(P&I) Extreme Economics – World Oil (The Company)

Figure 1: What were you drinking in 1965?

Drama. World Oil (the companies) is selling at a 20% discount to the “peak oil” of last year and some of the companies for less than that and the question is: is this our Coca-Cola moment aka +30,000% in fifty years?

In like fashion, does it make sense for us to just buy and hold a broad portfolio of World Oil in every country and every currency that produces it as an alternative to a portfolio of IPOs, leverages and beverages, restaurants, brands, and telephones, for example?

It’s a good question for pension plans and endowment funds because they have a 50-year horizon and none of them are talking about +30,000% in that lifetime although they can do it at 12% per year (which they do talk about) if they don’t have to spend any of our money on us.

However, after inflation, it doesn’t look all that good (please see the illustration in Figure 1 above) and great piles of money always disappear in fifty years so we think that a better approach is to just make a living every year from the money that we have invested and eating more frequently than just once (maybe) in fifty (long) years.

The Company Fleet at anchor today in Atlantic Bay.

And so the question really is: can we expect to make a living by owning a global interest in the World’s “favorite drink” – hydrocarbons of all sorts across all currencies and all countries that are producers of hydrocarbons (which we’ll just call “oil” from now on)?

But shouldn’t we worry about revolutions and nationalizations in the next fifty years? No, it is they who need to worry and Iran, Iraq, Algeria, Mexico, Colombia, Venezuela, and OPEC are good examples of that in their struggles to get back into the market economy with their oil where it might be wanted and the Company Fleet that is carrying their oil is anchored in Atlantic Bay today waiting for buyers – low prices and a reliable supply are good selling points whereas “blood oil” is not.

But what about currency exchange; aren’t the Yen and the Ruble and the Rupee and so forth “more likely” to lose their value against the US dollar or gold? No, it is more likely that the US dollar will lose its value against the basket of foreign currencies that we’re talking about (please see Figure 2 below) and if we find some other source of energy other than hydrocarbons in the next fifty years, it will probably be “manual labor” with clubs.

On the other hand, if World oil consumption per capita increases by just 5% in the next fifty years, the increase will be more than the US is using now.

But can we live with a 4% dividend yield (please see below)? We don’t know but it’s a much better deal than, for example, Berkshire Hathaway which doesn’t pay a dividend but relies on us to take profits and sell our stock if we need money; please see our Post “(B)(N) What’s A Girl To Do?” (Figure 2) for how that works out.

The pursuit of an income for us? Courtesy: Amarjeet Productions

Moreover, we don’t have to “worry” about the markets – we’re not in them – and we don’t have worry about “portfolio managers” who are garnisheeing our income every year because this portfolio can be run by an accountant and the less they know about the “market” the better it will be for us and they can also buy forward options on currencies to protect our income as if it were a “commodity”.

The Company

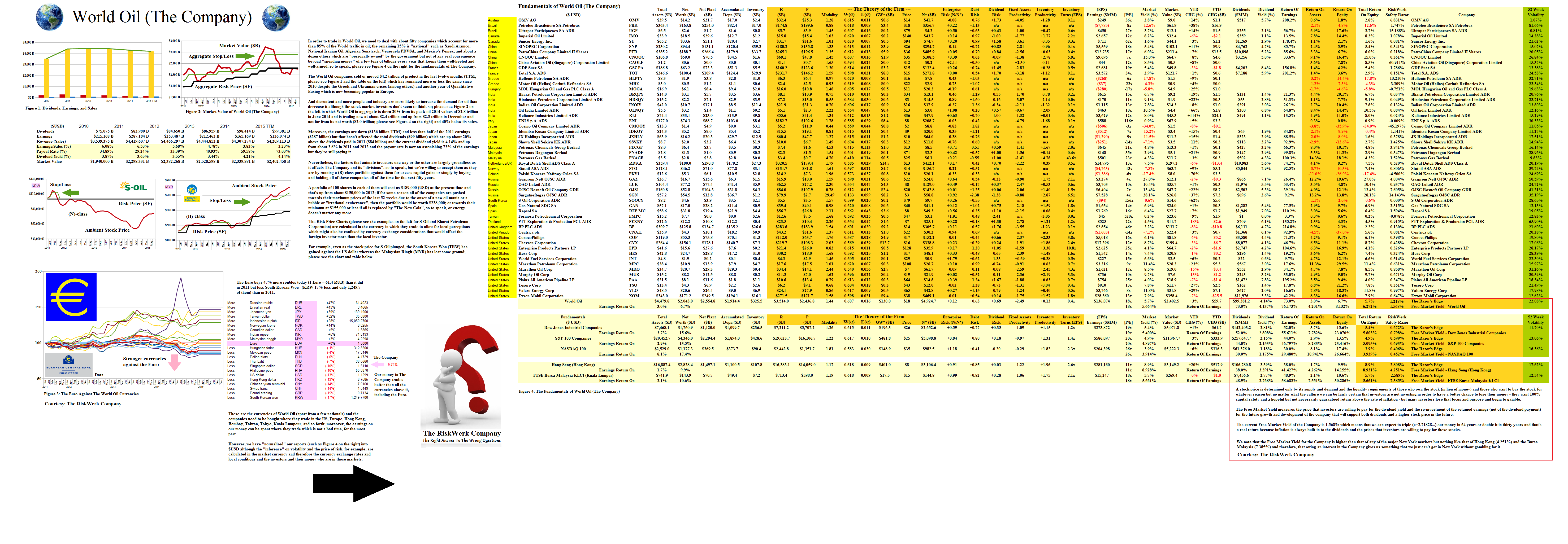

More than 85% of the World’s oil is handled (produced, refined, or moved) by just fifty companies and the balance of it is pumped from about a dozen nationals who don’t really use much oil and rely on us to find it, move it, refine it, and use it.

Figure 2: The Free Market Yield of World Oil (The Company)

At the current prices, the dividend yield of “The Company” is 4.14% and the Free Market Yield is 1.568% which means that we can expect a real return (in excess of inflation) of 1.568% per year and to triple (e=2.71828…) our real money in 64 years or double it in thirty; moreover, although the Free Market Yield varies inversely with the ambient stock prices, it’s a hard number to move for fifty companies in a market of this size that does about 5% of the World’s GDP every year; please see Figure 2 on the right (and click on it and again to make it larger as required).

Nevertheless, the number (the Free Market Yield) is moving and it’s down about 40% from its value in 2011 (please see Exhibit 1 below for more details) and it’s been moving downwards consistently from year-to-year no matter what the market prices; to raise it, the Company needs to improve its earnings and re-investment rate (retained earnings) but that’s not entirely material to us as investors because we’re firstly concerned about the dividend yield and the possibility of capital gains year-to-year for the next fifty years.

To do better than the Free Market Yield in the long- and short-term, we need to work the (B)-class portfolio against the volatility-based investors who begrudge us a living and are in and out of the market as it suits them according to the anxiety or excitement of the day – so come to us, dear fellows and huckleberries, and we’ll take your money and you won’t have to “worry” about it anymore; please see Exhibit 1 below for more details (and click on it and again to make it larger as required).

Exhibit 1: The (B)-class Portfolio in The Company

Figure 1.1: World Oil – (B)-class Portfolio

For more information and examples on the Free Market Yield and the terms that we have used above, please see our Posts “(P&I) The Dismal Equation (Ecclesiastes 9:1)” and “(B)(N) S&P 100 Volatility Risk and The Full Moon” and “(B)(N) NASDAQ 100 Volatility and The Stone Bunnies“ and for an introduction to The Barometer “(B)(N) What’s A Girl To Do” or “(P&I) The Swiss Franc Debacle“.

And for more information on real “risk management” in modern times and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary and “(P&I) Dividend Risk and Dividend Yield“, and our recent Posts “(P&I) The Profit Box” and “(P&I) The Process – In The Beginning“; and we’ve also profiled hundreds of companies in these Posts and the Search Box (upper right) might help you to find what you’re looking for, such as “(B)(N) TLM Talisman Energy Incorporated” or “(B)(N) ATHN AthenaHealth Incorporated” or “(B)(N) PETM PetSmart Incorporated“, to name just a few.

And for more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice. And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

And for more on what risk averse investing has done for us this year, please see our recent Posts on “(P&I) The Easy (EC) Theory of the Capital Markets” or “(B)(N) The Easy (EC) Theory of the S&P 500“, and the past, The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.