Microsoft, Apple, Google & The Tech Wars

Drama. The “Tech Wars” are finally over and the “losers” are the pioneers and main combatants – Microsoft, Apple, Google and to a lesser extent, Intel – which are now dealing with a “New World” of commodity pricing, diminishing margins and low prices and “free apps” from thousands of brilliant developers and firms worldwide that are following in their footsteps (New York Times, February 11, 2013, Apple, for the first time in years, is hearing footsteps and The Sydney Morning Herald, February 13, 2013, Why Google will pay Apple $1b in 2014.)

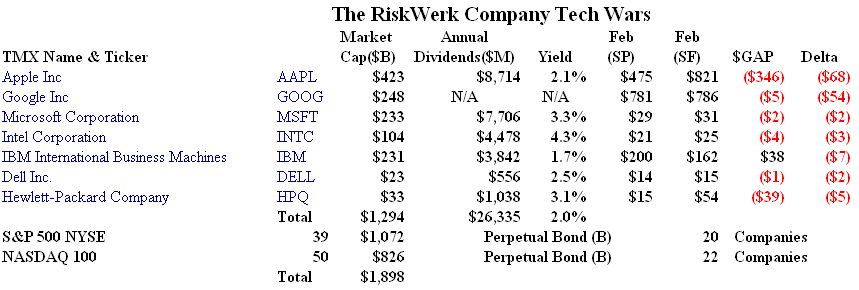

From our point of view, none of them (excepting IBM. Please see Exhibit 1 below and the following) have been “investor grade” since early last year and they are all in the “trading zone” (N) of volatility pricing and investor uncertainty. How bad can that be? Well, consider Hewlett-Packard and Dell which used to be #1 and #2 and the “go to” companies for retail and business personal computers and servers but now are struggling for survival in the new world of Lenovo, Samsung, Acer, Asus and many other companies selling timely and effective products in the new technologies. Notwithstanding the burbling and adoring press, for how long should we expect that Apple, Google, Microsoft and Intel will retain a market capitalization in excess of $1 trillion and pay dividends of $20 billion per year? Please see Exhibit 1 below and for another dissident view, CNBC, October 19, 2012, Why Google could disappear in 5 years.

Exhibit 1: The RiskWerk Company Tech Wars

(Please Click on the Chart to make it larger if required.)

The Chart shows that $1.3 trillion of the market capitalization of the “techs” is tied up in the notable seven but also that there are another 89 companies with market values in excess of $1 billion in the S&P 500 NYSE and the NASDAQ 100 with a total of $1.9 trillion in market capitalization and that 42 of them are currently “investment grade” (B) and can be included in the Perpetual Bond™. Please see our Post, Technical Fowls & Birds of Prey, September 2012, for more information or try the Search box for specific companies or terms.

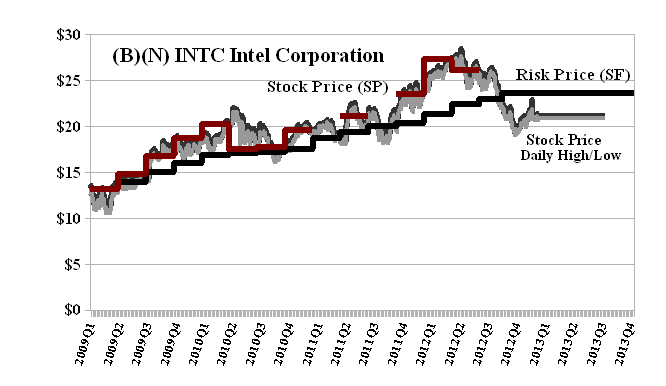

Exhibit 2: (B)(N) INTC Intel Corporation – Risk Price Chart

Intel Corporation is a semiconductor chip maker which designs, develops and manufactures new and advanced integrated digital technology products and general and specialized integrated circuits for industries such as computing and communications.

(Please Click on the Chart to make it larger if required.)

Exhibit 3:(B)(N) IBM IBM Corporation – Risk Price Chart

International Business Machines Corporation is a global and globally-integrated enterprise which creates business value for its clients and solves business problems through integrated solutions that leverage information technology and business production, marketing and knowledge requirements.

(Please Click on the Chart to make it larger if required.)

Exhibit 4: (B)(N) PCLN Priceline.com Incorporated – Risk Price Chart

Priceline.com Incorporated is an online travel company which offers its customers a range of travel services, including hotel rooms, car rentals, airline tickets, vacation packages, cruises and destination services.

(Please Click on the Chart to make it larger if required.)

Priceline.com is a “New World” company that could not exist without the consumer friendly capabilities of the Internet, the current Windows and OS operating systems, and the cheap and capable hardware that has emerged in the last ten years and even more so, in the last two years. Well-known competitors with a similar size and business model are Expedia (EXPE), Ctrip.com (CTRP) and Orbitz (OWW). The company has never paid a dividend but the market value is currently in excess of $35 billion, up from $12 billion two years ago and up from a post-IPO price of $10 per share in 2001 (please see Forbes, February 16, 2001, Pop Goes The IPO). The gross revenue is volatile but currently about $4 billion per year and the operating margin is 30% or so; the total assets are $6.2 billion and the shareholders equity is $2.6 billion with total liabilities of $5.7 billion; there are no inventories and the gross fixed assets are valued at under $200 million.

We only buy or hold the stock in the Perpetual Bond™ if the ambient stock prices summarized as the Stock Price (SP) (Red Line and a step-function) are above the Risk Price (SF) (Black Line, a step-function that is updated only as new balance sheet information becomes generally available), and for no other reason. With reference to Exhibit 4, we bought or held the stock between $100 and $250 in 2009 and again between $340 and $700 in 2010 through 2012 with the usual stop/loss or option “collar” in place (please see, for example, our Post, The Wall Street Put, August 2012). The current Risk Price (SF) is $660 and the ambient stock prices are at $700 with an estimated downside price risk due to the demonstrated volatility, of minus ($50) (please see our Post, Popoviciu’s Volatility, September 2012, for the details of that calculation). The company earned $20 per share last year and $10 per share the year before but investors can only make money from the stock by buying and selling it to each other.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

“Alpha-smart with 100% Capital Safety and 100% Liquidity”

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.