(B)(N) The Dow Transports

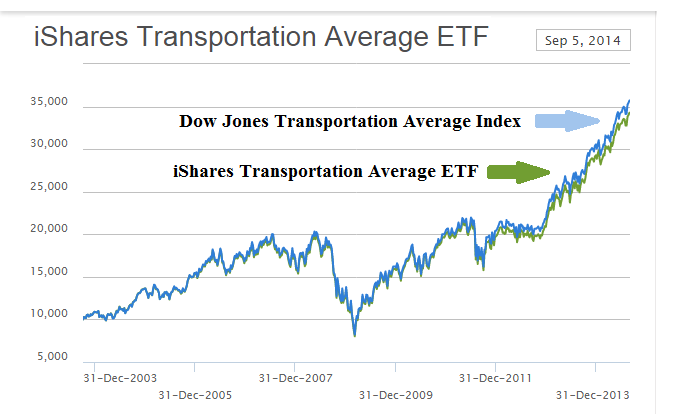

Figure 1: Rolling Stock Courtesy: Blackrock iShares Transportation Average ETF IYT

Drama. We love the transports – trucks, trains, ships and planes – because if it isn’t moving to a customer, then it isn’t moving at all.

As investors, we could just ride the rails forever by buying a “total return ETF” that invests only in the transports, but there aren’t many (please see Figure 1 on the right) and they don’t really do what we want – we want 100% capital safety, 100% liquidity, and a hopeful but not necessarily guaranteed return above the rate of inflation.

Instead, for which reason we don’t know, we get many of the usual confusion of transports, industrials, and maybe bonds, that does what it says that it will do – according to the prospectus – but doesn’t guarantee our capital – 100% capital safety – and might not flow-through any dividends that it might earn by actually buying those stocks with our money.

Liquidity is another issue because we might have to sell some of it at the wrong time, and we don’t have a choice in which part of it we sell – we indenture ourselves as “slaves to volatility” and factors (or fads) over which we have no control and might disagree with.

Are we there yet?

For example, if it’s not called an “investment”, do we usually buy everything that somebody wants us to buy? Do we hitch our wagon to somebody else’s horse? Do we buy a ticket to Chicago when we want to go to Muskoka? And some large investors (hedge funds) have a nasty business of trying to “play the market” and using an unsafe leverage in volatile markets, thereby distorting the values of what we have.

With reference to Figure 1 above, buying now would also seem to be a “risky” proposition, but that’s what’s happening, that’s what’s pushing up the prices – an excess of demand over supply at these prices for an abstraction.

But it’s not hard to “roll our own” and we can use the price of risk as our guide, and, in any case, whether we know the theory or not, the “price of risk” is what we paid for the stock, and it becomes our job to defend it, because there isn’t anybody else who is going to do that job for us, and there’s nobody who does it for an index – although we note that there is an active options market for IYT, as above, and we can buy and maintain insurance for our purchase for less than a few percent. But it’s still something that we need to do and it will raise the cost of our purchase.

Our Job is to Defend “Our Price”

You missed a spot – The Adventures of Tom Sawyer, 1876, by Mark Twain.

“Defending the price” is quite different from casting about in ETFs and mutual funds – which have no business defending the price and don’t do it – and it’s different even from “active investors” because we don’t care about “stock picking” – we don’t have to be either “bright” or “right” – but rather, we only care about “defending” what we do pick.

And that’s an easy job, much easier than the nine-to-five one that we might have, but would rather not.

The calculated price of risk is pro forma the theory of the firm, and it serves as a guide to separating the market into the stocks that we can defend, the (B)-class companies, and the others, the (N)-class companies, that are beset with investor uncertainty and volatility for factors that are not in our control, and for which the price is more difficult to defend because they are “overvalued” when we bought them – no matter how low the price, it’s more likely to go lower than it is to go up.

Exhibit 1: (B)(N) The Dow Transports – Fundamentals

(B)(N) The Dow Transports – Fundamentals – September 2014

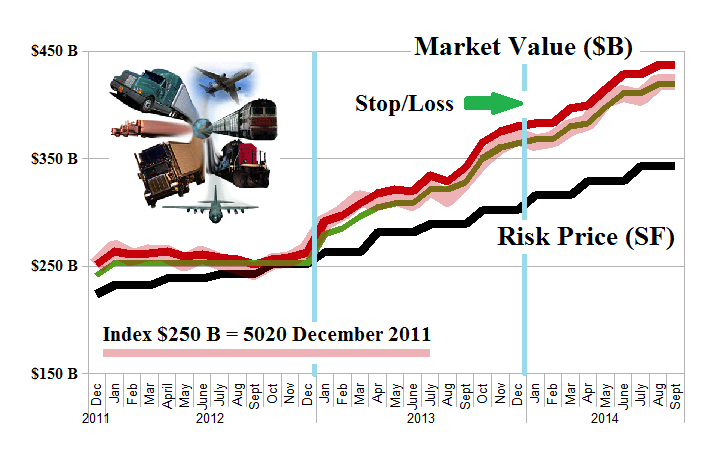

Figure 1.1: (B)(N) The Dow Transports – Risk Price Chart – September 2014

With reference to Figure 1.1 on the left, the Dow Transports were up +44% last year and are up another +15% so far this year.

They also paid $29.7 billion in dividends for a return of earnings of 23.4% and an aggregate dividend yield of 1.6%.

They are all currently (B)-class companies, but the actively managed portfolio returned +50% last year and is up another +30% so far this year, against index gains of only +14%; please click on the links (and again to make them larger if required) “(B)(N) The Dow Transports – Prices & Portfolio and Cash Flow Summary” for further details.

We’re also indifferent to tomorrow’s prices – or any future prices – because of the stop/loss (please see the green line in Figure 1.1) which we base on the demonstrated price volatility and our willingness to take profits at those levels, should other investors decide to bail.

Hence, an active defense is absolutely required; investors, in aggregate, demonstrate so much discernment that they are willing to price this entire industry at $440 billion, which is less than the current market value of Apple Incorporated ($600 billion) and similar to Google Incorporated ($400 billion), but more than Microsoft ($370 billion); that’s three-times as much, and up +20% this year, but the return of earnings was also 29% ($20.4 billion) with a dividend yield of 1.5%, and nobody rides an Apple to work … .

The Ecosystem

You have a wish?

“Ecosystems” are all the rage today, and for the next week or so, as Alibaba comes to market. But that’s only “new” to those who haven’t thought of it before – and there seems to be a lot of them. Absent “3D printers” in our homes, offices and factories, or “the genie in the lamp”, all of these products need to be delivered, which is where we come in, because, obviously, it’s not “cash & carry” on the Internet, at least not yet.

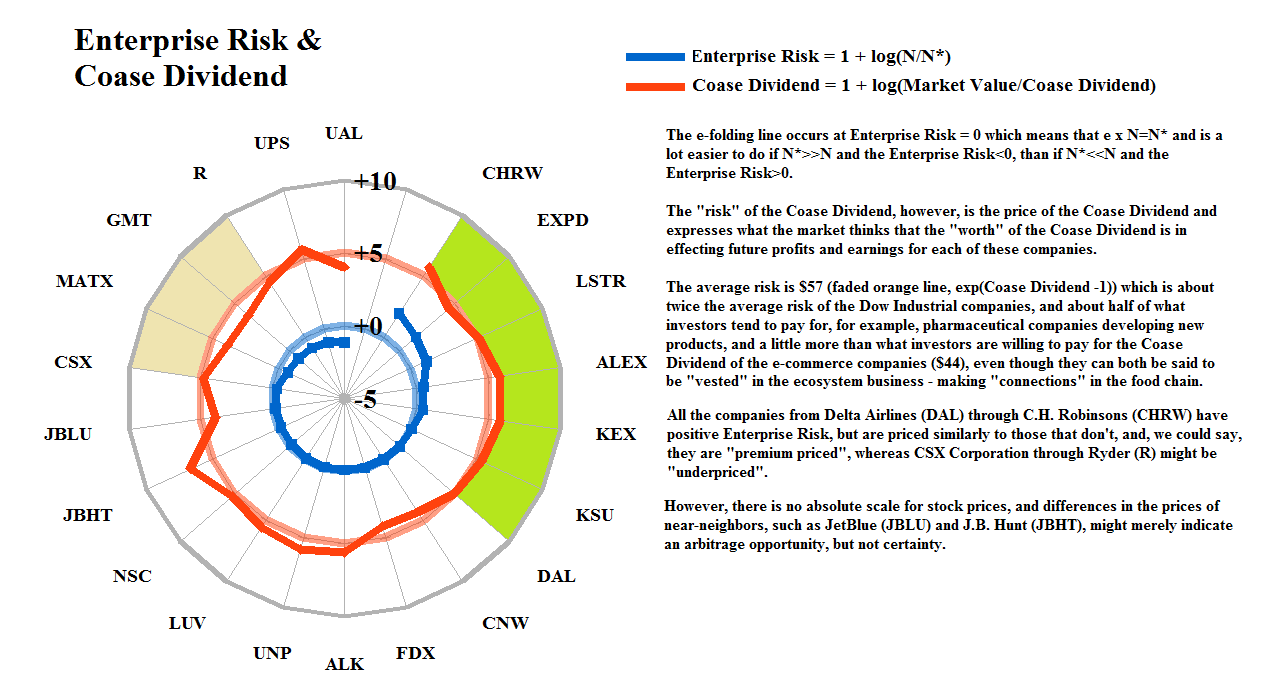

The “worth” of the ecosystem is the Coase Dividend which is “the balance sheet worth of the trading connections” and provably derived in Theory of the Firm.

Moreover, there is a surprising integrity between what investors are willing to pay for the Coase Dividend against the Enterprise Risk, and between the Dividend Risk and the Dividend Yield, and it is a surprise because “balance sheet”-values are used in determining the Enterprise Risk and the Coase Dividend, but more temporal earnings, and volatile and uncertain prices, are used in determining the other factors; please see Exhibit 1.2 and 1.3 below (and click on them to make them larger if required).

Figure 1.2: Dow Transports Enterprise Risk & Coase Dividend |

Figure 1.3: Dow Transports Dividend Risk & Dividend Yield |

Any chance that we might work this out?

However, we don’t pretend to have found terra firma or the Holy Grail, because prices will always be determined by investors – their ideas, and their needs, some of which are short-term and some longer – and their money.

Hence, if their goals are not the same as ours – which are merely safe, liquid, and hopeful – we need a defense.

For more information on the chart elements and the “Five Equations of State”, please see our recent Post, “(B)(N) Through The Looking-Glass“.

And for more information on real “risk management” in modern times and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary and “(P&I) Dividend Risk and Dividend Yield“, and our recent Posts “(P&I) The Profit Box” and “(P&I) The Process – In The Beginning“; and we’ve also profiled hundreds of companies in these Posts and the Search Box (upper right) might help you to find what you’re looking for, such as “(B)(N) TLM Talisman Energy Incorporated” or “(B)(N) ATHN AthenaHealth Incorporated” or “(B)(N) PETM PetSmart Incorporated“, to name just a few.

And for more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice. And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

And for more on what risk averse investing has done for us this year, please see our recent Posts on “(P&I) The Easy (EC) Theory of the Capital Markets” or “(B)(N) The Easy (EC) Theory of the S&P 500“, and the past, The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.

{kind=link}

{kind=link}