(B)(N) Crossroads at the G20

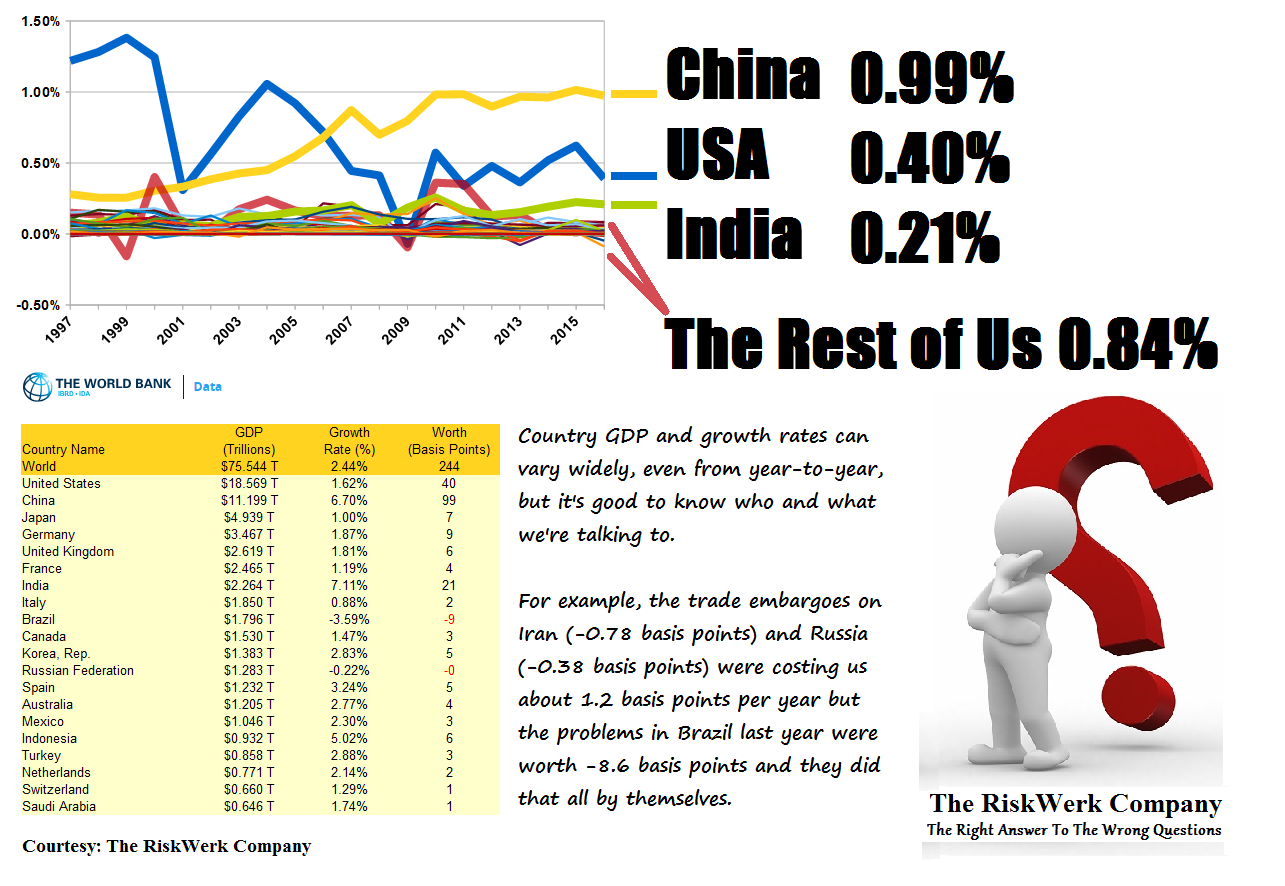

Figure 1: World GDP Growth

Drama. It’s 6AM and only midnight in New York, and the first podcasts on this quarter’s earnings are coming in from Paris and there will be eighteen more of those today; and, then, we will have the teleconferences in English, French, German, Italian, and Spanish until the market closes in New York. No Russian today, but Hong Kong, Shanghai, and Tokyo are on stand-by and pondering today’s closing prices (yesterday for them) and the 3rd shift has started working at L’Oreal.

Despite the anxieties of the market, there is no limit in the need for world production (GDP) because there are plenty of people who are in want of not only cosmetics but food, medicine, and capital goods and services which they would buy if only they could afford to buy them with their rupees, pesos, kwanzas, levs, or whatever short of gold and US dollars; nor is there any limit to US production or China or Russia production, and so forth, but the problem is that there is not enough real money to pay for it at G20 prices absent production at a loss (too low prices or too expensive a production) and a loss of capital.

However, 50% of the world’s GDP (USD $75 trillion) is produced in just four countries (the United States, China, Germany, and Japan) and 80% in the G20 and the other 20%, however heroic now and then, is a real mess mostly due to self-serving governments or punishing beliefs and, at best, they can only hope that we come to exploit them with our real money (Bloomberg, July 24, 2017, This Miner’s $190 Billion Tax Bill Would Take Centuries to Pay).

But if the world will gain only 2.4% and $1.8 trillion on its GDP (please see Figure 1 above), why is the stock market up by at least 10% and $8 trillion this year in real money and three times that much in the last five years for the same companies doing the same things in the same markets?

The reason is that the US dollar is the benchmark of global value and it is vastly overpaid compared to, for example, a miner in Tanzania who is probably working as a slave (ibid Bloomberg) and the investors in every market are spending it now in dollars, pounds, yuan, euros, and so forth, to buy an income at a “low price” in nominally high, or precious, US dollars which underwrite the capital of the world’s money as cash or investments but don’t guarantee its income.

If you like breathing fumes, fresh air will kill you.

For example, most investors and their money think that it’s quite reasonable to pay a [P/E]-multiple of 20× earnings for a stock because the market yield is 5% (the inverse of the [P/E]) and since most companies will pay out about 50% of their earnings as dividends, the investors can reasonably expect a 2.5% return every year and an annual income on their investment which is also capital safe and might have capital gains as long as the market does not write-down the stock price to below the purchase price; please see our Post, (B)(N) World Trade & Global Gold, for more information.

But the “production” is waning (please see below) and so is the shipping of it and our problem is not to worry about the problems of the companies and their production and a miserable 2.5% dividend return on them, but about the investors and their vast reserves of cash or money (including their investments at market prices) in search of an income; and how can we get their money before they don’t have any to spare?

For example, the US is currently trying to ease its trade deficit by selling more of its newly found oil self-sufficiency and by selling weapons and by promoting trade embargoes on countries such as Russia and Iran which might compete with it in both oil and weapons; such policies always end in war, for real or by proxy as is common now.

Should we be worried, then, like our friends above and scurry to our computers every day before dawn?

No. The market is doing all that it ever does and creating plenty of buying opportunities at the price of risk (please see below) and all that we need to do, and can do today, is to keep a wary eye on our selling price (which we call the stop/loss price) and take the appropriate defensive action at that time and not before.

Moreover, in order for money to have value, it needs to be spent, and spent again, and so forth, and the stock market is the biggest and fastest spender on the planet.

Our Money Is Much Better Than Yours

The market value of these nineteen companies has gone up by 90% since 2012 and the [P/E]-multiple has increased from 13× to the current 24× because the earnings are faltering and the prices aren’t.

And it’s fair say that the market is anxiously waiting for “news” today that it already knows but can’t do anything with it until it triggers their “robo-advisers” (computer programs) to buy, sell, or hold on this new old news; please see Exhibit 1 below.

Exhibit 1: Crossroads at the G20 – Risk Price Chart

I just said that we never gamble, mom.

And it’s also fair to say that the market should be concerned about what it perceives to be “rational behavior” because it does and will bet its money (your money, actually) on that outcome.

However, we never gamble and the (B)-class portfolio in these same companies has tripled our money since 2012, +215% and an average of 23% per year pro forma (that is, we did no work to speak of on the world’s clock) and we own fourteen of them now and we’re waiting for the outcome on the other five (including four of them today) with no capital risk at all and more idle cash – too much idle cash – than we started with.

Exhibit 2: Crossroads at the G20 – (B)-Class Portfolio – Cash Flow Summary

Exhibit 3: Why our money is much better than yours.

For more information on real “risk management” in modern times and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary and “(P&I) Dividend Risk and Dividend Yield“, and our recent Posts “(P&I) The Profit Box” and “(P&I) The Process – In The Beginning“; and we’ve also profiled hundreds of companies in these Posts and the Search Box (upper right) might help you to find what you’re looking for, such as “(B)(N) TLM Talisman Energy Incorporated” or “(B)(N) ATHN AthenaHealth Incorporated” or “(B)(N) PETM PetSmart Incorporated“, to name just a few.

And for more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice. And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

And for more on what risk averse investing has done for us this year, please see our recent Posts on “(P&I) The Easy (EC) Theory of the Capital Markets” or “(B)(N) The Easy (EC) Theory of the S&P 500“, and the past, The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”). The Canada Pension Bond®™, The Medina Bond®™, The Barometer®™, the Free Market Yield®™ and Extreme Economics®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.