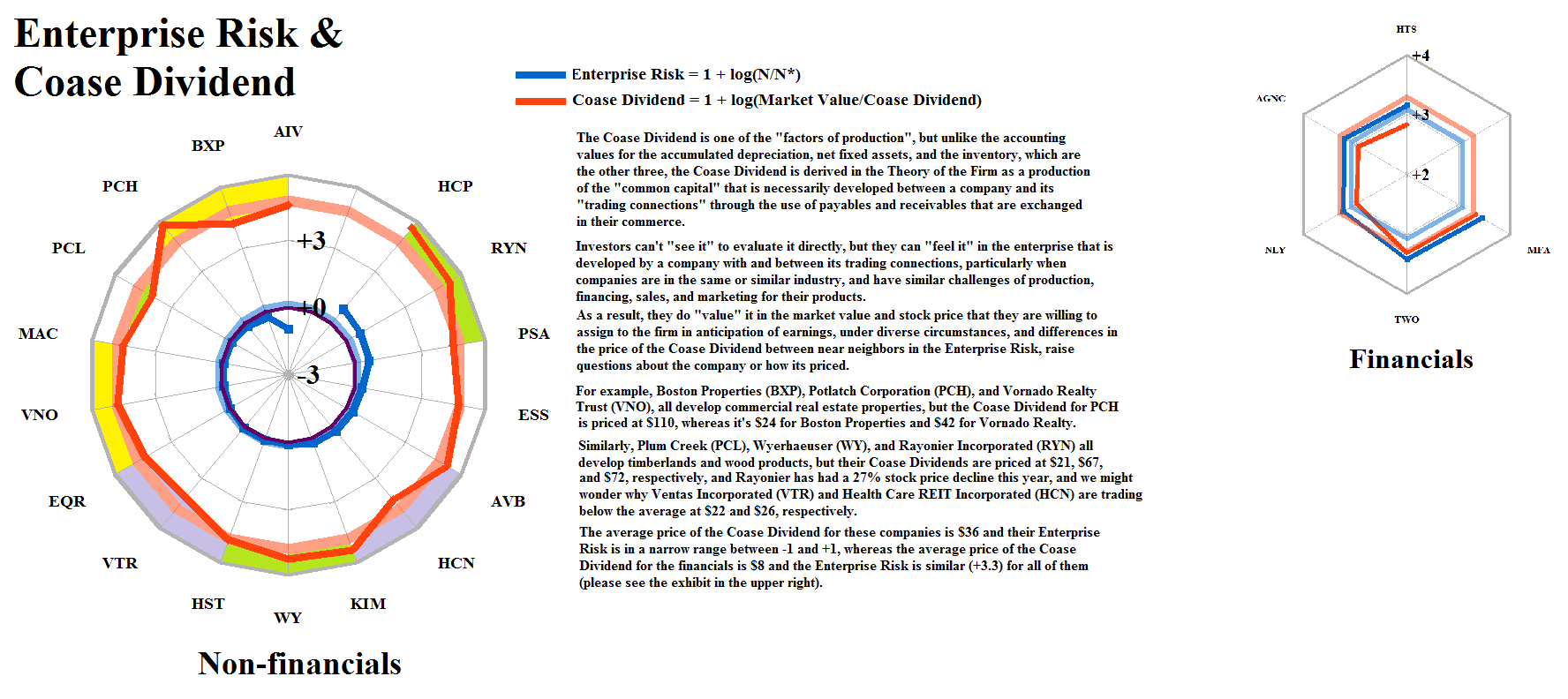

Exhibit 4: S&P NYSE REITS – More Money, Please – Non-financials

Figure 4.1: S&P NYSE REIT Non-financials – Enterprise Risk & Dividend Risk |

Figure 4.2: S&P NYSE REIT Non-financials – Enterprise Risk & Coase Dividend |

Figure 4.3: S&P NYSE REIT Non-financials – Enterprise Risk & Yield |

Figure 4.4: S&P NYSE REIT Non-financials – Dividend Risk & Yield |

We note in passing, so to speak, that the Perpetual Bond™ is also an “eternal life annuity” and a financial REIT in all but name – 100% capital safety, 100% liquidity, and a hopeful but not necessarily guaranteed return above the rate of inflation.

For more information on the “Five Equations of State”, and an introduction to the terms that we have used here, please see our Post “(B)(N) Through the Looking-Glass“, and for the really hard rocks, the Theory of the Firm which is based on The Process.

And for more information on real “risk management” in modern times and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary and “(P&I) Dividend Risk and Dividend Yield“, and our recent Posts “(P&I) The Profit Box” and “(P&I) The Process – In The Beginning“; and we’ve also profiled hundreds of companies in these Posts and the Search Box (upper right) might help you to find what you’re looking for, such as “(B)(N) TLM Talisman Energy Incorporated” or “(B)(N) ATHN AthenaHealth Incorporated” or “(B)(N) PETM PetSmart Incorporated“, to name just a few.

And for more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice. And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

And for more on what risk averse investing has done for us this year, please see our recent Posts on “(P&I) The Easy (EC) Theory of the Capital Markets” or “(B)(N) The Easy (EC) Theory of the S&P 500“, and the past, The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.

{kind=link}

{kind=link}