(P&I) Deflation – Japan & Company

Essay. “Deflation” which is defined as a falling price for baskets of consumer or producer goods, is a current concern of nearly every economy in the world because the long-term prognosis for “deflation” is a low demand for consumer or producer goods and services and, therefore, falling prices, idle businesses and production-lines, rising unemployment and under-employment, and low or slow “economic” growth.

Essay. “Deflation” which is defined as a falling price for baskets of consumer or producer goods, is a current concern of nearly every economy in the world because the long-term prognosis for “deflation” is a low demand for consumer or producer goods and services and, therefore, falling prices, idle businesses and production-lines, rising unemployment and under-employment, and low or slow “economic” growth.

However, the definition of deflation (or inflation, which we’ll also consider) is not its cause, but only a symptom, and policy makers are generally transfixed by the symptoms and, apparently, perplexed by the cause and, as in medicine, it’s a natural hope that we might cure an illness by relieving its symptoms, but what if a surgery is required to remove the cause? And what do we do if we know that removing the cause will kill the patient, or the doctor?

The cause of deflation is a “high price for an income”, and that is also its signature, but we need to look closely at the “factors of production” in the economy that is deemed to be deflationary; and, similarly, the cause of an inflationary economy is a “low price for an income” which is the signature of an inflationary economy.

August Ludwig von Rochau (1810-1873) & Otto von Bismarck

Realpolitik

In many countries, we can look at the prevailing prices for stocks in an active stock market to determine whether the economy is inflationary (a low price for stocks), deflationary (a high price for stocks), or neither – a “just” or “fair” price for stocks, which is almost unheard of (please see below) – but there are also other reasons that the price of an income could be deemed to be too high, or too low.

Figure 1: Traders Almanac – The Profit Box – Company D

If we say that an economy is “normal” if neither inflation nor deflation are a pressing or vexing concern, then an economy is “normal” if and only if the “Profit Box” due to foreign trade is “as large as possible”, signifying that the country and its trading partners have as many options as possible in negotiating their terms of trade; please see Figure 1 on the right, and for more details “(P&I) The World Trader’s Almanac“.

For example, in a “normal” commerce, buyers don’t offer the highest price (inflationary), nor will sellers accept the lowest price (deflationary), but that can also be re-phrased as buyers tend to offer a lower price (deflationary) and sellers tend to ask for a higher price (inflationary).

But what if the “normal” commerce is not permitted, or not effective, because of some overriding demand or supply issue, or the buyer/seller relationship is asymmetric and one of the parties has more “bargaining” power, or just “power”?

For example, a person who is already in debt might have a problem obtaining credit (a low modality and a high Debt Risk), whereas a person who already has a lot of money (a high modality and a low Debt Risk), might not be interested in having more money, but is interested in having some other kind of benefit, such as keeping it.

For example, a person who is already in debt might have a problem obtaining credit (a low modality and a high Debt Risk), whereas a person who already has a lot of money (a high modality and a low Debt Risk), might not be interested in having more money, but is interested in having some other kind of benefit, such as keeping it.

The range of “normal” for debt is a modality, 1/e<α<e, which is equivalent to 2>Debt Risk = 1 – log(Modality) > 0, so that we may say that a “high debt risk” has Debt Risk>2 and a “low debt risk” has Debt Risk<0; nor should we be perplexed if a person, or company, or government, owes less than 3× what its owed, or is owed less than 3× what it owes, where we use the shorthand 3=2.718128… the exponential.

For example, governments (which we will distinguish from the country governed) are almost always in debt, and we expect (please see our Post “(P&I) The Process – The 1st Real Dollar” or Figure 1 above) that the government will “owe” (P) at least three times “what is owed to it” (R) so that its modality, α=R/P, will tend to be less than 0.333 for a Debt Risk = 1 – log(Modality) > 2.1 (high debt risk, “inflationary”).

But that is not a problem for governments because they can always “print money” to pay their debts to the governed and might only have a problem in paying their debts to the ungoverned in foreign locales, and in a foreign currency.

In particular, a government that is willing (or has to) to pay more for its debt by lowering the price of government bonds (or raising the rate of interest on them), may cause an inflationary economy because the “price” of an income is made lower by buying their “cheap” bonds, and it may cause the collapse of its stock market, if it has one, because of a “flight to safety”, and it might also invite foreign exchange to invest in its debt, or its equities, which are both for sale at a lower price.

On the other hand, a government that pays its bills in “cash” and refuses to raise the rate of interest on its debt, creates a deflationary economy and a “flight to income” in its stock market, both of which also tend to discourage foreign investment because the price of a “business”, which gives an income, becomes so high in the local currency.

Keynes General Theory 1936

It’s noteworthy, however, that the extremes in both cases create the opposite; that is, too much printed money results in hyper-inflation, and not enough money results in a slow death by deflation, and an inflationary economy might only be resolved by a hyper-inflationary economy in which all debts are paid in “worthless” cash and no business is for sale, depending on how much of a problem the government has with its debt; and a deflationary economy might result in slow economic growth, unemployment, and under-employment, and no way out because the price of an income is very high and encourages further vesting in what the people already own, including their cash.

The real question, then, is, How can we encourage inflation, and a lower price for an income, but not too much, and what is the normal rate of inflation that we might encourage?

The answer is that the normal and, in fact, minimal rate of inflation is 8.3%, but it matters whether that “rate” is per decade (deflation), per year (exuberant growth), or per month (hyper-inflation), and the time frame is governed by the Country Risk and the Trade Modality, notwithstanding what good or harm governments might do, out of school, to curry favor with the voters (if there are any); please see below.

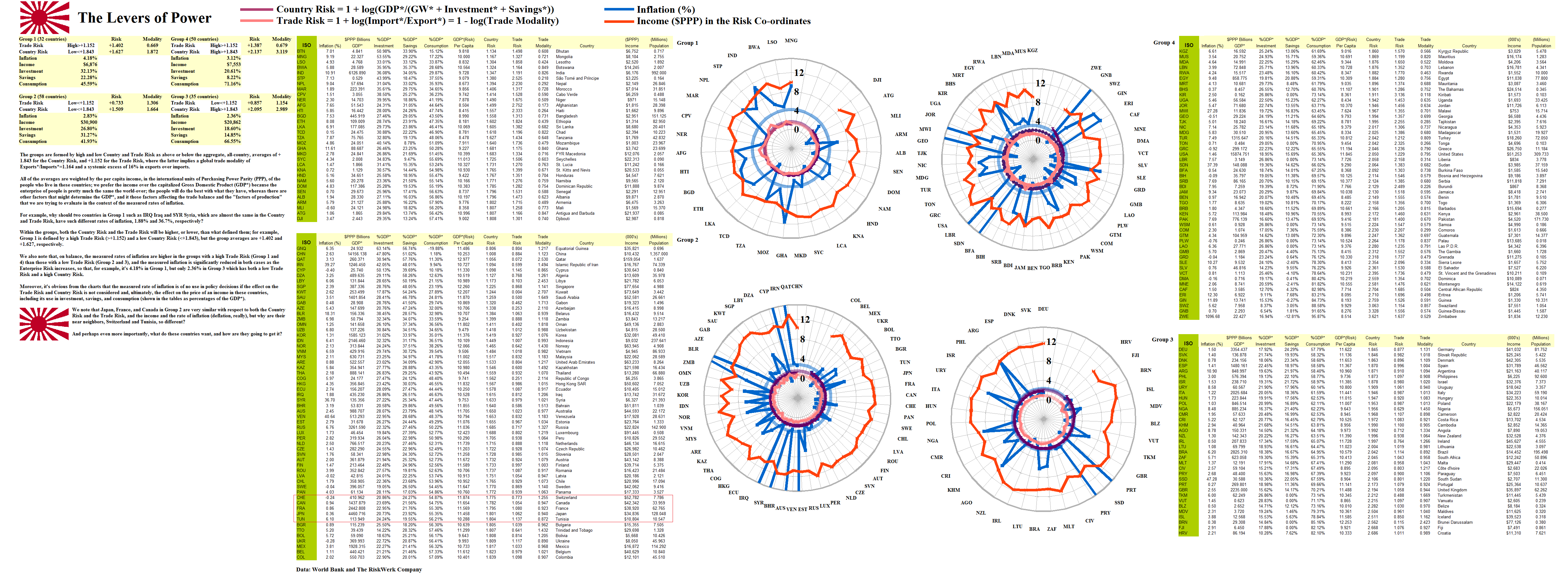

Country Risk & Trade Risk

Whether a country succeeds in the world, or not, is determined exactly by its ability to trade, and that is no less true of countries, or companies, than it is in our interpersonal relationships, if we need to consider the force of that observation.

It is possible to quantify whether a country has an inflation or deflation “problem” by examining its Trade Modality in which the imports and exports are determined as a percentage of its capitalized Gross Domestic Product (GDP*) in the international units of Purchasing Power Parity (PPP) that are calculated by the World Bank and the International Monetary Fund (IMF), and to determine its cause by understanding why obtaining an income is expensive, or cheap, in that country, which is measured by the Country Risk.

The Country Risk = 1 + log(GDP*/(GW* + Investment* + Savings*)), where GDP* is the capitalized Gross Domestic Product (as above) and can be understood as the country’s “net worth” or “shareholders equity” in the same sense as it is for firms; in particular, the country’s net worth is “supported” by its ability to earn an income by “producing” the factors of production, which are the Coase Dividend, GW*, earned from trade, and the country’s investments in its fixed capital and inventories (Investment*), and its savings (Savings*).

The Trade Risk = 1 + log(Imports*/Exports*) = 1 – log(Trade Modality) is similar to the Debt Risk; a country with a large excess of imports over exports has a continuing liability which needs to be financed if the standard of living in that country is not to decline, or invite the gun-boats, and, hence, it has a high Trade Risk.

Conversely, a country with a negative Trade Risk has a continuing excess of exports over imports, and will come under competitive, and even belligerent, pressures from other countries which need to pay for it all.

If we do that for all the countries in the world, then the average Trade Risk = +1.152, and is equivalent to the Trade Modality = Exports*/Imports* = 1.164, and implies a global excess of 16% of exports over imports among all the countries, which needs to financed by some of them.

Similarly, the Company Risk = +1.843 and implies a “Country Modality” of 2.322, which is typical of the companies in the Dow Jones Industrials (1.27 with variation between 0.65 (Boeing Company) and 3.63 (Visa)), or the S&P 500 companies (1.20 with a much larger variation between 0.28 (Plum Creek Timber Company REIT) and a dozen companies with modalities in excess of 4.0).

However, the average that we calculate for the Trade Risk and Country Risk is weighted by the per capita income in the international units of Purchasing Power Parity (PPP) calculated by the World Bank and the International Monetary Fund (IMF), in order to reflect the situation of the people in these countries more accurately than does the GDP*, which income is often proscribed to government interests.

If we then say that the Trade Risk and Country Risk are high, or low, depending on whether they are above or below the world averages, as weighted by the per capita incomes, we can partition the world into four groups of countries which all demonstrate the same property of high and/or low Trade Risk and Country Risk; please see Exhibit 1 below for more details.

Exhibit 1: The Levers of Power – Country Risk & Trade Risk

Figure 1.1: Group Country & Trade Risk

Where there can be life, there will be life

Where there can be life, there will be life, and it begets, and begets, and begets, …., and begets, and it thrives on a difference, W, that is “compounded” and “additive” as 1 + W + W² + W³ + … without end.

It’s noteworthy, though, that in this “Equation of Life”, the progenitor, (1), is called on only once, to create (W), which thereafter, plays only with itself and its progeny as (W)(W) = W² and (W)(W)² = (W)³, and so forth, so that, in effect, we get a series of new (1)’s, each of which has a real (1) in it, but which is more scattered and does not have the integrity of the original and first (1).

Growth is not like “compounding”

We mention this because “growth” is not like compounding a capital, (1), as (1)×(1+w)^k, for some rate of interest, w, and time period, k, because the (1) is re-used each time, as well as its progeny, to give us 1 + w + 2×w² + 3×w³ + … and so forth, and the numbers 1, 2, 3, and so forth, are a result of “re-using” the original (1) which is returned to us at the end of (k); we also note that this formula is more cogently expressed as (1)×exp(k×f), where f=log(1+w) is the “force of interest”, and the inverse of the “e-folding time”, 1/f, and that the “growth” is “linearized” as k×f by taking the logarithm.

The “operator”, (W), that we’re looking for is given to us by the Theory of Firm which implements The Process in which the difference is between the “receivables” (R) and “payables” (P) that are created by a company, (1), and its “trading connections” which are in-process, and which “creation” respects the “N/B/W”-financing model and the “demonstrated societal norms of bargaining practice and risk aversion” which may be expressed in different forms in different societies but, as in life, not all the forms work and too much deviation from the “standard form” just results in “death”.

The linearized form of the growth equation, δ = log (1 + W + W² + W³ + …) = log (1/(1-W)) = -log(1-W), operates in the “space” of receivables and payables (as sets, possibly with a topology, and ultimately with a σ-algebra and probability measure) that are created by the firm, (1), and its trading connections, and the “projection”, 1 – δ, “illuminates” those results in the same units as the balance sheet of the firm; for example, the projection of (1) is (1-δ)(1) = GW* + “Accumulated Depreciation”, where GW* is the Coase Dividend and the accumulated depreciation is the same, or similar, to the usual accounting definition and meaning; moreover, if the firm fails to develop its trading connections (and customers), the projection of the firm is (0).

When we “linearize” the action of (W), the modality, α=R/P, where R is “what is owed to the firm” and P is “what the firm owes”, is an “eigenvalue” of (W) (similar to the “force of interest”, above, but also understood as the “entropy” of the process) for which W(α) = CR(α) – DB(α) is the difference between the “Credit Float” CR(α) and the “Debit Float” DB(α) developed in the Theory of the Firm, which is similar (but not necessarily comparable to) to the “working capital” of the firm which is usually described as the difference between the current receivables and payables as calculated by the accountants, where in the latter “current” means within one year, whereas in the Theory of the Firm, there is no “time”.

Global Trade Is A World Economy

However, the global trade between the 175 countries of the world, is an “economy” and we know exactly who the firms are, and who the trading connections are; it’s also a “free economy” in that if we don’t want to deal with one country, or they don’t have we want, or they don’t want what we have, then we can try another, absent colonialism or “trade blocs” which are eventually all defeated in any case.

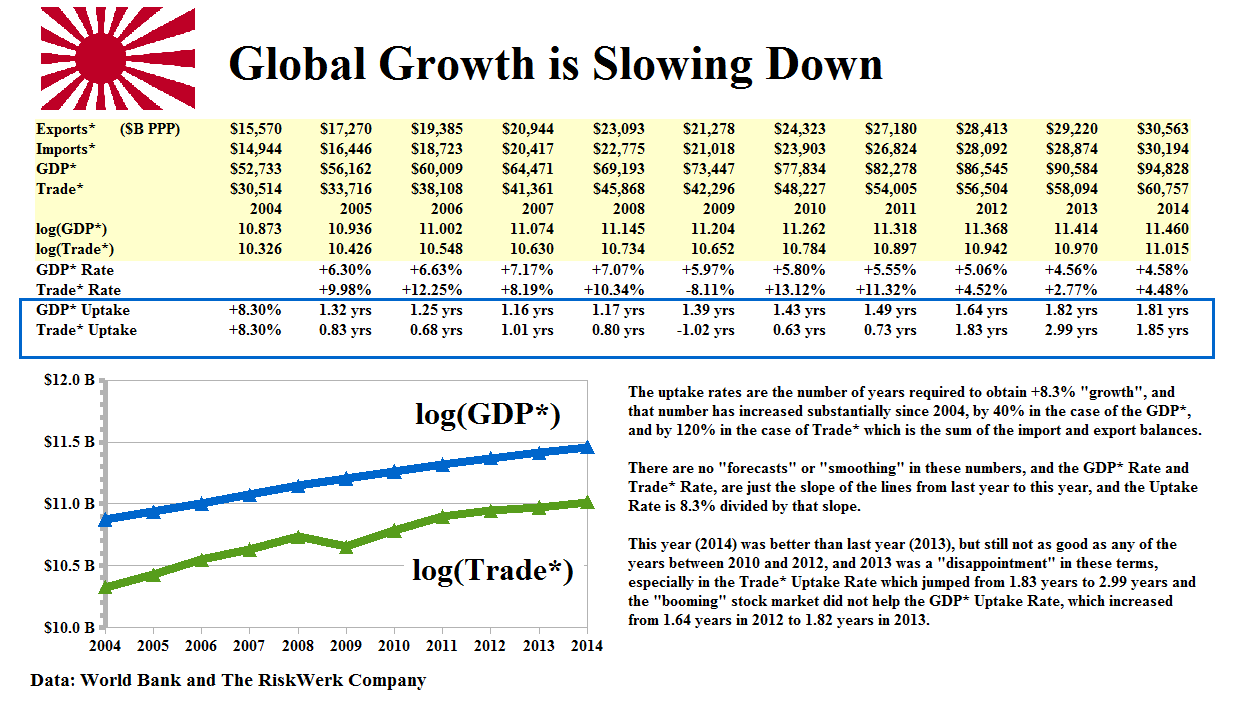

Exhibit 2: Global Growth is Slowing Down

Figure 2.1: Global Growth

As a result, the global trade modality, α = Export*/Import* = 1.164, is almost optimal for the “Profit Box” which occurs with a modality of α≈1.10; we also know that the expected rate of growth (not exactly “inflation”) is 8.3% and we can determine the “take-up” rate in years by simply measuring Export* + Import* over some number of years (which we do in rolling blocks of six years in order to “capitalize” these quantities); please see Exhibit 2 on the left.

Courtesy: Mrs. Fung Wong Fung Ting Company

The chart shows that we have been in a “deflationary” economy for the last ten years, but policy-makers seem to be only discovering that now and rather than address the “systemic” issues, they might just tinker with the rates of inflation, which creates a “drama” as in 2009, but no “show” worth remembering.

Particularly disturbing is the oft-repeated nostrum of world leaders that they must do something to fight or encourage “inflation and inflation expectations” suggesting that it is we, the hapless people and allegedly “insatiable or cautious consumers” who are growing in leaps and bounds, that create the problem – well, we guess not.

For more information on real “risk management” in modern times and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary and “(P&I) Dividend Risk and Dividend Yield“, and our recent Posts “(P&I) The Profit Box” and “(P&I) The Process – In The Beginning“; and we’ve also profiled hundreds of companies in these Posts and the Search Box (upper right) might help you to find what you’re looking for, such as “(B)(N) TLM Talisman Energy Incorporated” or “(B)(N) ATHN AthenaHealth Incorporated” or “(B)(N) PETM PetSmart Incorporated“, to name just a few.

And for more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice. And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

And for more on what risk averse investing has done for us this year, please see our recent Posts on “(P&I) The Easy (EC) Theory of the Capital Markets” or “(B)(N) The Easy (EC) Theory of the S&P 500“, and the past, The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.