(P&I) The World Trader’s Almanac – China

Capital Gains Are Not An Income

Drama. The Chinese Yuan, the Renminbi (CNY), is as strong as the US dollar and has kept pace with it even as other currencies have faltered significantly; for example, merely holding the Yuan or the US dollar as near cash or in their government bonds or even in their stock markets (please see below) has given us a 10% to 30% “capital gain” against the Euro, the British Pound Sterling (GBP), the Japanese Yen, and the Canadian dollar in the last twelve months.

The reasons for this are the same and easy to understand – the “demand” for the Yuan and the US dollar exceeds the “supply” and the reverse is true for the other currencies against them – but the causes are different and it’s natural that we should want to know how and when this might end and what we can do with our strong and “overvalued” currencies in the Yuan and US dollar before it does.

While We Were Out

Figure 1: The Price of Everything

While we were out last year or just counting our money, the price of everything that we used to buy while in Europe, Canada, Japan, and Great Britain, went up by as much as 30% depending on its US dollar or Chinese Yuan combined content; please Figure 1 on the right (and click on it and again to make it larger as required).

Because the value of the Euro (for example) has declined by 30% against the US dollar, the Euro area countries are under pressures of “price inflation” in so far as their products might rely on US materials and services and, therefore, they could demand a higher price in the local currency; and for quite another reason – the US dollar is a currency that can be used to buy up their businesses at effectively a 30% discount simply by converting US dollars (which have done next to nothing at home all year) into Euros; and for yet another reason – local businesses might not be able to raise their prices without losing business or market share so that they might have to reduce wages and employment in order to stay in business which is a “deflationary” consequence of “Producer Price Inflation”.

Moreover, the US dollar, Euro, Pound Sterling, and the Japanese Yen are the four “Reserve Currencies” of international trade but, obviously, three of them have lost significant value between the purchase of a product, its delivery a few months later, and the receipt of payment. How long should we expect that to last because every transaction that we did in Euros last year, for example, is now a “bargain” because it will cost more if we buy it today and that puts downwards pressure on the US dollar in order to maintain its trade and not foster substitutes or new competition.

Cheap Money and Dear Investments

One response of governments to their cheapening currency and deflationary economies is to try to drive new money from “savings” and “consumption” into “investment” in the stock market but they won’t be able do that by raising the yield on government bonds – it needs to be low or lower.

For example, the rate on bank deposits is already negative in Switzerland and Switzerland tried to maintain the value of the Swiss franc by guaranteeing the exchange rate against the Euro but before long, they called it a “tsunami” that wiped-out investors on the short-side but was a boon to consumers who saw the Swiss franc appreciate by about 20% against the Euro and a bane to the Poles who had their mortgages in Swiss francs and their income in Euros; please see our Post “(P&I) The Swiss Franc Debacle” for further details.

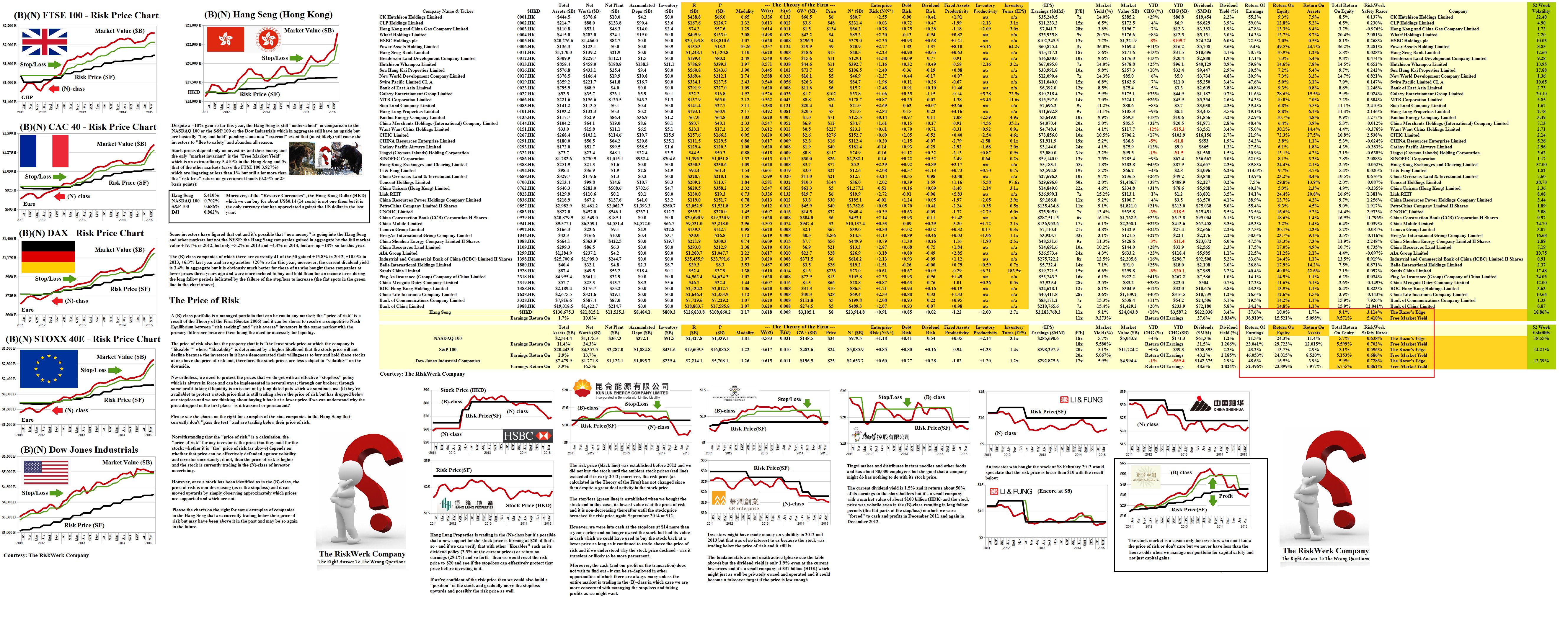

Figure 2: The Price of Everything In The Hang Seng

However, “cheap” money in terms of a low yield and low investment return on government bonds has had the desired effect in the US and more recently in the Euro area countries (please see Figure 2 on the right) but it hasn’t worked in China, Japan, or Canada to the same effect because the consumers are tending more to buy “properties” (real estate and houses) at high and inflated prices rather than investments in the stock market and they are borrowing the “cheap” money in order to do it – which is a “tsunami” in the making should the interest rates on borrowed money rise or the demand for houses wane; and these investments are about “capital gains” and not about an “income” (money and sudden wealth notwithstanding).

Another solution, of course, is to neither borrow money nor rely on an increase in the interest rates on bonds for an income but rather to invest in the income and capital gains of the equities market – but there aren’t many investors who know how to do that without assuming “risk” as “volatility” even though these markets are as “risk-free” as government bonds – but that’s their choice and has more to do with opportunism (and gambling) than investment for an income and capital safety.

Capital Gains Are Not An Income

Although it’s a heresy to say it, “capital gains” don’t have an economic “value” other than to weed-out the bad investors from the good and we can readily imagine that the “best” investors are eventually concerned not with more capital gains (it’s just more money and we already have lots of it) but with capital safety and obtaining an income on our money that we might not need to spend it to pay our bills.

If we are in a “deflationary economy” then the price of an income will tend to rise as it has in the US during the last several years and has recently started in the Euro area markets (please see Figure 2 above) and although we might be able to make lots of money by taking capital gains, we have to sell our stocks in order to do it and the price of an income isn’t getting cheaper and the World isn’t getting “larger”.

China has three multi-trillion dollar equity markets, one in Hong Kong (the Hang Seng; please see Figure 2 above) which is readily available to foreign investors and two others in Shanghai and Shenzen that are more restrictive of foreign capital investments and for which many of the companies are owned or controlled by the Chinese government.

The Hong Kong Dollar (HKD) currently trades at a 20% discount to the Chinese Yuan (CNY) but it has lost considerable ground from par value in 2005-2006 which we must attribute to an “inflationary economy” in China relative to a “deflationary economy” in Hong Kong as if affects the Hong Kong dollar relative to the yuan and makes it more “valuable”.

In other words, the yuan is “overvalued” (and “inflated”) because the value of the yuan as it trades against the Hong Kong dollar (and, therefore, against other international currencies) is maintained by “other means” as in the case of Switzerland (above) and should that support falter today (or tomorrow) the value of the yuan against the $US will join the other currencies such as the Euro, the yen, and the British pound.

However, the Chinese Yuan is a de facto “Reserve Currency” simply because of the trade – China’s world trade is about $7.1 trillion and nearly twice that of the US ($4.8 trillion) in international units of purchasing power parity (PPP) – if the Chinese Yuan is entered into the “Reserve Currencies” then the demand for it will increase even further and support the “worth” of both the yuan and the Hong Kong dollar.

Moreover, in our view, the US should not concern itself with a monopoly on “global hegemony” and “global human rights” but with survival as new trade blocs emerge in the Eurasian countries of the Euro area, Russia, China, India, and Southeast Asia; please see Exhibit 1 below for the “transparent” details (and click on it and again to make it larger as required).

Exhibit 1: The Waning West and The Rising Sun

Figure 1.1: The Waning West and The Rising Sun

For more information on the Free Market Yield and the terms that we have used above, please see our Posts “(P&I) The Dismal Equation (Ecclesiastes 9:1)” and “(B)(N) S&P 100 Volatility Risk and The Full Moon” and “(B)(N) NASDAQ 100 Volatility and The Stone Bunnies“ and for an introduction to The Barometer “(B)(N) What’s A Girl To Do” or “(P&I) The Swiss Franc Debacle“.

And for more information on real “risk management” in modern times and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary and “(P&I) Dividend Risk and Dividend Yield“, and our recent Posts “(P&I) The Profit Box” and “(P&I) The Process – In The Beginning“; and we’ve also profiled hundreds of companies in these Posts and the Search Box (upper right) might help you to find what you’re looking for, such as “(B)(N) TLM Talisman Energy Incorporated” or “(B)(N) ATHN AthenaHealth Incorporated” or “(B)(N) PETM PetSmart Incorporated“, to name just a few.

And for more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice. And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

And for more on what risk averse investing has done for us this year, please see our recent Posts on “(P&I) The Easy (EC) Theory of the Capital Markets” or “(B)(N) The Easy (EC) Theory of the S&P 500“, and the past, The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.