(P&I) Our G20 Weekend and The Rush to India

Courtesy: IIF G20 Conference

Drama. The 2nd plenary meeting of the G20 Finance and Central Bank Deputies, Ministers, and Governors is taking place this weekend in Istanbul, Turkey, and the focus is on reinvigorating growth, reducing inequality, mobilizing private-sector support for infrastructure development, financial inclusion and new technologies, funding the SME (small to medium economies), financial globalization, regulatory reform, and the Business 20 (B20) agenda.

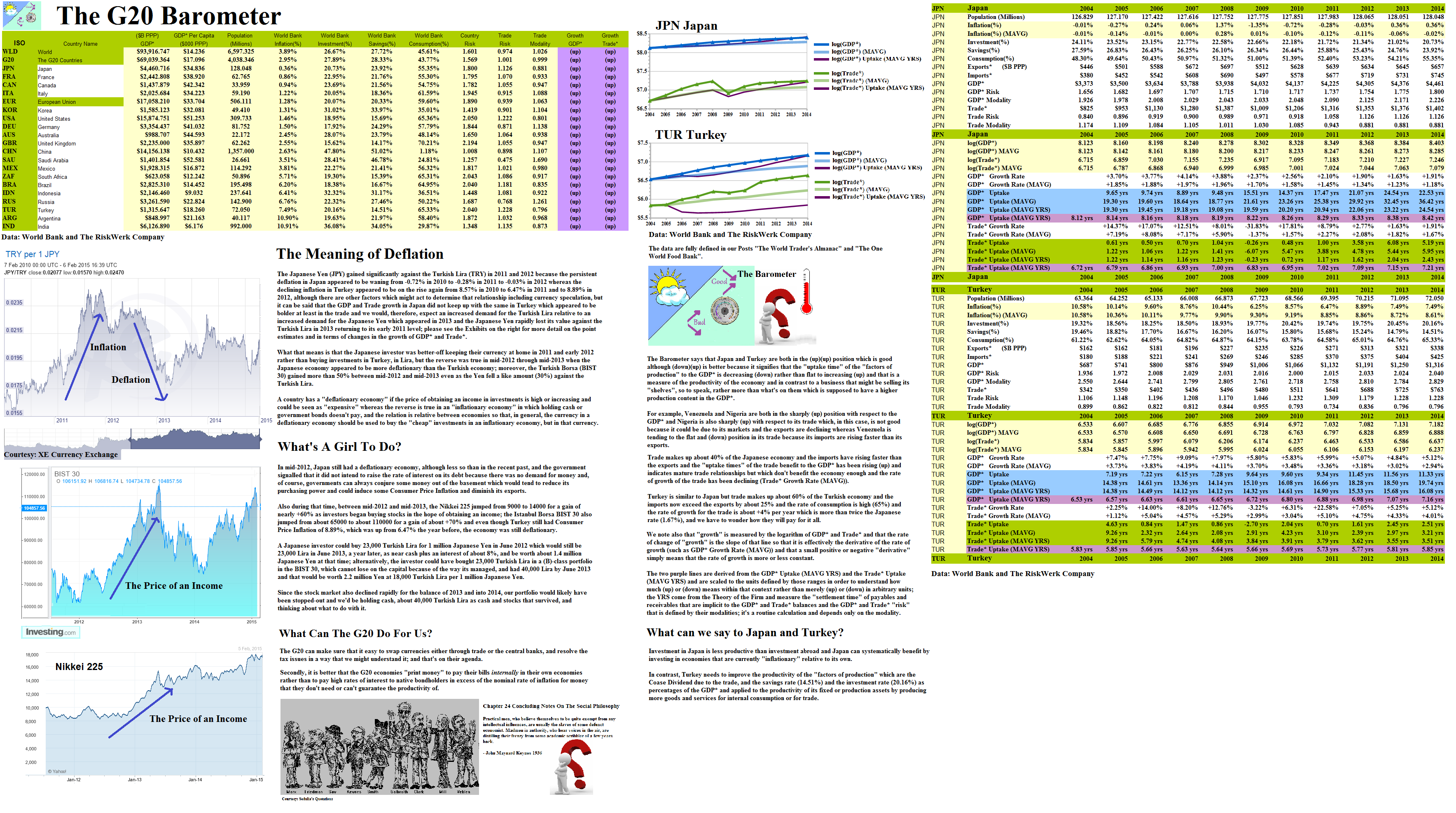

Of the nineteen countries and the European Union which consists of twenty-eight countries, only Australia, China and the United Kingdom seem to be working as planned with Consumer Price Inflation (CPI) in the range of 2% to 3% and all of the other countries are deemed to be too low (less than 2%) or too high (above 3% and possibly unknown in India and Argentina above 10%).

Figure 1: The G20 Barometer

And even of these three, only Australia is “working to spec” and has CPI inflation of 2.45% and similar growth in its trade (2.36%) and GDP* (2.35%) with current point estimates being a little higher at around 4%; the United Kingdom under-performs the growth measurements and China exceeds them but they have similar rates of Consumer Price Inflation; please see Figure 1 on the right (and click on it to make it larger as required) for a brief summary of the differences between the two extreme cases, Japan and Turkey, and how investment can be used to moderate between a deflationary and a nominally inflationary economy.

In the case of Argentina, which is one of the G20 countries, we concluded that the “economy” was fine for those who owned it but that the Argentine government might have a problem servicing its foreign currency debt and a high rate of inflation has caused real shortages in essential consumer goods (Bloomberg, February 5, 2015, Why Argentina’s President Really Can’t Afford to Mock China); and Canada seems unable to avoid a turf war with its largest customer, the US, even though it has a lot of turf to work on (Business Insider, February 5, 2015, Canadian Government ‘Optimistic’ Trade War With U.S. Averted); and the very small economy in Greece is getting whipped into shape by Germany (Bloomberg, February 5, 2015, Greek Leaders Return Home for Rethink After Rebuff From Germany).

G20 Summit Leaders Window dressing or the real thing?

We’re not surprised, of course, that economic and fiscal policy by the book might not agree with political and sovereign agendas but it seems that none of these countries doesn’t have a complaint about one or more of the others (The Huffington Post, February 5, 2015, Here’s The Biggest Problem With Obama’s New Trade Push and February 2, 2015, Russia Warns Of Recession In 2015 Amid Sanctions And Low Oil Prices).

And it could be that the November 2015 Summit in Antalya, Turkey, will turn-out to be a bust and a triumph of Realpolitik for which there is no cure not settled by a call to arms.

Is There A Problem?

The Barometer (please see Figure 1 above) shows that there is a difference between the current Japanese economy which is deflationary and has a low rate of Consumer Price Inflation (CPI 0.36%) and the Turkish economy which has a high rate of Consumer Price Inflation, about 7.5% but down from 10% in 2008, and an economy that has doubled in size in the last ten years but for which the growth has slowed down since 2009 and it is also a “deflationary economy” as measured by the “high price for an income” which can be gauged from the investment opportunities afforded by their capital markets.

Moreover, in economic terms, the World is very small – the median income is about $11,000 (PPP) and it’s obtained in Egypt, Peru, and Tunisia, but there are 4.3 billion people who earn less than that for a total of $29 trillion which is about 1/3rd of the World economy of $94 trillion (PPP); in order to raise their income by $1,000 per year by the book, we would need to increase the World GDP by $1,000 ×4.3 billion×3 = $12.9 trillion (since they only get a third of it) which is 13% above the current World economy.

Figure 2: World Per Capita Income

How we are going to do that is a good question for the folks at the G20 but they haven’t asked it.

Moreover, it’s not about more money in our pockets to spend but that a people and its government, whatever it is, might have the resources to live the way that they want to.

Have we moved the needle? No, in ten years the percentage of the world population that is still below the average, the median, and the weighted average income, is still the same – 71% of the people – even though the GDP* has nearly doubled and there are only 500 million new people – just one nation; please see Figure 2 above for further details.

Obviously, the G20 and the G8 before them are failures – F is their grade.

The solution is that every economy is different and needs to develop its trade in a different way and in order not to have to do the impossible, we need to find some way to inject $2.9 trillion into the bottom-line of the bottom two thirds this year; does that seem impossible?

It can be done with world trade which balances out to about $30 trillion in imports and $30 trillion in exports; it’s just a matter of where they’re sourced and how they’re used because it’s not just exports that count – imports of technology and materials can also be used to activate the local industry and raise the level of the GDP.

Moreover, an economy that is deflationary with respect to another can expect to profitably invest in the latter which also doesn’t seem too hard to do and every country can, more or less, profitably invest in itself and any of the ones to the right of it (please see Exhibit 1 below) and with due attention to their customers can benefit the rest of the World.

Since every country will know what its opportunities are, we’ve profiled The Barometer for the G20’s in Exhibit 1 below from low CPI inflation or deflation to high CPI inflation but we note that neither measure is a measure of an inflationary or deflationary economy; they are afterthoughts and possible consequences, but they not causes and the hallmark and cause of a deflationary economy is a high price for an income from money.

Exhibit 1: The G20 Economies From Deflation to Inflation

|

Figure 1.1: JPN Japan FRA France |

Figure 1.2: CAN Canada ITA Italy |

Figure 1.3: EUR European Union KOR Korea |

|

Figure 1.4: USA United States DEU Germany |

Figure 1.5: AUS Australia GBR United Kingdom |

Figure 1.6: CHN China G20 Countries |

|

Figure 1.7: SAU Saudi Arabia MEX Mexico |

Figure 1.8: WLD World ZAF South Africa |

Figure 1.9: BRA Brazil IDN Indonesia |

|

Figure 1.10: RUS Russia TUR Turkey |

Figure 1.11: ARG Argentina IND India |

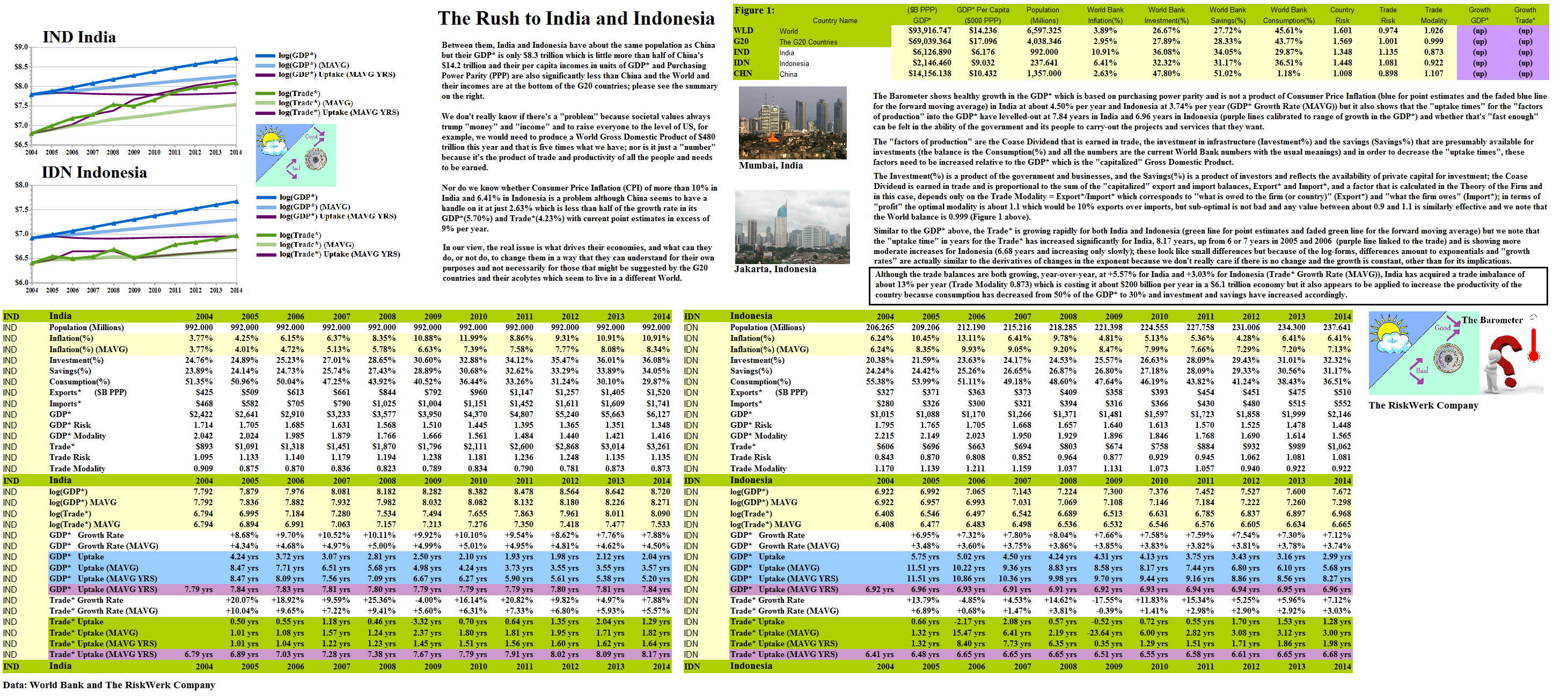

Exhibit 2: The Rush to India and Indonesia – A Practicum

Figure 2.1: The Rush to India and Indonesia – A Practicum

For more information on The Barometer, foreign economies and trade, please see our Posts “(P&I) The World Trader’s Almanac” , “(P&I) The One World Food Bank” and “(P&I) La Francophonie & The Commonwealth“.

And for more information on real “risk management” in modern times and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary and “(P&I) Dividend Risk and Dividend Yield“, and our recent Posts “(P&I) The Profit Box” and “(P&I) The Process – In The Beginning“; and we’ve also profiled hundreds of companies in these Posts and the Search Box (upper right) might help you to find what you’re looking for, such as “(B)(N) TLM Talisman Energy Incorporated” or “(B)(N) ATHN AthenaHealth Incorporated” or “(B)(N) PETM PetSmart Incorporated“, to name just a few.

And for more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice. And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

And for more on what risk averse investing has done for us this year, please see our recent Posts on “(P&I) The Easy (EC) Theory of the Capital Markets” or “(B)(N) The Easy (EC) Theory of the S&P 500“, and the past, The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.