(P&I) Who will cast the first stone?

Figure 1: S&P 500 and Inflation

Drama. Die-hard bond investors are waiting, and waiting, for a return to the “old days” when government bonds gave us 5%, 8%, and even 12%, and there was no risk to the coupon and no risk to the capital – but what about the income?

Our 12% bond loses its luster if the rate of the inflation rises to 15%, over which we have no control, and to get the 15% bond, or liquidity, we need to sell our 12% bond at a discount for a 3% capital loss so that we have less money to buy the 15% bond, or to pay our pensioners, and we will only get it back if inflation declines – over which we have no control; please see Figure 1 on the right, and for the longer story, the Post from which it came “(P&I) One economist at a time“.

The bottom-line for us, as actuaries, is that government bonds, or any interest-rate dominated investments, are “riskier” than stocks, because only the coupon and the capital are effectively guaranteed, but the income isn’t, and depends on interest rates to which we can respond, and mitigate our “surprise”, but over which we have no control.

And it’s in the evidence, in the failure of our pension plans and endowment funds, for example, that investors have paid a very high price for the “guaranteed” cash flow that doesn’t guarantee its worth.

Government bond investors in the US dollar, the yuan (China), and the Euro, face that problem now because the rates of inflation in the US and China are less than 2%, 1.7% and 1.6%, respectively, and the Euro-area countries have been flirting with zero inflation, and even deflation (as did the US in 2008-2009), with no place else to go but up.

Moreover, the price of an income in stocks is up +50% since 2012, and that creates a “double-whammy” for the die-hard bond fans, done in by Miss Moneypenny, so to speak; please see the aforementioned Post and for even more chilling news, “(B)(N) The Stock Market Is Always Cheap” and “(B)(N) BlackRock’s Broken Bond Market“.

There is an enduring solution, and we’ve already described it in these Posts, but to get it, we need to cast-off some sixty years of investment folly; please see below.

Who will cast the first stone?

Guns, Germs, and Steel by Jared Diamond, 1997, A Scientist

The historical, usual, end to a downwards drift in the return on government bonds, and recession, depression, and deflation, is a declaration of war on our neighbors, or civil war on our friends, and the arms trade is an ongoing, steady business, for all the countries that we love – the US, Britain, France, Russia, and China – and then there are those who can make and sell an AK-47 knockoff, rocket launcher, grenade, or drone, or bullets by the bucket.

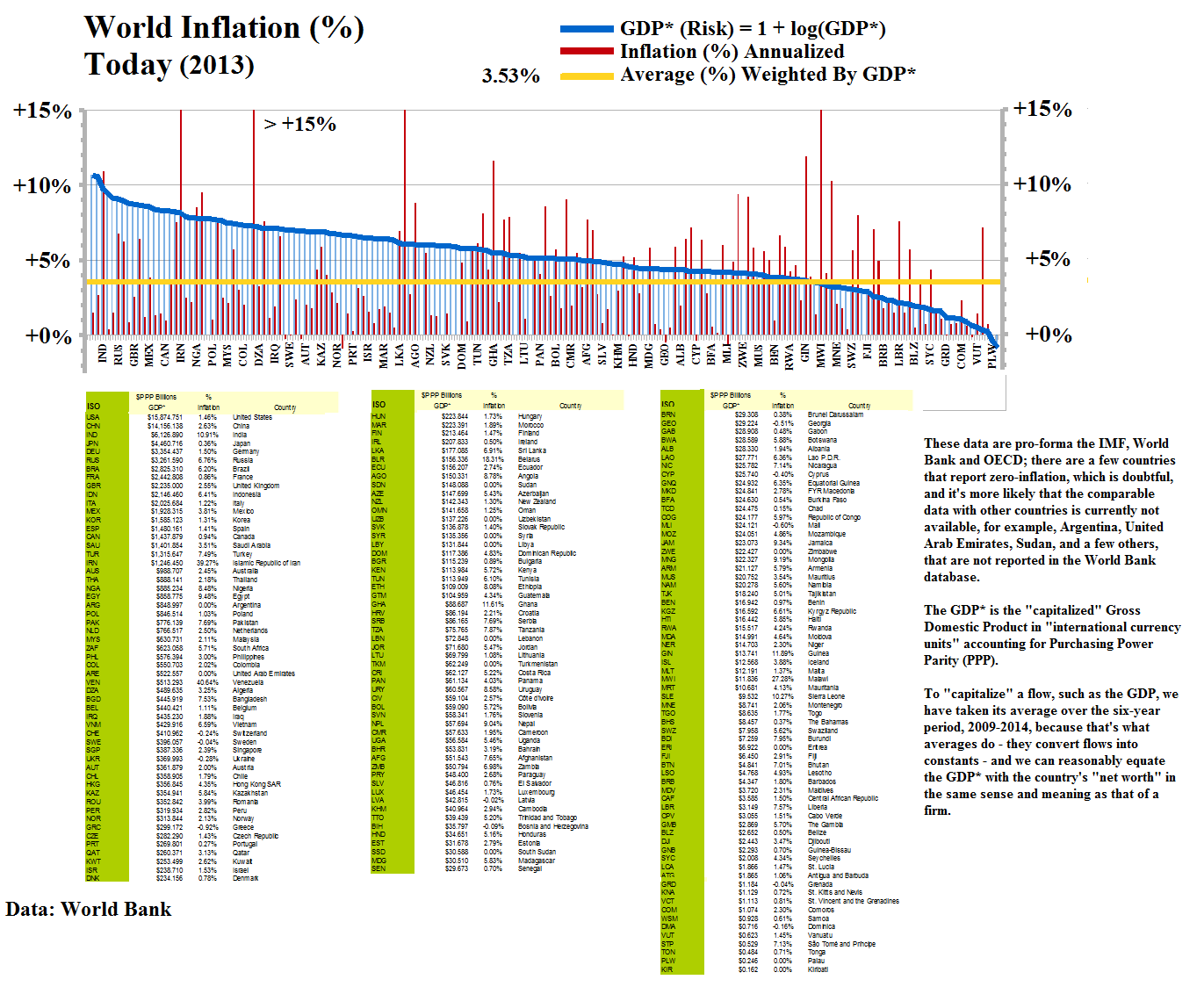

Exhibit 1: World Inflation & GDP*

Figure 1.1: World Inflation & GDP*

The chart on the left shows the “standing” (there is no relationship) of inflation by the capitalized Gross Domestic Product (GDP*); please click on it make it larger, and again if required.

The average rate of inflation in 2013 was 3.53% per year (the yellow line), weighted by the GDP*, and among those economies with a “net worth” (GDP*) in excess of $1 trillion, Iran stands-out with a rate of inflation of 39%, followed by Venezuela (41%), Belarus (18%), and Malawi (27%) (on the far right).

Of the $93.5 trillion GDP* and 175 countries in the table, 105 countries and $66.6 trillion is currently under less than 3.53% inflation; and 70 countries and $26.9 trillion above that, in the local currencies; and there are 76 countries and $41.8 trillion for which the rate of inflation is less than 2%, including the United States, China, Japan, Germany, France, Italy, Spain and Korea; and a dozen countries with inflation less than 0% (deflation) including Greece, Georgia, Cyprus, Ukraine, Switzerland, and Sweden.

Exhibit 2: The Wheel of Fortune

Figure 2.1: The Wheel of Fortune

The Wheel of Fortune (Figure 2.1 on the left, please click on it to make it larger as required) grades the countries by inflation (the blue line) and also shows their “net worth” as GDP* (Risk) = 1 + log(GDP*) (orange line), and the Country Risk = 1 + log(GDP*/(GW*+Investment*+Savings*)) (purple line in the center); please see our Post “(P&I) The World Trader’s Almanac” for the definitions and full explanations, and “(P&I) The NYSE Mittelstand” for an application to “industrial America” treated as a “sovereign economy”.

The chart shows that no matter what country we live in (excepting GRC Greece, and a few others that are at high-noon and are deflationary economies), in the local currency, there are countries with less inflation and greater resources (GDP*) and/or less Country Risk, than ours – and we might think about investing our “cheap dollars, or yen, or yuan” and so forth, that are depreciating more rapidly due to our higher rate of inflation, in their “expensive investments” which are “cheap” in their currency, unless the government is offering us bonds with a return that is in excess of their rate of inflation; for more on that, and the subject of “inflation” and “cheap, expensive, or dear investments”, please see our Post “(P&I) One economist at a time“.

For example, we might think that the United States is in a class of its own because it has an inflation rate of only 1.46%, and a “net worth” GDP* (Risk) of $10.672 trillion (which is equal to $15.875 trillion = exp(10.672-1) in the units of Purchasing Power Parity (PPP $Billion)) which is the “biggest” in the world; but every country on the chart that is clockwise to it (and later in the day but before Noon), such as Vanuatu (1.45% and $0.526), Czech Republic (1.43% and $6.643), Spain (1.41% and $8.300), and so forth, has a lower rate of inflation, and in all of those countries (and there are 44 of them), either the government is paying a rate of interest on its bonds that is in excess of the local rate of inflation, or there is a “flight of capital” to “equity investments” similar to what is happening in the NYSE markets at the present time; please see, for example, our Post “(B)(N) What’s A Girl To Do” for a run-down on the NYSE big-caps.

To complete the example, both Canada and Korea are on that list; Korea has a lower rate of inflation (1.31%) and a lower Country Risk (+1.419) than the United States (+2.050); and Canada has a lower rate of inflation (0.94% at the time, 2013) and a lower Country Risk (+1.782); and although neither of those two countries is as “rich” as the United States, neither are they “impecunious”, and the “flight of US dollars” into Canada last year had a huge effect on the stock market; please see our Post “(B)(N) The Easy (EC) Theory of the S&P TSX” or “(B)(N) S&P TSX Rents (Canadian REITS)” for examples.

There are, of course, numerous other issues in foreign investment, and in a foreign currency, but the principle is that either the foreign government is willing and able to pay a rate of interest that exceeds the local rate of inflation, or their stock market (if they have one) will be “buoyant” because the investors there need to find a source of income that exceeds the rate of inflation, and such income is always “expensive” (in their currency) if the investors are boosting the stock prices because they have no place else to put their money where it might obtain a non-negative real return, and an income.

Exhibit 3: High Noon

Figure 3.1: High Noon

There are several countries at the top of the chart (at “High Noon”, Exhibit 3 on the left) which have very low and even negative (deflationary) rates of interest.

In such a country, “cash is King” because merely holding cash increases its purchasing power; however, that might not be enough to qualify as an “income” (without spending it) and, therefore, “investments” are at a premium because they can produce an income in excess of cash, and keep on producing it, which “cash” cannot do.

Investing in a foreign country is no less “tricky” than investing in our own, but (as in our country) we need reliable partners, employees, suppliers, and so forth, if our intention is to “own” the business.

A lot of that problem goes away if there is a stock market, but the methods of “equity analysis” that are required in the Capital Assets Pricing Model (CAPM) and Modern Portfolio Theory (MPT), have even less “relevance” to stock market investing in a foreign market than they do in our own, because the liquidity and transaction issues, for example, are not like those of the NYSE – where we have a “highway”, they might only have a “cobblestone” path, or just a “dirt road”.

But we can help the moneyed-classes with a different solution that also maintains the “natural order of things”, as they like it, but which is much less “taxing” than guns, germs, and steel, when the bills come due.

The Perpetual Bond™ and The Separation Theorem

The Perpetual Bond™ never loses on the capital and is always liquid – 100% capital safety and 100% liquidity – which makes it look like “money”, and it would be “cash” were it not for a hopeful but not necessarily guaranteed return above the rate of inflation; that is, a hopeful but not necessarily guaranteed non-negative real return that we have some control over.

The Separation Theorem

Something like that befuddles the economists who think – and apparently they all do – that there can’t be a “reward” if there is no “risk”.

But they are wrong, and they were told, long ago, that “volatility is not risk; it is volatility” (John von Neumann, 1947) and “volatility” has nothing to do with investment success that is more profound than “pinching our pennies” in a hard-scrabble market.

For more information on real “risk management” in modern times and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary and “(P&I) Dividend Risk and Dividend Yield“, and our recent Posts “(P&I) The Profit Box” and “(P&I) The Process – In The Beginning“; and we’ve also profiled hundreds of companies in these Posts and the Search Box (upper right) might help you to find what you’re looking for, such as “(B)(N) TLM Talisman Energy Incorporated” or “(B)(N) ATHN AthenaHealth Incorporated” or “(B)(N) PETM PetSmart Incorporated“, to name just a few.

And for more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice. And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

And for more on what risk averse investing has done for us this year, please see our recent Posts on “(P&I) The Easy (EC) Theory of the Capital Markets” or “(B)(N) The Easy (EC) Theory of the S&P 500“, and the past, The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.