(P&I) Deflation – Tinker, Tailor, Soldier, π

Essay. There’s a lot of “tinkering” going on in the World Economies this weekend – who knows about tomorrow? Relax. Just do business, build trade, and good relationships, and we’ll be fine (Bloomberg, November 14, 2014, World Economy Worst in Two Years, Europe Darkening, Deflation Lurking: Global Investor Poll).

Exhibit 1: The Wheel of Fortune

Figure 1.1: The Wheel of Fortune

However, we don’t share that dark view of the world by economists (ibid, Bloomberg) who are regarding the alleged “dangers” of inflation and deflation, as they measure it, nor do we have much use for it, because it doesn’t explain anything – it’s like observing that it’s raining again, and we left our ‘brollies at home.

But we are very concerned about the use of “trade sanctions” in order to enforce a “moral hegemony” to which no country, or community of countries, is entitled.

The Crimean War 1854-1856 at Malakoff post-Balaklava

Because the next step is always the same – a declaration of war – because “trade sanctions” have dire consequences for the “enforcers” as much as for the “enforcees”, and more so if they have resources of their own that reduce the “forces” of the “enforcers”, and exclude them from their trade to create some shallow bunkers, and the end of reason; please see below for the antidote because there is nothing forthcoming from the economists.

The Price of An Income and The Real Cost of Governing

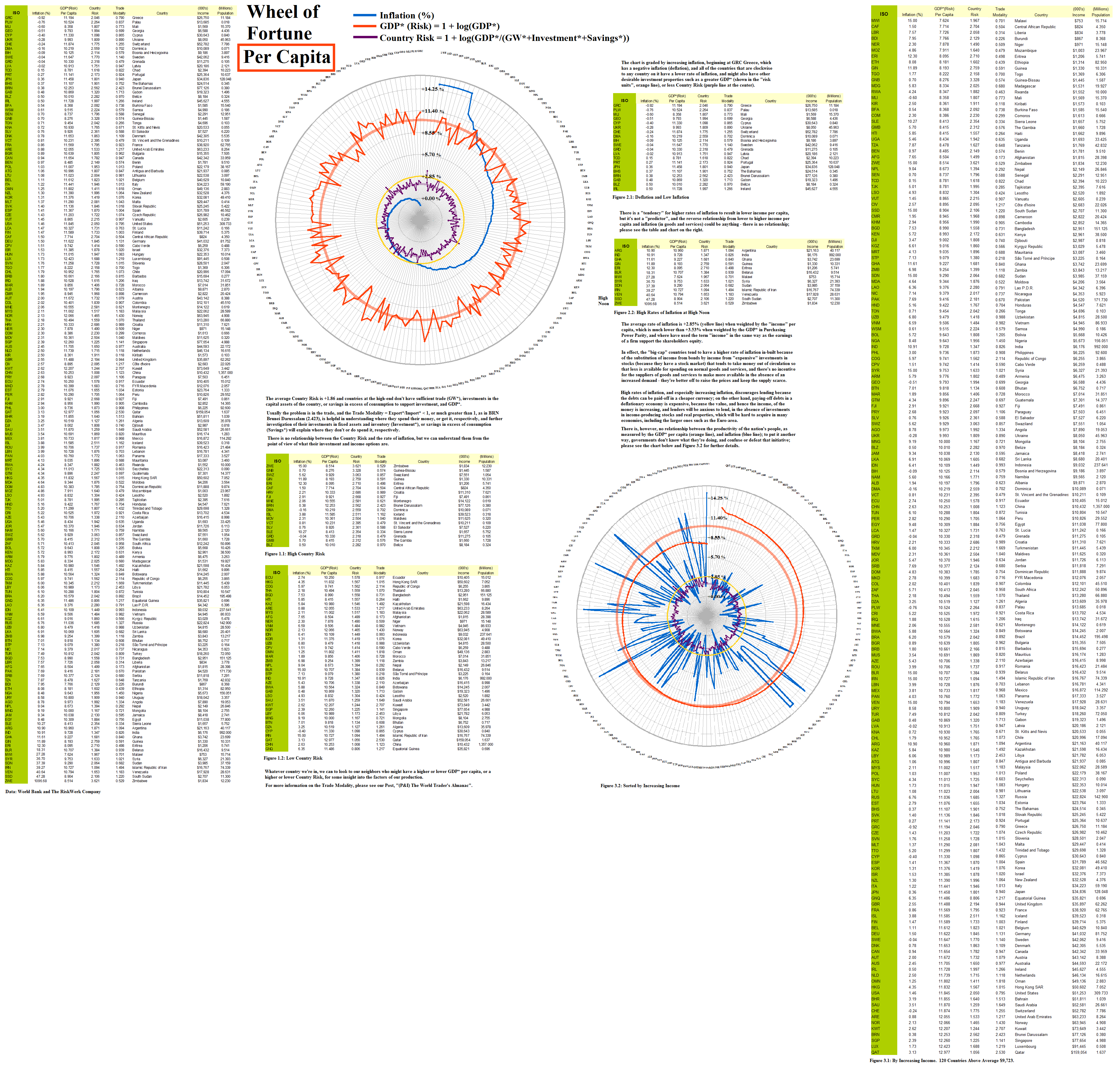

Inflation in the price of consumer goods and services doesn’t depend on the GDP* (Gross Domestic Product as capitalized in the international units of Purchasing Power Parity) of a country, or the GDP* per capita, or the Country Risk, which is a competent measure of the productivity of its people; please see Exhibit 1 above for a re-cap of “(P&I) Who will cast the first stone?” and Exhibit 2 below for further details.

In contrast, we say that “inflation” depends only on the cost of governing and that cost can be a positive, real, out-of-pocket, cost to the taxpayers, such as the cost of the government debt, or the cost of its expenditures on national and international enterprise or adventures (such as war); or it can be a persistent negative opportunity cost due to its failure to assure the infrastructure of the country for which it is charged, and which can be measured by the GDP* per capita; all of these cases occur in the examples below, and no country is exempt from them.

Figure 2: S&P 500 What are they buying?

For example, the current rate of inflation in the United States is estimated at 1.46% per year, and the “target rate” is 2% which appears to be more easily said than done, and that problem also bedevils the Euro-area countries at the present time; the cost of US government debt, however, is about 1% in treasury bills of three to five years duration, or less, but the prices of stocks in the stock market have been bid-up by about 50% in the last few years, and the reason is that investors (and all savers) are willing to pay a high price for an income which they can’t get from government bonds, and it is the price of an income that is the real measure of inflation in a country; please see Figure 2 on the right.

With respect to Figure 2, is it reasonable that investors are willing a pay a 50% premium over 2012 prices in order to obtain an aggregate dividend yield of 2.1% and a total return on their equity, the shareholders equity, of 16.4% by buying the stocks of companies in the S&P 500?

We must say, yes, it is, because that’s what they’re doing, and they will keep on doing it until the government is willing and able – or has no choice – to pay a higher price for its debt – and if it does, that alone will cause a higher rate of inflation as measured by the price of consumer goods and services because of the increased cost of debt, but reduce the price of an income in stocks because we can expect an alleged “flight to safety” in government bonds, and we use the term “alleged” because a guaranteed coupon and a guaranteed capital does not necessarily mean a guaranteed real income if “inflation” is rising.

However, if that happens, has “inflation” gone up or down? In our view, it has gone down because the price of an income has likely gone down, given the typical difference between the interest rates on government bonds and the price of an income in the stock market, or the price of buying a business (which in some countries is almost impossible).

Moreover, investors have ploughed about $6 trillion into the S&P 500 since 2012, and another $1.5 trillion into the Dows, for example, and that’s not all, to earn a 2% or 3% or 4% dividend yield; in total, that’s more than $10 trillion that can’t be spent on goods and services, and when they pull it out, there will be a stock market crash, but no new money, and no new income – just cash, all set for the bonds.

If we think about the measure, “the price of income” now as “inflation”, we can answer a lot of questions for which, at the present time, there might be neither question nor answer; for example, why is the price of an education so high in the United States, so much so that debt-collectors are chasing graduates right-up into their Social Security, whereas the price of a higher education in Germany, Russia, and Cuba, is free, or next to nil? And what does the high and forbidding cost of an education do for the price of an income, or the quality of the graduates, or the productivity of the work force?

Or if we raise the minimum wage, will that tend to increase the real incomes of workers, and more workers, over time? The answer is, obviously, yes it does, and if we’re unsure, we need only consider the state of incomes pre-war (1940) and post-war (1950) and what that has done for the growth of America, which is a lot more than just higher incomes and more purchasing power.

Our goal is to understand whether we could have more of what we have, and what might we do to get more with what we have; it’s not an idle question because the answer is systemic, and although the United States has the highest Gross Domestic Product (GDP*) in the World, there are ten countries that have a higher GDP* per capita – how did they get it, and what do they have to do to keep it?

And there are many more that are close per capita, and don’t “work” at all; and many that are not even on the scale, and “work” from sunrise to sunset, every day, and still can’t buy anything.

And since people are pretty much the same all over the World, why is that? Please see Exhibit 2 below.

High Inflation and Deflation Per Capita

Economists measure “inflation” as an increase or decrease in the “price” of consumer (or producer) goods and services, month over month, annualized, but we note again that that has not much to do with the price of an income which is determined by the price of government bonds and the price of our investments, which could be in stocks or in companies that we are trying to buy.

However, the notion of “price inflation” is fundamentally flawed because there is a “time period” involved; for example, even though the current annualized rate of inflation in the United States is 1.46%, it doesn’t feel like that when we go to the store and routinely obtain discounted prices on most consumer goods, such as 30% off, or 2 for 1, which is the signature of a deflationary economy, whereas the positive rate of inflation +1.46% suggests that prices are still increasing, when they are not, and we won’t know that until much later.

A sequence of decreasing annualized rates of inflation might suggest that we are already in a deflationary economy and, therefore, that growth, as measured by the Gross Domestic Product with Purchasing Power Parity (PPP), is slowing down, but still might not have stopped, or is negative; and if the rate of price inflation begins to increase, then we can say that growth is “picking-up” and there is a higher demand for goods and services, but are we just working off the surplus from the lower inflation environment?

As a result, government policy is always mis-informed – the news is always late – and the cause is not clear, and the cost is the same as compounding one error with another. And what tools do they have? “Would you all like more money or less?” But what does that have to do with the economy and the welfare of the nation? Please see Exhibit 2 below for the cost of an income, and what that means.

Exhibit 2: The Wheel of Fortune Per Capita

Firgure 2.1: The Wheel of Fortune Per Capita

That is still not the whole story, although the tools are pragmatic and ready to cook; please see our Post “(P&I) One economist at a time” for the connection between “inflation” and “growth”.

And for more information on real “risk management” in modern times and additional references to the theory and how to read the charts and tables, please see our Post, The RiskWerk Company Glossary and “(P&I) Dividend Risk and Dividend Yield“, and our recent Posts “(P&I) The Profit Box” and “(P&I) The Process – In The Beginning“; and we’ve also profiled hundreds of companies in these Posts and the Search Box (upper right) might help you to find what you’re looking for, such as “(B)(N) TLM Talisman Energy Incorporated” or “(B)(N) ATHN AthenaHealth Incorporated” or “(B)(N) PETM PetSmart Incorporated“, to name just a few.

And for more applications of these concepts please see our Posts which rely on the Theory of the Firm developed by the author (Goetze 2006) which calibrates The Process to the units of the balance sheet and demonstrates the price of risk as the solution to a Nash Equilibrium between “risk-seeking” and “risk-averse” investors within the demonstrated societal norms of risk aversion and bargaining practice. And for more on The Process, please see our Posts The Food Chain and The Process End-Of-Process.

And for more on what risk averse investing has done for us this year, please see our recent Posts on “(P&I) The Easy (EC) Theory of the Capital Markets” or “(B)(N) The Easy (EC) Theory of the S&P 500“, and the past, The S&P TSX “Hangdog” Market or The Wall Street Put or specialty markets such as The Dow Transports & Utilities or (B)(N) The Woods Are Burning, or for the real class action, La Dolce Vita – Let’s Do Prada! and It’s For You, Dear on the smartphone business.

And for more stocks at high prices, The World’s Most Talked About Stocks or Earnings Don’t Matter – NASDAQ 100. And for more on what’s Working in America, Big Oil, Shopping in America or Banking in America, to name just a few.

Postscript

We are The RiskWerk Company and care not a jot for mutual funds, hedge funds, “alternative investments”, the “risk/reward equation” and every other unprovable artifact of investment lore. We have just one product

The Perpetual Bond™

Alpha-smart with 100% Capital Safety and 100% Liquidity

Guaranteed

With No Fees and No Loads on Capital

For more information on RiskWerk, please follow the Tags or Categories attached to this Letter or simply enter Search for additional references to any term that we have used. Related data may be obtained from us for free in a machine readable format by request to RiskWerk@gmail.com.

Disclaimer

Investing in the bond and stock markets has become a highly regulated and litigious industry but despite that, there remains only one effective rule and that is caveat emptor or “buyer beware”. Nothing that we say should be construed by any person as advice or a recommendation to buy, sell, hold or avoid the common stock or bonds of any public company at any time for any purpose. That is the law and we fully support and respect that law and regulation in every jurisdiction without exception and without qualification to the best of our knowledge and ability. We can only tell you what we do and why we do it or have done it and we know nothing at all about the future or the future of stock prices of any company nor why they are what they are, now. The author retains all copyrights to his works in this blog and on this website. The Perpetual Bond®™ is a registered trademark and patented technology of The RiskWerk Company and RiskWerk Limited (“Company”) . The Canada Pension Bond®™ and The Medina Bond®™ are registered trademarks or trademarks of the Company as are the words and phrases “Alpha-smart”, “100% Capital Safety”, “100% Liquidity”, ”price of risk”, “risk price”, and the symbols “(B)”, “(N)” and N*.